For artists and designers, Etsy is no less than a blessing. It is the best place for creative people to turn their hobbies into an online business. With Etsy, sellers don’t have to worry about paying any rent, taking care of inventory, or even hiring employees to manage their store.

Sellers on Etsy can only focus on making creative designs. They don’t need to know how to make a website or market their products to people. Etsy does it all for them.

However, one problem that many sellers face with Etsy is their complex fee structure. We will break down all the different types of Etsy fees so you can have a clear idea of the cost involved before starting your online store on Etsy.

The Standard and Plus Plans on Etsy

The standard plan does not cost anything monthly. However, there are additional listing fees, payment processing fees, delivery fees, and many other kinds of fees that you need to pay.

The plus account would cost sellers $10/month. You get all the advantages of the standard plan along with some additional benefits.

Some of the additional benefits are:

15 free listings monthly (worth $3)

$5 Etsy ads credit

Special discounts on custom domains

Additional tools for better shop customization

Various Fees that Etsy sellers have to pay

Etsy requires the sellers to pay fees for various purposes. Some of the charges are flat fees, while others are percentage-based. We will talk about all of them so you can estimate the cost of running an Etsy store.

Listing Fees

The fee for listing each item on Etsy is $0.2. It doesn’t mean that you can sell multiple identical items for just one listing fee of $0.2. For example, if you are selling five identical signboards on Etsy, you would have to pay a listing fee of $1 combined for them.

Transaction Fees

Transaction fees in Etsy are different from what sellers pay for payment processors. Transaction fees of 5% per sale are Etsy’s commission for using their platform. The transaction fees don’t cover wrapping and product customization.

There is also a shipping transaction fee that sellers need to pay. The charge is 5% of the shipping price.

You don’t have to pay 5% fees on your sales tax if you are from the USA or Canada. For sellers from other countries, additional charges may be applicable on sales tax.

Payment Processing Fees

Etsy has payment processors you will use if you belong to one of the 36 eligible countries that support the system. The fee for each Etsy payment processing is 3% of the total payment plus $0.25.

If you are not from one of the 36 eligible countries, you can use PayPal or Square, which typically costs 2.9% plus $0.30 processing for each payment.

Etsy Pattern Fees

If you are looking to create an online store, you should check out Etsy Pattern. It costs $15/month and allows you to list products for free for an unlimited time.

The pattern store links with your Etsy seller account. You can also try it for free for 30 days to see if it suits your needs.

Square In-Person Selling Fees

Etsy has teamed up with Square to provide sellers an option to collect in-person payment. It is necessary to own a square card reader to be eligible for this option.

Everything is like usual, except instead of the 5% transaction fees, you would be paying Square processing fees. For each transaction, the Square processing fee is 2.6% plus $0.10.

Currency Conversion fees

Sellers should set the listings in the same currency as their payout currency. However, if sellers don’t do that, the cost of currency conversion is 2.5% of the total amount.

You can also avoid this if you are using PayPal as a payment processor.

Etsy Ad Fees

You can choose to market your listings on Etsy using in-house ads. The cost for advertisement follows a pay-per-click system. The PPC is determined depending on the demand of the ad space. Sellers have the option to set a maximum budget for each day. The ads would stop running when that budget is reached.

Offsite Etsy Ads

The Etsy offsite ads are a new feature for all to use. It is mandatory for all sellers, and the only sellers who are given the option to opt-out who made sales less than $10,000 in a year.

The ads are displayed on platforms like Facebook, Google, Bing, and others. The sale counts if someone clicked on an ad for one of your products and buys products from your online shops.

The fees for these ads can be between 12% and 15%, depending on your sales. For sellers crossing annual sales of $10,000, the fee is 15%, while sellers who make sales below that have to pay 12% advertising fees.

How can you start your online store on Etsy?

After knowing all the associated fees and you are still willing to open an online store with Etsy, you will need the following things.

