Today The Official Merchant Services Blog has learned of a new partnership agreement between Host Merchant Services and cloud hosting services provider. With HostingCon 2012 right around the corner, this partnership announcement is well-timed. Credit card processing firm Host Merchant Services has announced that it has entered into a strategic marketing partnership with ServInt.

Servint is the latest provider to join a partner program that has taken the web hosting and cloud services industry by storm. This alliance will give ServInt the ability to provide flexible and customizable merchant services and credit card processing to its customers quickly and efficiently.

ServInt, based in McLean, VA, has been providing managed hosting services to businesses and enterprises around the world since 1995. Today, they offer a full portfolio of VPS, dedicated, IaaS cloud and PaaS Java hosting to clients in more than 130 countries.

Partnering with Host Merchant Services, the premier provider of payment processing and e-commerce services for small businesses and medium businesses, lets ServInt maintain its high level of quality customer service while offering a guaranteed best-rate plan for merchant services. ServInt customers will be able to accept credit card payments easily from a merchant services provider that is intimately familiar with the needs of cloud hosting customers and e-commerce merchants.

Host Merchant Services is a registered Independent Sales Organization (ISO) with Visa U.S.A. and MasterCard International with bank sponsorship provided by Wells Fargo Bank, Walnut Creek, CA. The company specializes in providing world class customer service and support to its credit card processing customers.

“ServInt is an outstanding, reseller-centric, cloud services company that we are excited to partner with,” said Host Merchant Services CEO Lou Honick. “Host Merchant Services shares ServInt’s dedication to quality customer service. Their customers will benefit greatly from a seamlessly integrated payment processing solution, from a provider that really understands their needs. ServInt customers will enjoy transparent pricing, 24x7x365 customer support, and a skilled technical support team to assist them in quickly integrating the service to their website.”

ServInt COO Christian Dawson added, “ServInt prides itself on being one of the most reseller-friendly service providers in the hosting marketplace. Our partnership with Host Merchant Services further enhances our ability to meet the needs of this critical segment of our customer base, as it adds a critical business product to the best-of-breed support services we offer – at very favorable terms – to the hosting reseller community.”

The partnership is part of a Host Merchant Services initiative to provide web hosts and cloud operators like ServInt a fast and transparent third party solution for processing credit cards. The Host Merchant Services partner programhas been gaining traction at a rapid rate to become the “go to” choice for web hosts that want the best mix of revenue sharing and quality service without onerous contracts or commitments.

Host Merchant Services COO Dan Honick sums it up by saying, “Our customers and partners stay with us because they are happy with our service.”

About ServInt

ServInt is a pioneering provider of high-reliability, managed cloud hosting services for enterprises worldwide. Founded in Northern Virginia in 1995, ServInt provides a range of IaaS, PaaS, VPS and dedicated server packages to hosting service resellers, web designers, developers and online businesses in more than 130 countries. To learn more about ServInt’s cloud, VPS and dedicated hosting solutions you can visit their website http://www.servint.net/.

About Host Merchant Services

Host Merchant Services is a different type of merchant services company which focuses on delivering the industry’s lowest processing rates while providing industry-leading service and support. The company’s products include merchant services and credit card processing. Host Merchant Services is the only merchant services company with a partner program that guarantees unsurpassed pricing, support, and customer service. The company is headquartered in Newark, Delaware and executes all operations with the manifesto of “bringing trust to merchant serivces”.

To learn more about Host Merchant Services visit https://www.hostmerchantservices.com

Payment processing can be confusing even for the experts in the industry. The system seems to be purposely designed to be difficult to understand even the most basic things, like what exactly your rate is and what fees are associated with accepting credit cards.

But accepting credit cards has become a necessity for businesses today. People are shifting toward a paperless society quickly, and online shopping has become a staple to even the most resistant consumer. As a business owner you need to become an expert on payment processing and do so quickly if you wish to keep ahead of the curve and not get burned by hidden fees and surcharges that cut directly into your profits.

Which credit card processing company should you get your merchant account from? Credit card processing fees, transaction fees, statements fees, PCI DSS fees, annual fees, all pile up. And these fees vary a lot from processor to processor.

Today, The Official Merchant Services Blog is going to give our faithful readers a quick and effective guide on how to compare and evaluate credit card processing companies.

