The Official Merchant Services Blog tackles the topic of Debit Card processing today. While the blog has extensively delved into the Durbin Amendment and the affects the legislation is having on merchants, one topic we’ve overlooked is Debit Card processing –– specifically PIN Debit vs. Swipe Debit.

Difference Between Credit, Debit, and Check Cards

First thing we need to do is define debit cards. True debit cards can only be accepted when a merchant is able to accept a personal identification number (PIN) from customers using a PIN pad. So for true debit cards, the only option is PIN Debit.

Buttransaction processing has been evolving. Most debit cards today are actually check cards that are mistakenly referred to as “debit cards.” The difference between a debit card and a check card is that a check card has a Visa or MasterCard logo in the lower right-hand corner where a true debit card does not. These cards are hybrids and can work as either a credit card or a debit card when used in a transaction. Amerchant account allows a merchant to accept debit, credit and check cards.

Price Comparison

Prior to the Durbin Amendment taking affect, PIN Debit was the most cost effective choice for debit card/check card transactions. Swipe, or Signature-based, debit transactions carried higher interchange ratesthan PIN debit transactions for many years.

Once the Durbin Amendment took affect on October 1, 2011, the fees for both PIN Debit and Signature Debit were balanced. Swipe Debit now costs as much as PIN Debit for banks that are capped by the Durbin legislation. Swipe Debit is also, in rare cases, less expensive than PIN Debit in situations where the bank is exempt from Durbin rules. The change that the Durbin Amendment brought on has many merchants asking the question: If Signature and PIN debit are now capped at the same interchange fee, do I still need my PIN Pad?

Continue Reading – PIN Debit vs. Swipe Debit, Part 2

On the last day of September, Durbin Amendment Eve if you will, The Official Merchant Services Blog is about ready to end its Countdown to Durbin Series. Today we take a look at the big news that has the media buzzing.

Bank of America Reacts to Durbin

Bank of America, the largest bank in the country going by deposits, announced it is going to begin charging its customers a $5 monthly fee to use debit cards. The bank will begin charging the fee next year for the bank’s basic checking accounts. It will apply only to debit card purchases and not to ATM withdrawals, online bill payments or mobile phone transfers, the company said.

Consumer Backlash and Cut Up Cards

Bank of America announced this change, which will take effect for its customers in 2012, and were soundly slammed with negative feedback. Our first link comes from Fox Business Network, where Gerri Willis cut up her debit card on the air in reaction to the news from Bank of America. “Right here, right now, I’m going to show Bank of America what I think of their fees,” she said before using a pair of scissors on her card.

Durbin Slams Bank of America

Our next link comes from The Washington Post. It picks up the topic, mentioning what Willis did on the air. It then offers Bank of America’s defense of this new fee, stating that the bank is doing this to recoup losses that will come from the cap on debit card swipe fees that the Durbin Amendment will put into place tomorrow on October 1. Then the article quotes Senator Dick Durbin: “Bank of America is trying to find new ways to pad their profits by sticking it to its customers,” Durbin said in a statement Thursday. “It’s overt, unfair, and I hope their customers have the final say.”

Bank of America Already in Crisis

While this move was quite predictable, and falls into line with Host Merchant Services’ previously published analysis of how banks will react to the Durbin Amendment, the news is quite incendiary because of Bank of America’s current situation. Which is mentioned in the third article we highlight on Bank of America, by Fox News: “the Bank of America decision drew outrage for several reasons. The company is the largest U.S. bank by deposits. And it reaped $45 billion in federal bailout money — receiving the first chunk in 2008 and the rest in 2009 to cope with losses at Merrill Lynch. “

The article also mentions that Bank of America did pay back the government all of the bailout money.

Bank of America a Microcosm of Durbin’s Impact

A fourth article, from the Christian Science Monitor, sums up quite succinctly how this news is quite standard Durbin Amendment fallout: “So in other words, Bank of America is shifting a part of the fee obligation from merchants to customers.”

As we’ve seen in the ongoing Countdown to Durbin series, this is one of the most expected moves that banks are making. Shifting the burden of the fees away from merchants and putting it squarely on the shoulders of the consumers. This avoids the scope of the Durbin Amendment’s regulations and lets the banks continue to reap profits from the billion dollar payment processing industry.