Etsy Account

You would need to create an Etsy account. It can be a standard or a plus account. You can then choose the currency for your shop, the name of the shop, and set up other preferences.

Products

You should have products available to list on your Etsy shop. To make an Etsy listing, you would need product photos, title, and product description.

Billing Account

You need to verify your billing account to confirm your identity and also allow Etsy to charge your fees automatically.

Payment Account

You can use Etsy’s payment processor, or you can choose other payment processors like PayPal and Square. It is also possible to use the mail to receive payments as checks from your customers.

Conclusion

Etsy takes care of the many needs of creative design sellers, but are the fees they charge worth it? Is it better to sell on eBay? Those are answers that you have to find for yourself. We hope that our breakdown of Etsy fees helped you get a clear picture of what you would manage.

Today The Official Merchant Services Blog is going to get a bit personal, for me at least. I’m going to take a moment to talk about print media, and its withering industry. Or, think of it this way: I’ll be talking about the rise to power of E-Commerce — the industry that has helped deliver excruciating body blows to print media over the past decade, knocking it to the mat time and time again.

My history with print media goes back. Way back. All the way back to the beginning of my own career. I’ve worked for four different newspapers, the most high profile being the Asian Edition of the Wall Street Journal at the turn of the millennium. I’ve illustrated various comic strips and published my own comic book. I’ve worked for a printing company in Delaware. Along the way I’ve essentially learned how to make a printed publication from beginning to end; the only skill I lack is the ability to actually push the buttons on a printing press. But every other step, from concept to creation to pre-production to layout and design to editorial to post production I’ve done during my career.

And all of these skills are endangered because of E-Commerce. (Well not really; most the skills translate easily into the virtual media world which is why I’ve been able to transition my career; but everything involving production kind of gets tossed out the window, replaced with skills revolving around web safe colors, pixel sizes and screen ratios).

A really vast, somewhat oversimplified recap of the internet’s impact on newspapers, comic books and book publishing can be summed up by my own career. One of the companies I used to work for, Gannett (publisher of the USA Today), used to have an empire built on small to mid-size suburban community newspapers. They were everywhere. Including Lansdale, PA — where I worked for a time. Gannett was slow to embrace online news though. And the transition from the late 1990s to the aughts left Gannet in a position to streamline and essentially drop a lot of those small and mid-size papers from its stable.

At the same time, I was trying my best to get some traction going in my quest to be a freelance illustrator for comic books. Things didn’t quite work out. I never became the regular artist on The Flash or Spider-man like I dreamed of doing when I was younger. I did however get paid for doing a few projects and got quite a bit of my art published.

Still, steady work was hard to find. And the comic book industry appeared to be dying because of the problems that all of print media now faced.

The major publishers (DC Comics and Marvel Comics) were no longer selling millions of copies of their books. In fact, sales these days are horribly low, with top books barely cracking 100k in sales volume. This reduction in volume can be linked to its distribution channel. Comics stopped appearing in mainstream outlets because the sole distributor of the material, Diamond, only catered to specialized direct market hobby shops (comic book shops). You couldn’t find them at the local supermarket or the local 7-11 anymore. The comic book “rack” was gone. I’d go so far as to make the claim that today, in 2012, the two major comic book companies are really just stables for intellectual properties. Disney and Time Warner wanted Marvel and DC not so much for their ability to publish millions of paper periodicals every month. Instead they wanted the comic book companies for the properties that could at any moment be turned into $100 million blockbuster movie franchises.

So the comic book industry ended up being sold as a niche hobby, and stopped being made as a mass medium periodical. Big companies bought the two biggest publishers of those comics just to keep the ideas and licensing on ice for future movie potential. Print media, it is dying.

And then then there was the issue with comic strips. Newspapers shrunk the comics section over decades. When Action Comics first appeared in newspaper print in thge 1940s, the comic strip took up half a broadsheet, which back then was much larger than the broadsheet sizes for newspapers of today. But by the time Bill Watterson and Gary Larson gave up on two of the most popular comic strips of all-time (Calvin and Hobbes and The Far Side), the newspaper strip had shrunk to 3 tiny postage stamp sized panels shoved into the back end of the feautres/lifestyle sections of most papers.