Not All Processors Are Alike

There are many processors that offer merchant accounts and let small, medium and large businesses accept credit cards in brick and mortar locations as well as online through their website. There’s even a huge push today for mobile payments — letting merchants accept payments directly through their mobile phone from just about anywhere. With the wide variety of options, business owners may feel overwhelmed when trying to find the processor that suits them best.

Finding a processor and getting a merchant account isn’t easy.

For starters, the card associations — Visa, MasterCard, Discover and American Express — all have their own rate sheets know as Interchange Reimbursement Fees. These fees make up the majority of what a merchant pays to their processor and they vary greatly depending on the card type accepted. The rates and categories are complex, and confusing to follow for just one of the card companies. All of them together combine to make a maze of fees and categories that most merchants get lost in.

Second, many banks don’t offer merchant accounts directly to small businesses, so those businesses need to go through third party providers for a merchant account. These third party processors have different fee structures among themselves and different rules. So business owners face a lot of confusing variety from both the card association as well as the processor.

To add even more layers to this, businesses that process credit card orders online need to pass their transactions through an online gateway system. Whatever shopping card software is used has to interface with that gateway, so integration from shopping cart to gateway to processor is extremely important.

So let’s dig right in and see what’s what from the processor side of things.

First: Their Rates and Fees

For payment processors, a variety of things about you and your business can influence the discount rate and various fees they charge you for accepting charge cards as payment. Some of those factors include:

The number of years you’ve been in business

The percentage of your sales that are made over the phone or the internet

The type of business you are in

Your personal credit rating

The average dollar amount of each sales transaction

Your monthly sales volume

Keeping all of that in mind, discount rates tend to range from 2.24 to 3 percent for home run and small businesses that accept Mail Order/Telephone Order transactions. These transactions are higher risk and carry higher fees. To find out more, read our knowledge base article on MO/TO.

You’ll find in your search for a processor, however, that many processors advertise discount fees less than 2 percent. These lower fees are for swiped transactions — sales made by running the customer’s credit card through a machine. These card present transactions are more secure and much less risky so fees and penalties tend to be much lower. And online transactions through secure payment gateways also carry less fees and penalties than card-not-present transactions. Keep all that in mind when comparing pricing and rates between offers from payment processors.

Another key to rates and pricing was touched on before by The Official Merchant Services Blog when we compared Tiered Pricing to Cost Plus Pricing. To recap, Cost Plus Pricing tends to end up costing the merchant less because the merchants don’t get dinged for higher surcharges from other rate buckets. So a tiered pricing rate offer will seem lower than it actually ends up being.

Second: Other Fees

The discount rate isn’t the only fee to consider when comparison shopping. Business owners should also consider the application fees, the initial cost of equipment, per-transaction fees (a fee you pay on top of the discount rate for each transaction you process), monthly minimums that affect your fees, voice verification charges, address verification fees (if extra), monthly statement fees and any other added costs a processor will charge you. Something to always keep in mind, processors are very flexible in how they present your proposal and they could offer you a much lower discount rate with a higher per-transaction fee if your average ticket price is low but your transaction volume is high.

Also pay close attention to the cost of equipment and/or software for processing the transactions. Equipment can vary in cost between different processors by hundreds of dollars, even for the exact same piece of equipment. Merchants should try their best to not lease equipment or software. Buy the items outright. By leasing a credit card terminal you lock yourself into a term-contract that may not be something you can cancel without a heavy penalty. And you pay more for the item than its actual cost in the long run.

Third: Read the Fine Print

Be sure to read all application forms and contracts presented to you very carefully. Read all of the small print. Some processors will attempt to charge you if you want to stop processing charges through them in less than two or three years — termination fees. That termination fee can also be completely separate from any penalties you incur when canceling a lease of a terminal. If you plan to do a lot of MO/TO, pay careful attention to what the contract says about the percent of transactions you can process as phone orders (non-swiped). What the salesman says to you during the pitch process may not be what the application actually says because the offer is being given to you at a best case scenario and isn’t taking into account details like added surcharges for card-not-present transactions. At the end of the day, the contract carries the weight over the salesman’s pitch.

Also take into consideration what conditions the company can terminate your account and whether or not there are monthly minimums and maximums. Much of the juggling between different rate buckets in a tiered pricing proposal hinges on being able to surcharge you for details like exceeding a monthly maximum or failing to reach a minimum.