Rounding out the coverage of Bank of America and its announced monthly debit fees we find:

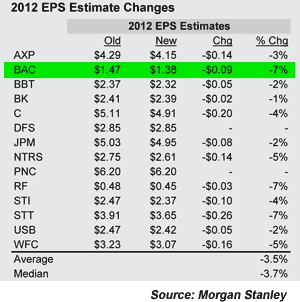

This chart, while the story states is not entirely tied to Bank of America’s recent announcement or to the Durbin Amendment, does show that banks will be affected by the Durbin Amendment. They will have to make changes to deal with the losses they expect to take from a hard cap on fees that they were profiting from, and if Bank of America is any indicator, the burden of those changes will go from the merchants who used to get hit with the swipe fees to the consumer who will now have to pay more to support the use of debit cards.

The Official Merchant Services Blog once again takes up the task of analyzing the media reports revolving around the Durbin Amendment and the changes it will bring to how banks do business with their customers because of its cap on debit card swipe fees. We continue to use Host Merchant Services‘ own analysis as the foundation of the comparisons we make regarding other media sources and their take on the legislation and its impact.

Durbin on Durbin

The first article comes from a Chicago-based radio station WLS 890 AM. It’s an interesting read because it quotes the legislation’s namesake, Senator Dick Durbin from Illinois. It’s one of the few articles that includes Durbin’s perspective on the legislation as we get closer to the October 1 date of when the law takes effect. The article begins with a brief explanation of what Durbin sought to do with the legislation:

“Sen. Dick Durbin told reporters Tuesday afternoon that the debit card fees retailers have to pay will go down Saturday thanks to the Durbin Amendment.”

It then offers a lively retort from J.P. Morgan Chase executive Jamie Dimon: “The big boss at J.P. Morgan Chase, Jamie Dimon, calls this ‘price fixing at its worst’ that will surely cause banks to raise fees on customers with deposit accounts. “

While many of the articles on this amendment have been dancing around the confrontation between consumers and banks over the Durbin Amendment this article dives right into the rhetoric, giving it a much more active tone for the reader and an insight into the debate that framed and spawned the legislation. It helps that the article ties this confrontational perspective into the legislation’s author and Durbin’s motivation for working on the amendment. Citing a letter that Durbin wrote to Dimon back in April, the article states: “Durbin said to Dimon, ‘Your industry is used to getting its way with many members of Congress and with your regulators. The American people deserve to know the real story about the interchange fee system and the ways that banks in general — and Chase in particular — have abused that system.’ “

But the basic conclusion is pretty much the same as the other articles focusing on the amendment and what changes it will bring on October 1. The conclusion is that banks will react by creating more fees for their customers and just recouping the losses from the swipe fee cap in other areas not covered by the legislation. Durbin is quoted in the article, calling that tactic “indefensible” but conceding it is the likely outcome of the amendment. The article sums it up: “So what the government giveth, the banks may take away.”

The Cost of Doing Business

The next article we look at is an Associated Press piece located on Bloomberg’s website. It’s a report that reveals how much money American Express spent in the second quarter of this year to lobby Congress and fight against the implementation of the Durbin Amendment.

“American Express Co. spent $610,000 in the second quarter to lobby the federal government on rules involving the fees charged to merchants for processing payments and other issues, according to a disclosure report.”

The article notes that the company spent the same amount of money in the previous quarter of 2011, but that they spent 3% more money in the second quarter of 2010 comparatively. The article also notes that Amex doesn’t offer debit card services, but does offer interchange services on credit card payments, suggesting that was the reason it spent money to lobby Congress on the topic. The money wasn’t solely spent on lobbying against the Durbin Amendment. And the article notes that: “Amex representatives also lobbied the federal government on legislation involving online tracking of consumer behavior and the protection of personal information, cyber security, financial regulatory reform, consumer financial protection and issues related to reloadable prepaid cards, patent reform, tax reform and reform of the U.S. Postal Service.”

So what we see in today’s Countdown to Durbin is a look at how heated the debate still is between the legislation’s namesake and the big banks that are targeted by the reform. The intensity of this debate was such that American Express even spent more than $600,000 in a single quarter to lobby against it in 2011.