Then the internet hit newspapers big time, as people went online for their news. They got the stories for free. And newspapers could no longer compete. Comic strips were a casualty of that shift in media.

So right now, survival instinct is kicking in for the comic art form. The internet allows both the strip and the comic book format room to breathe, and easier distribution. Penny Arcade is what I feel to be the best example of the modern comic strip, giving renewed life to the art that newspapers were choking out of their shrinking pulp empire. Penny Arcade can publish in color (because it’s online), can publish unorthodox sizes (because it’s online) and offer their content for free (online). They then make a killing selling collected editions (many sales being made … online) of the same content daily readers get for free. They adapted and brought the art form onto a new stage. Meanwhile … print media continues to not adapt.

Comic Books are starting to finally embrace the changing landscape. ComiXology offers Marvel, DC and independent publishers through their mobile application. You can purchase and download all of your favorite comic books directly to your iPhone, Android, iPad or Kindle. You no longer need to go to direct order hobby shops. Your comic books no longer need to take up physical space. They’re right there at your fingertips — your entire collection just a thumbtap away. While they may be a bit unwieldy and tiny on the smartphones, they look rather luxurious and eye-popping on a larger device like a Kindle (where, not so surprisingly, I’ve been reading my comic books in 2012).

That brings me to the Kindle — or more generally, the reader devices and THIS BLOG HERE from Michael Essany at Daily Deal Media. The article resonates with me. A number of my close friends used to work at Borders Books and Music in their twenties. Last year the local Borders closed up shop. And all we currently have in our local area is a Barnes and Noble located in the Christiana Mall.

The most striking thing about their store in the mall is when you walk in their front door you are immediately overwhelmed by their eBook section, with large signage telling you all about the Nook (their version of the Kindle).

That sight at my own local big box book store really drives home Essany’s second paragraph, when he writes, “Although many avid readers are mourning the noticeable loss of traditional big box and mom-and-pop book retailers, the economics of eCommerce and the popularity of eBooks are quickly dispatching publishing companies, paperback publications, and even print magazines to the trash receptacle of history.”

The point Essany is making was driven home even further when I attempted to make a quick trip to that Barnes and Noble for a book on a work-related topic: Web Design. I knew the right section of the store to go to, but couldn’t find the title I was looking for. I used their interface terminal in the store to look that title up. Apparently it was in stock as an eBook. And I could order a regular print version of it from there, but had to order it as an online purchase and have it delivered to my house days later. The entire point of my trip was to get the book that day, otherwise I’d have gone online when I got home from work instead. So I kept browsing, and found every single book they had under the topic of web design was only available either through an online purchase or as an eBook.

E-Commerce is winning

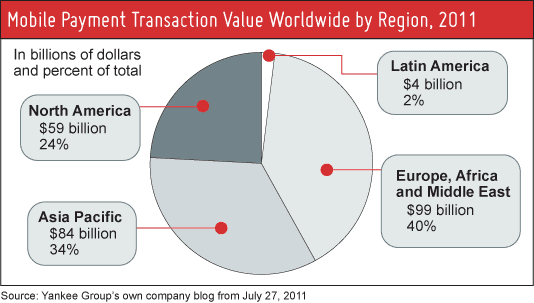

In terms of printed media E-Commerce is absolutely dominating. Essany cites a statistic to back up this outlook, writing that according to the Yankee Group (a research company we’ve cited ourselves when they made projections on The Future of Mobile Payments), consumers will purchase approximately 381 million eBooks next year with an average selling price of $7.