Fourth: The Application Process

Some companies will eagerly attempt to send a representative directly to your place of business — including your home if that’s where you do your business from. Part of this is to pitch the services to you in person. But another part is to be present on site, and to take a photograph of your location. This is part of the application process and is done to verify that you are at the location you say you are. Some other companies can do online site surveys or accept photos and information you yourself provide.

During the process of applying for a merchant account you should be prepared to furnish these items to the company:

A copy of your business license or certificate of doing business

Your driver’s license

Profit and Loss Statements

Copes of previous years’ tax returns

A photo of your office

All processors require two-way access to your bank account once you are accepted. This allows the processor to deposit funds into your account and also allows them to withdraw funds if there are chargebacks.

Comparison: Host Merchant Services

Just for comparison’s sake, here’s quick rundown of Host Merchant Services in the context of the tips we just provided you.

Host Merchant Services offers cost plus pricing. This is transparent pricing where we show and explain all of the fees you are charged. The company also guarantees to offer you the best rate, claiming that if the company can’t save a merchant money they will give them a $100 gift card for their time. And the company guarantees that it will not raise its merchant’s rates. Ever.

The company has no hidden fees. Host Merchant Services also cuts off a lot of the fees that other processors charge — there’s no annual fee, no application fee, no monthly minimums, and the lowest PCI Fee int he industry.

The company provides free equipment — both a credit card terminal and receipt paper.

Host Merchant Services provides customer support for integration of payment gateway services. The company has a variety of gateway options that will integrate with almost all of the shopping carts out there — and will help its merchants get integrated. HMS also offers its own in-house gateway with no transaction fees and full AP for custom integration with any software package.

Today we just want to remind all of our readers and subscribers of the upcoming Host Merchant Services webinar. On Tuesday June 12, 2012, at 10 a.m., CEO Lou Honick will be giving a 30-minute presentation on the Host Merchant Services Partnership Program as well as a quick introduction on how credit card processing works. After the presentation there will be a 10-minute Q&A period. The webinar is absolutely free to any and all interested in attending.

You can find the registration form here AT THIS LINK.

As stated before this webinar focuses on the partnership program — a bold offering from Host Merchant Services where we help businesses make money by sharing revenues with them from referrals they bring to us. The system goes beyond the normal lead-referral system, giving the partners potential for a much larger share of the revenue. HMS does all the work on its own to set up the partner’s customers for credit card processing. Host Merchant Services provides the partner’s customers with a complete payment processing and financial transaction service quickly and easily. Once the customer has their merchant account set up and has begun processing, the partner then begins to earn a steady and consistent stream of shared revenue with each and every monthly processing statement.

Or you can Register for the Free Webinar and get walked through the entire process, see how the partnership works, and learn about how Host Merchant Services will make you money and keep your customers happy.

This is the latest installment in The Official Merchant Services Blog’s Knowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s terms are Revenue Share and Strategic Partnership.

Revenue Share

At its most general definition, Revenue Sharing refers to the sharing of profits among different groups. One form shares between the general partner(s) and limited partners in a limited partnership. Another form shares with a company’s employees, and another between companies in a business alliance.

When applied to the Payment Processing Industry, revenue sharing is a bit more specifically involved in a cost per sale sharing of profits and accounts for about 80% of affiliate compensation programs. E-commerce web site operators using revenue sharing pay affiliates a certain percentage of sales revenues generated by customers whom the affiliate refer via various advertising methods. Another form of online revenue sharing consists in people working together and registering online in a way similar to that of a corporation, and sharing the proceeds.

A third form of revenue sharing on the internet consists of enticing internet users to sign up and create content by offering a share of advertising revenue.

Strategic Partnership

A strategic partnership is a formal alliance between two commercial enterprises, usually formalized by one or more business contracts but falls short of forming a legal partnership or, agency, or corporate affiliate relationship. Typically two companies form a strategic partnership when each possesses one or more business assets that will help the other, but that each respective other does not wish to develop internally.

The Official Merchant Services Blog has some breaking news to report. Host Merchant Services is offering its very first Webinar. On Tuesday June 12, 2012, at 10 a.m., CEO Lou Honick will be giving a 30-minute presentation on the Host Merchant Services Partnership Program as well as a quick introduction on how credit card processing works. After the presentation there will be a 10-minute Q&A period. The webinar is absolutely free to any and all interested in attending.