Most impressive

My own research for this very blog during last year’s holiday shopping season demonstrated what to me has become a very obvious aspect of the economy: shopping online is a common thing for people to do. That means E-Commerce is making buckets of money. Each one of those transactions are part of the payment processing industry. The foundation is there. People have found the convenience of shopping online so powerful that it outweighs the risk of fraud. So more and more people have taken to solving their shopping problems online. I know that I myself do this. It’s so much easier to look for a product online and know you’re getting what you want with a few clicks, than it is to go trudging out to a store that may or may not have the item you want.

Last year in a Blog Post about the upcoming holiday shopping season, I reported “A 2010 survey conducted by Google and OTX found that 35% of internet users start their holiday shopping prior to the end of summer, months ahead of Black Friday. This trend is only continuing to grow as consumers find online shopping convenient to their shopping habits, easy to do, and the wide selection lets them find great deals on price.”

This trend in shopper behavior combines with the rise of virtual media like eBooks like Voltron to form a very powerful lion-fisted, right-left combo to the solar plexus of Print Media’s crumbling empire.

And you know what? I’m OK with this.

I’m a voracious reader. But I’m also under the thrall of the convenience of online shopping. I truly do turn to the internet first for most products I’m interested in. This is heightened when I want to purchase a book, a magazine or a comic book. It’s just so much easier. The only time I’ve wanted to wander into a book store to buy a book was when I wanted it right then, with no wait on delivery. And I found the remnants of the only big chain bookstore in my local area to have already forced the decision upon me: If I wanted a book about web design, I needed to go directly to the web to get it.

I’ve been using the ComiXology app this year. And when the company that I once worked for (Valiant Comics) as a production intern returned to the comic book industry after a long hiatus, publishing a comic book I once did post production work for (X-O Manowar), I immediately jumped onto my phone to purchase it. I find that I read more web comic strips than I ever read in a newspaper. I find I go to the web for my news. Or my phone. I’ve even found myself reading straight up only published electronically eBooks this year. I still prefer printed books, but for me they’ll be online purchases. I’ll buy the collected editions of comics I like, but do so online. I’ll buy printed books of titles I really just want to curl up with and turn the pages of, but I’ll make the purchase online. It’s gotten so pervasive in my life that I now buy tickets to sporting events online, brands of tea I can’t find at my local supermarket online, all of my roller derby referee equipment and rules books online. I even bought my ticket to The Avengers on my phone through Fandango and had it delivered to my phone as a mobile ticket.

E-Commerce is where it’s at. And publishers of the written word need to embrace this shift. Maybe it’s easier for me to do so because I work in the payment processing industry and get to see firsthand how big and booming E-Commerce is.

The Official Merchant Services Blog returns to a topic that it covered thoroughly throughout 2011: The Durbin Amendment. With the Stop Online Piracy Act getting most of the headlines lately, Durbin Amendment’s continued impact on the payment processing industry has gone into stealth mode. Until today that is. Stick with us as we offer a whirlwind roundup of all things Durbin related.

Bank of America Took a Beating

We’ll start off our tour Durbin tidbits with this article by ABC News. Apparently Bank of America took a substantial hit from their plan to charge $5 per month to use debit cards. According to the article: “Bank of America’s failed plan to impose a $5 monthly debit card fee led to a 20 percent increase in closed accounts in the last three months of 2011 and a public relations headache.”

The article quotes Bank of America CEO Brian Moynihan as saying, “yes, we had some impact from the $5 debit fee. That’s why we made a decision to reverse it.”

It wasn’t all bad news for Bank of America though, as the bank reported earnings of $2 billion in the last three months of 2011, up from a net loss of $1.2 billion in the same period a year ago, boosted in part from a one-time gain on the sale of China Construction Bank.

Small Lenders Strike it Big

The next little bit of Durbin aftermath comes from this article by NACS online. As was seen in the Host Merchant Services in-depth analysis of the legislation, The Durbin Amendment only applies to lending institutions with assets over $10 billion. Smaller banks and credit unions are exempt from the Durbin Amendment. As a result of being exempt, a Wall Street Journal report cited by the NACS article states that these institutions have been “collecting fees that are often three times those imposed on cards by large banks.”

For comparison, the article says: “The WSJ notes that a $100 sweater purchased with a debit card would incur a fee of 95 cents on a card issued by a smaller bank and only 26 cents for those issued by big banks. “

The article also suggests that banks face further uncertainty by April 1, 2012, when “all U.S. banks and credit unions must offer retailers more choices of companies used to process debit card transactions, a move that is expected to lower interchange fees further.”

New Target: Credit Card Swipe Fees

Time Magazine Online Feature Moneyland reports something that Host Merchant Services has already touched on before in The Official Merchant Services Blog — that Credit Card Swipe Fees may be the next target of legislators and financial reform. From the Time article: “There’s another interchange fee fight in the offing — this time over credit cards. According to CNBC, equity analysts who cover the financial sector have expressed worry that ongoing litigation involving several major banks could lead to a cap of 0.5% on credit interchange fees — one-fourth of what’s currently charged — potentially dragging down bank earnings. If that happens, consumers who are used to generous credit card rewards programs complete with double miles, accelerated earnings, and big sign-up bonuses might get a rude awakening.”

The Official Merchant Services Blog on December 13, 2011 covered the topic of a Credit Card Swipe Fee. In that blog we wrote: “the plan would end up working much like the Durbin Amendment has worked. Where the idea of reform would get overshadowed by how banks and credit card companies reacted to the law. There would be some shifting, so in that sense the reform would cause change. But that eventually the burden for paying for any losses that banks and credit card companies get forced into through reform would end up squarely on the shoulders of the consumers.”

The Time article notes something that Host Merchant Services already pointed out regarding a Credit Card version of the Durbin Amendment — Banks would take another huge hit because Durbin has language that freed up banks and merchants to market and promote options to the consumer directly. In short, Durbin’s language freed merchants up to promote credit over debit. And because of that, a lot of merchants did just that as Banks offered new programs to make credit the more attractive choice. Subsequent changes that would now penalize Banks for doing that would create a lot of negative momentum for Banks and added onus for consumers who get stuck with no good choices overall.

New Hampshire Law

This article from credit.com reveals that one state legislature is already making moves to see a Credit Card Swipe Fee Cap become reality. As the article states: “A piece of legislation introduced in the New Hampshire House of Representatives, House Bill 1319, has drawn some attention for the way in which it would drastically alter the credit card landscape between businesses and payment processors. The law will limit the amount banks chartered within the state are able to charge businesses for processing credit card transactions to just 1 percent of the total purchase value.”

The article goes on to state that many businesses pay costs that range from 0.67 percent of the transaction’s value to 4.76 percent and that a MasterCard spokesperson told the Nashua Telegraph that the average 1.75 percent.

Cash Still Rules Everything Around Me

Our last news brief on the topic of the Durbin Amendment and swipe fee caps is a little different. This article from the Huffington Post shows a study that reveals cash is still king. The gist of the article: “More than three-quarters, or 79 percent, of consumers said they made a cash purchase in the last seven days, according to a report released on Tuesday from Javelin Strategy & Research, a market research group for financial services. Compare that to about 65 percent of credit and debit cardholders who say they swiped their plastic in the last week.”

The article suggests that this is a consumer reaction to card swipe fees. The article states that consumers are choosing to pay for items with cash to avoid fees on small, everyday purchases. The convenience of plastic gets overrun by the savings consumers perceive they get from going back to cold, hard cash. The study indicates that cash is replacing debit for small purchases, and credit is replacing debit for big purchases and the Durbin Amendment’s lasting legacy may simply be that it pushes Debit out of the consumer’s arsenal of payment options.

Today The Official Merchant Services Blog is playing a bit of catch up. The story we’re going to highlight and discuss is almost three weeks old. It was intended to run earlier, but technical difficulties with the blog’s production kept it from appearing until now. However, we feel the story is still worth some attention due to the issue it highlights about the payment processing industry.