You can find the

registration form here AT THIS LINK.

What is the Partnership Program?

The Partnership Program that Host Merchant Services has devised is a way for businesses to expand their monthly revenue through referrals. It goes beyond the normal lead-referral system however, and as such gives the partners a larger share of the revenues. With the Host Merchant Services partnership program, HMS helps its potential partners earn monthly revenue through the business transactions of their very own customers. HMS does all the work on its own to set up the partner’s customers for credit card processing. The company provides the partner’s customers with a complete payment processing and financial transaction service quickly and easily. Once the customer has their merchant account set up and has begun processing, the partner then begins to earn a steady and consistent stream of shared revenue with each and every monthly processing statement.

Happy Customers are the Key

Host Merchant Services makes it easy for its partners to find leads and generate revenue. The company does this through the features of its HMS Guarantee. Each lead a partner brings to Host Merchant Services is offered these features:

Great Rate. HMS saves its customers money on their processing. The company pledges that if it can’t save one of its partner’s referrals money on processing, the company will give that referral a $100 Gift Card for their time.

Great Service. Host Merchant Services is about bringing trust to the payment processing industry and the company strives to go the extra mile with its commitment to superior customer service. The company has live people available 24x7x365 to take technical support and customer service calls. As company CEO Lou Honick says, “We pledge that if our customers have a problem, we will fix it.”

No Hidden Fees. Host Merchant Services offers a pricing model that has no annual fee, no application fee, no monthly minimums and the lowest PCI Fee in the industry.

Lifetime Rate. Host Merchant Services offers a straightforward “cost plus” pricing model and the rate is guaranteed. The company grandfathers that rate and will not raise it. The only time the rates change is when the card associations — MasterCard, Visa and Discover — raise the rates for everyone.

No Contracts. Host Merchant Services does not lock its customers into a term contract or charge them early termination fees. As CFO Dan Honick likes to say, “Our customers stay with us because they are happy with our service.”

This combination of features adds plenty of enticement to a partner’s customer base to add Host Merchant Services as its credit card processor. Making Host Merchant Services a reliable company for the partner to refer to its customer base. Host Merchant Services does all of the work to set the referral up with a merchant account, to install a robust payment processing solution, and to keep the customer happy with superior customer service month after month. It’s a safe and easy way for a business to add more revenue to its bottom line each month.

For More Information

You can visit our Partnership FAQ Page HERE AT THIS LINK to get more information. Or contact the company at 1-877-571-4678.

Or you can Register for the Free Webinar and get walked through the entire process, see how the partnership works, and learn about how Host Merchant Services will make you money and keep your customers happy.

Today The Official Merchant Services Blog is going to get a bit personal, for me at least. I’m going to take a moment to talk about print media, and its withering industry. Or, think of it this way: I’ll be talking about the rise to power of E-Commerce — the industry that has helped deliver excruciating body blows to print media over the past decade, knocking it to the mat time and time again.

My history with print media goes back. Way back. All the way back to the beginning of my own career. I’ve worked for four different newspapers, the most high profile being the Asian Edition of the Wall Street Journal at the turn of the millennium. I’ve illustrated various comic strips and published my own comic book. I’ve worked for a printing company in Delaware. Along the way I’ve essentially learned how to make a printed publication from beginning to end; the only skill I lack is the ability to actually push the buttons on a printing press. But every other step, from concept to creation to pre-production to layout and design to editorial to post production I’ve done during my career.

And all of these skills are endangered because of E-Commerce. (Well not really; most the skills translate easily into the virtual media world which is why I’ve been able to transition my career; but everything involving production kind of gets tossed out the window, replaced with skills revolving around web safe colors, pixel sizes and screen ratios).

A really vast, somewhat oversimplified recap of the internet’s impact on newspapers, comic books and book publishing can be summed up by my own career. One of the companies I used to work for, Gannett (publisher of the USA Today), used to have an empire built on small to mid-size suburban community newspapers. They were everywhere. Including Lansdale, PA — where I worked for a time. Gannett was slow to embrace online news though. And the transition from the late 1990s to the aughts left Gannet in a position to streamline and essentially drop a lot of those small and mid-size papers from its stable.

At the same time, I was trying my best to get some traction going in my quest to be a freelance illustrator for comic books. Things didn’t quite work out. I never became the regular artist on The Flash or Spider-man like I dreamed of doing when I was younger. I did however get paid for doing a few projects and got quite a bit of my art published.

Still, steady work was hard to find. And the comic book industry appeared to be dying because of the problems that all of print media now faced.

The major publishers (DC Comics and Marvel Comics) were no longer selling millions of copies of their books. In fact, sales these days are horribly low, with top books barely cracking 100k in sales volume. This reduction in volume can be linked to its distribution channel. Comics stopped appearing in mainstream outlets because the sole distributor of the material, Diamond, only catered to specialized direct market hobby shops (comic book shops). You couldn’t find them at the local supermarket or the local 7-11 anymore. The comic book “rack” was gone. I’d go so far as to make the claim that today, in 2012, the two major comic book companies are really just stables for intellectual properties. Disney and Time Warner wanted Marvel and DC not so much for their ability to publish millions of paper periodicals every month. Instead they wanted the comic book companies for the properties that could at any moment be turned into $100 million blockbuster movie franchises.

So the comic book industry ended up being sold as a niche hobby, and stopped being made as a mass medium periodical. Big companies bought the two biggest publishers of those comics just to keep the ideas and licensing on ice for future movie potential. Print media, it is dying.

And then then there was the issue with comic strips. Newspapers shrunk the comics section over decades. When Action Comics first appeared in newspaper print in thge 1940s, the comic strip took up half a broadsheet, which back then was much larger than the broadsheet sizes for newspapers of today. But by the time Bill Watterson and Gary Larson gave up on two of the most popular comic strips of all-time (Calvin and Hobbes and The Far Side), the newspaper strip had shrunk to 3 tiny postage stamp sized panels shoved into the back end of the feautres/lifestyle sections of most papers.

Then the internet hit newspapers big time, as people went online for their news. They got the stories for free. And newspapers could no longer compete. Comic strips were a casualty of that shift in media.

So right now, survival instinct is kicking in for the comic art form. The internet allows both the strip and the comic book format room to breathe, and easier distribution. Penny Arcade is what I feel to be the best example of the modern comic strip, giving renewed life to the art that newspapers were choking out of their shrinking pulp empire. Penny Arcade can publish in color (because it’s online), can publish unorthodox sizes (because it’s online) and offer their content for free (online). They then make a killing selling collected editions (many sales being made … online) of the same content daily readers get for free. They adapted and brought the art form onto a new stage. Meanwhile … print media continues to not adapt.

Comic Books are starting to finally embrace the changing landscape. ComiXology offers Marvel, DC and independent publishers through their mobile application. You can purchase and download all of your favorite comic books directly to your iPhone, Android, iPad or Kindle. You no longer need to go to direct order hobby shops. Your comic books no longer need to take up physical space. They’re right there at your fingertips — your entire collection just a thumbtap away. While they may be a bit unwieldy and tiny on the smartphones, they look rather luxurious and eye-popping on a larger device like a Kindle (where, not so surprisingly, I’ve been reading my comic books in 2012).

That brings me to the Kindle — or more generally, the reader devices and THIS BLOG HERE from Michael Essany at Daily Deal Media. The article resonates with me. A number of my close friends used to work at Borders Books and Music in their twenties. Last year the local Borders closed up shop. And all we currently have in our local area is a Barnes and Noble located in the Christiana Mall.

The most striking thing about their store in the mall is when you walk in their front door you are immediately overwhelmed by their eBook section, with large signage telling you all about the Nook (their version of the Kindle).

That sight at my own local big box book store really drives home Essany’s second paragraph, when he writes, “Although many avid readers are mourning the noticeable loss of traditional big box and mom-and-pop book retailers, the economics of eCommerce and the popularity of eBooks are quickly dispatching publishing companies, paperback publications, and even print magazines to the trash receptacle of history.”

The point Essany is making was driven home even further when I attempted to make a quick trip to that Barnes and Noble for a book on a work-related topic: Web Design. I knew the right section of the store to go to, but couldn’t find the title I was looking for. I used their interface terminal in the store to look that title up. Apparently it was in stock as an eBook. And I could order a regular print version of it from there, but had to order it as an online purchase and have it delivered to my house days later. The entire point of my trip was to get the book that day, otherwise I’d have gone online when I got home from work instead. So I kept browsing, and found every single book they had under the topic of web design was only available either through an online purchase or as an eBook.