The story comes to us from a Chicago, IL section of the Better Business Bureau (BBB). This article from the BBB says that the organization has seen a 42% rise in complaints against credit card processing services. The article, which originally was posted by the BBB on December 15 found that complaints were up for the 12 month period in 2011 compared to the previous 12 months. The breakdown was specifically 110 complaints in the recent 12 month period versus 77 complaints in the period prior.

Not Just In Chicago

The complaints aren’t just lodged in Chicago. This article from Fox40.com details similar complaints in Sacramento, CA. The article states: “The Better Business Bureau is warning businesses to beware of sales pitches by credit card processors that don’t reveal key details that could end up costing business owners more than they bargained for.”

And it quotes Caitlin Peterson of the Better Business Bureau of Northern California as saying “We’ve had over 1,700 complaints this year against the merchant processing business.”

What the Problem Is ?

From reading through the two articles — as well as an older BBB article about issues in the St. Louis, MO area — the problems that merchants are encountering are really straightforward. Business owners are being approached by salespeople offering big savings on their payment processing. And then once the merchant signs a contract with that person, they are saddled with hidden fees for services they were not told about. In short, the business owner is led to believe they are getting a great deal but end up having to pay out more because of all the things not mentioned in the deal. So complaints against payment processors rise in select areas.

Pricing and Transparency

This type of behavior is the exact reason Host Merchant Services utilizes its philosophy of Interchange Plus pricing and no hidden fees. These types of issues are why CEO Lou Honick says “Host Merchant Services is about bringing trust to the payment industry.”

“Payment processing is confusing,” says Honick, noting the ease in which merchants can get saddled with the types of issues that have cropped up with the BBB complaints. “The big guys make it difficult to understand exactly what your rate is and what fees are associated with accepting credit cards. We deliver personal service and clarity. Our people care about customer service and will take the time to explain how everything works.”

Honick also cites the process that Host Merchant Services uses to directly counter the problems that business owners encounter with other processors: “We believe that when you get your statement every month, you should understand every item, and it should match what you were promised in the sales process. If you have a question, there is a live person at Host Merchant Services ready to assist you.”

The Details

One of the primary ways Host Merchant Services combats the practices that lead to these complaints is with their pricing structure. Host Merchant Services uses Interchange Plus pricing instead of the more standard tiered pricing format. Interchange Plus makes statements easier to read, customer service easier to provide to merchants, and savings much easier to guarantee. Here’s a small graphic explaining the basics of how Interchange Plus works:

You can review a comparison between Host Merchant Services Interchange Plus pricing — which is simple and transparent — and the tiered pricing plans that other processors use in a two-part blog series that The Official Merchant Services Blog ran in October, 2023.

Part One

Part Two

Follow Up

What the BBB Advises ?

The BBB advises merchants take these steps to avoid getting stuck with the issues that their complainants have encountered:

Ask around.

The BBB suggests getting at least three estimates from different Payment Network Providers and to checkout he BBB Business Review of the merchant processing service. They also suggest asking fellow business leaders for referrals.

Know where to turn.

The BBB advises you check up on the support team that a potential Merchant Services Provider offers you. Can you contact them 24 hours a day? What is their response like outside of typical business hours? And the BBB advises you make sure their technical support can handle your needs as that kind of support is vital to your business’ success.

Try them out.

The BBB says that you should not settle without a trial period. You should make sure that the payment processor you choose has a 100 percent money-back guarantee before selecting them. Make sure their service works for you, and make sure they keep their promises to you.

Don’t get locked in to a long term contract.

The BBB is very clear on this. Never commit to a long term agreement that locks you in. Make the merchant services provider earn your business each and every month.

Get references.

The BBB advises that you get the payment processor to provide you with references. And then suggests you spend some time checking up on those references.

Make sure you know what you’re being charged for.

The BBB says that if you have a question regarding a fee that you were charged, ask the merchant services provider. Don’t let them hide fees on you. Make sure you understand your statement.