E-Commerce is winning

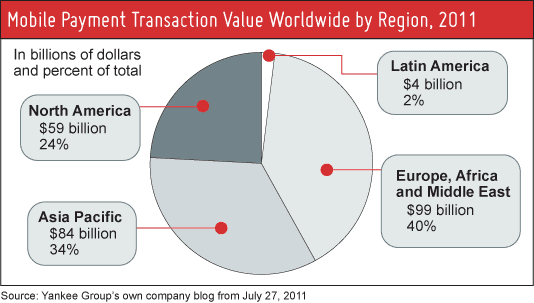

In terms of printed media E-Commerce is absolutely dominating. Essany cites a statistic to back up this outlook, writing that according to the Yankee Group (a research company we’ve cited ourselves when they made projections on The Future of Mobile Payments), consumers will purchase approximately 381 million eBooks next year with an average selling price of $7.

Most impressive

My own research for this very blog during last year’s holiday shopping season demonstrated what to me has become a very obvious aspect of the economy: shopping online is a common thing for people to do. That means E-Commerce is making buckets of money. Each one of those transactions are part of the payment processing industry. The foundation is there. People have found the convenience of shopping online so powerful that it outweighs the risk of fraud. So more and more people have taken to solving their shopping problems online. I know that I myself do this. It’s so much easier to look for a product online and know you’re getting what you want with a few clicks, than it is to go trudging out to a store that may or may not have the item you want.

Last year in a Blog Post about the upcoming holiday shopping season, I reported “A 2010 survey conducted by Google and OTX found that 35% of internet users start their holiday shopping prior to the end of summer, months ahead of Black Friday. This trend is only continuing to grow as consumers find online shopping convenient to their shopping habits, easy to do, and the wide selection lets them find great deals on price.”

This trend in shopper behavior combines with the rise of virtual media like eBooks like Voltron to form a very powerful lion-fisted, right-left combo to the solar plexus of Print Media’s crumbling empire.

And you know what? I’m OK with this.

I’m a voracious reader. But I’m also under the thrall of the convenience of online shopping. I truly do turn to the internet first for most products I’m interested in. This is heightened when I want to purchase a book, a magazine or a comic book. It’s just so much easier. The only time I’ve wanted to wander into a book store to buy a book was when I wanted it right then, with no wait on delivery. And I found the remnants of the only big chain bookstore in my local area to have already forced the decision upon me: If I wanted a book about web design, I needed to go directly to the web to get it.

I’ve been using the ComiXology app this year. And when the company that I once worked for (Valiant Comics) as a production intern returned to the comic book industry after a long hiatus, publishing a comic book I once did post production work for (X-O Manowar), I immediately jumped onto my phone to purchase it. I find that I read more web comic strips than I ever read in a newspaper. I find I go to the web for my news. Or my phone. I’ve even found myself reading straight up only published electronically eBooks this year. I still prefer printed books, but for me they’ll be online purchases. I’ll buy the collected editions of comics I like, but do so online. I’ll buy printed books of titles I really just want to curl up with and turn the pages of, but I’ll make the purchase online. It’s gotten so pervasive in my life that I now buy tickets to sporting events online, brands of tea I can’t find at my local supermarket online, all of my roller derby referee equipment and rules books online. I even bought my ticket to The Avengers on my phone through Fandango and had it delivered to my phone as a mobile ticket.

E-Commerce is where it’s at. And publishers of the written word need to embrace this shift. Maybe it’s easier for me to do so because I work in the payment processing industry and get to see firsthand how big and booming E-Commerce is.

This is the latest installment in The Official Merchant Services Blog’s Knowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works.

This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access.

Today’s terms are Level I, Level II and Level III Data.These terms are all related to Purchasing Card Data. There are different levels of data in the merchant account business. This three level system decides whether or not a transaction is qualified. When changes are implemented in the credit card processing industry, there are also changes in the regulations on how this data is processed, and it’s a good idea to know the difference between the various levels when thinking about data security and PCI Compliance.

Level I Data

Level I card data is typically associated with consumer transactions and limited purchase data returned to the cardholder. Level I purchasing card data includes the same information captured during a traditional credit card purchase transaction. This includes: total purchase amount, date, merchant category code and supplier/retailer name.

Level II Data

Level II purchasing card data includes the same information captured at Level I, plus the following: sales tax amount, customer’s accounting code, merchant’s tax ID number, applicable minority – and women-owned business status and sales outlet ZIP code. Level-2 data elements benefit the corporate/government/industrial buyer and can often be transmitted via a standard credit card point of sale terminal due to their restricted capabilities.

Level III Data

Level III purchasing card data includes the same information captured at Levels I and II, plus the following: quantities, product codes, product descriptions, ship to ZIP, freight amount, duty amount, order/ticket number, unit of measure, extended item amount, discount indicator, discount amount, net/gross indicator, tax rate applied, tax type applied, debit or credit indicator and alternate tax identifier. Level III is comprehensive line item detail. This data is equivalent to the information found on an itemized invoice, requires greater system capability which is provided through 3Delta Systems’ payment applications.

Interchange is a term used in the payment card industry to describe a fee paid between banks for the acceptance of card based transactions. Usually it is a fee that a merchant’s bank (the “acquiring bank”) pays a customer’s bank (the “issuing bank”).

In a credit card or debit card transaction, the card-issuing bank in a payment transaction deducts the interchange fee from the amount it pays the acquiring bank that handles a credit or debit card transaction for a merchant. The acquiring bank then pays the merchant the amount of the transaction minus both the interchange fee and an additional, usually smaller fee for the acquiring bank or ISO, which is often referred to as a discount rate, an add-on rate, or passthru.

For cash withdrawal transactions at ATMs, however, the fees are paid by the card-issuing bank to the acquiring bank (for the maintenance of the machine).

These fees are set by the credit card networks, and are the largest component of the various fees that most merchants pay for the privilege of accepting credit cards. Visa, Mastercard, and Discover are each known as card associations. And each card association has their own rate sheets known as Interchange Reimbursement Fees. These fees make up the majority of what you pay to your processor and they vary greatly depending on the card type accepted.

Interchange Plus pricing means that the acquirer charges you a variable MSC consisting of the cost price plus a fixed markup. Interchange Plus Pricing is exclusively how we quote at Host Merchant Services. Interchange Plus, also known as Cost Plus, pricing gives the customer a fixed rate over published Interchange Fees. This pricing format is normally quoted as a discount rate (percentage fee) along with a per item or authorization fee. The great thing about Interchange Plus pricing is that you always know exactly what you are paying to your processor to services your account. Think of Interchange, and all the associated fees, as an unavoidable cost. No matter who you process with, you have to pay these fees. They may be labeled differently, or wrapped up in a confusing pricing tier, but one way or the other, you are paying Interchange fees. By understanding the markup you pay over Interchange, you know exactly what you pay to your processor and exactly what is going to the card associations. That allows you to make a decision on whether or not the markup seems reasonable for the service you get and choose your processing partner accordingly.

Here’s a small graphic explaining the basics of how Interchange Plus works:

This is the latest installment in The Official Merchant Services Blog’s Knowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is:

Chargeback

Chargeback typically refers to the act of returning funds to a consumer. The action is forcibly initiated by the issuing bank of the card used by a consumer to settle a debt. Essentially what happens is a consumer disputes a transaction, and the credit card company’s bank responds by taking the money back from the Merchant and returning it to the consumer.

Customers dispute charges to their credit card usually when goods or services are not delivered within the specified time frame, goods received are damaged, or the purchase was not authorized by the credit card holder — the latter being the most common reason for a chargeback.

The chargeback mechanism exists primarily for consumer protection. To start a chargeback a consumer will contact their credit card company and ask for a chargeback. The dispute process then begins. During the dispute process he merchant will have to provide proof they rendered service properly. If the merchant can’t provide sufficient evidence, the credit card company debits the transaction amount from the merchant’s account and credits it to the consumer’s account. Additionally, the credit card company charges the merchant a chargeback fee as a penalty.

With each chargeback the issuer selects and submits a numeric reason code. This feedback can help the merchant and acquirer diagnose errors and improve customer satisfaction. The code also helps the merchant better investigate the transaction in order to find proof during the Dispute Process. Reason codes vary by bank network, but fall in four general categories:

Technical: Expired authorization, non-sufficient funds, or bank processing error.

Clerical: Duplicate billing, incorrect amount billed, or refund never issued.

Quality: Consumer claims to have never received the goods as promised at the time of purchase.

Fraud: Consumer claims they did not authorize the purchase or identity theft.

For transactions where the original invoice was signed by the consumer, the merchant may dispute a chargeback with the assistance of the merchant’s acquiring bank. The acquirer and issuer mediate in the dispute process, following rules set forth by the corresponding bank network or card association. If the acquirer prevails in the dispute, the funds are returned to the acquirer, and then to the merchant.

The merchant’s acquiring bank accepts the risk that the merchant will remain solvent over time, and thus has an incentive to take a keen interest in the merchant’s products and business practices. Reducing consumer chargebacks is crucial to this endeavor. To encourage compliance, acquirers may charge merchants a penalty for each chargeback received. Payment service providers, such as PayPal, have a similar policy. In addition, Visa and MasterCard may levy severe fines against acquiring banks that retain merchants with high chargeback frequency. Acquirers typically pass such fines directly to the merchant. Merchants whose ratios stray too far out of compliance may trigger card association fines of $100 or more per chargeback.

For More Information

To find out more about Chargebacks and to gain some Chargeback Tips, be sure to CLICK HERE and read The Official Merchant Services Blog entry from January 9, 2012.

Host Merchant Services finally gets to make this announcement official: All mobile payment solutions the company offers now feature both iPhone and Android compatibility.

On February 28, 2012 Host Merchant Services teased through its Facebook Page that it would have big news regarding HMS and Mobile Payments in March. But technical difficulties with the full release of Payfox’s Android solution held the news back until today. In the Android Marketplace, Payfox is now listed and available for download. You can see the listing here.

The App has been on the Android Marketplace since March 21. But now the rest of the support is in place to get the app working. The final piece of the puzzle was the card reader — UniMag II, Two-Track Secure Mobile MagStripe Reader. The device is a two-track, encrypted magnetic stripe reader that works with a wide variety of mobile platforms, including Apple, HTC, LG, Motorola, and Samsung devices. Use your mobile device to read credit cards, signature debit cards, gift cards, loyalty cards, driver’s licenses, and ID badges. The UniMag reads up to 2 tracks of information with a single swipe in either direction, providing superior reading performance for your mobile device. A merchant account is required to accept credit card transactions.

You can download the specs from the UniMag II data sheet right here. These are the Android devices supported by the reader:

HTC Aria

HTC Desire Z

HTC Eris

HTC EVO 4G

HTC EVO Shift 4G

HTC G2

HTC Hero

HTC Incredible

HTC MyTouch 4G

HTC EVO 3D

HTC Nexus One

HTC Incredible 2

HTC MyTouch 3G Slide

HTC MyTouch 4G Slide

HTC Thunderbolt

HTC Merge

LG Optimus T

LG Revolution

Motorola Droid 2

Motorola Droid X

Motorola Droid Pro

Motorola Milestone

Motorola FlipSide

Motorola Atrix

Motorola Droid 2

Motorola Droid 2 Global

Motorola Droid Bionic

Motorola Droid 3

Samsung Captivate

Samsung Droid Charge 4G

Samsung Epic

Samsung Epic 4G

Samsung Fascinate

Samsung Nexus S

Samsung Replenish

Samsung Infuse 4G

Samsung Continuum

Samsung Galaxy SII

Please Note

When you go to the Google Play Market and search for PayFox using your Android/Droid phone, the PayFox application will only display for those devices for which the application itself is compatible.

Red 5 Standing By

Our friends at Transfirst also wanted to offer some clarification about the use and licensing around the word Droid:

“Android and Droid are often used interchangeably when referring to ever-growing & increasingly popular line of smartphones that run on Google technology. The difference, for most purposes, is one of legal definitions and intellectual property. Android simply refers to the operating system and software that powers phones built by any of number manufacturers, including HTC or Motorola, and that run on any of the major carriers.

Droid, on the other hand, is a term coined and owned by LucasFilm Ltd., the licensing rights for which Verizon had to purchase in order to brand their specific line of Android Smartphones.”

In short, Androids are phones, and you can now use them to swipe payments. Droids are what Jawas scavenge. Though I’m sure the Jawas will happily accept mobile payments from all you moisture farmers out there. Ootini!

{kind=link}