How Host Merchant Services Stacks Up

Host Merchant Services falls in line with what the BBB advises merchants to do. The company places a big emphasis on transparency. Their salespeople will explain a merchant’s statement in detail. One of strengths of the offering from Host Merchant Service is their guarantee to save a merchant money. They achieve this by a statement analysis. Not only will Host Merchant Services explain the details of what your statement and fees are, completely transparent, while you process with them, they’ll also explain where the hidden fees are with your current statement.

Host Merchant Services will provide references. They do not lock you in to a contract. They do not charge you a termination fee. They provide free equipment and free paper for your terminals. And they offer 24-7-365 customer service where they guarantee you will talk to a real person that will help you out with your issues. You can even initiate a live chat with HMS Support right from any page on their web site.

As Host Merchant Services COO Dan Honick says, “You stay with us because you’re happy.”

The Official Merchant Services Blog is here to share information with merchants to get them better prepared to understand how the payment processing industry works. This premise stems from Host Merchant Services and its philosophy to bring trust to the industry.

Payment processing can be confusing. And nowhere is that more evident than in a merchant’s processing statement. One of the ways some processors make their money is by hiding fees within the arcane labyrinth of a monthly statement, making the fees and the numbers difficult to understand.

Host Merchant Services believes that when one of its merchants receives their statement every month, that merchant should understand the items on the statement and that the fees should match what was promised in the sales process.

So in an attempt to help everyone understand that process better, The Official Merchant Services Blog is going to shine a spotlight on statements and see what there is to see.

What Is a Merchant Statement?

Every month, you receive a Merchant Statement from the company that processes your transactions. These transactions include Debit and Credit Card Transactions. This statement summarizes your net sales for all the cards that you process. It also provides your monthly transaction volume as well as provides you with an itemized list of your daily transactions. You can also see the majority of your debit and credit card processing fees. This is where we’re going to shine the spotlight, as this is where fees get hidden. Your fees on your statement include:

your transaction fee

your monthly discount rate for your Credit Cards

your monthly terminal fee (if you do not own your credit/debit card machine).

your Interchange charges

any chargebacks

third-party transactions

credit adjustments

The tricky part about these fees is that each company assembles their statement in a different way. Each payment processing provider has a unique statement layout structure, so most of the characteristics of the statement are the same but are put there in a different order. It forces merchants –– especially those who have used more than one processor in their time in business –– to do all of the eagle-eyed investigating themselves.

We’ll stick to the basics and then when that’s done, we’ll take a moment to explain why Host Merchant Services might be a little less confusing than other Payment Network Providers.

Card Deposit Summary

It’s pretty common for the Card Deposit Summary to be prominently displayed in a merchant statement. A lot of times it’s the first item a merchant will see on their statement. The phrasing may be a tad different –– perhaps it’s called a fund summary –– but for the most part it’s the opening line on each merchant services provider’s statement. The summary tends to include a laundry list of statement data, such as:

Amount of transactions incurred in that month

The dollar amount of those transactions

What credit cards were used

Any discount or coupon usage charges

Often this information is presented as individual daily line items, but some payment processors may combine all the data into one section.

Credit Card Fee Summaries

After the deposit summary information, most statements provide some sort of variation of how much the credit card issuer charged per transaction. This is usually called the Summary of Card Fees. As we explained in a previous blog series, a lot of payment processors offer a tiered pricing plan. And this is the section of the statement where you will see fees being charged for “qualified transactions.” That term specifically relates to your qualified tier in the pricing plan you signed up for. This section should include any fees, discounts and rates applied to transactions made through your merchant count. Most payment processors provide a complete list of card fee categories in this section, since qualified and non-qualified pricing tiers differ. Also included should be a listing for gross sales amounts per credit card and any fees and discounts applied to specific card transactions.

Transaction Fees

This section is an extension of the Summary of Card Fees section. This section lists each fee related to card transactions in dollar amounts. This can be a daunting section to sift through as the terminology used in this section is extensive. There is no shortage of card fee categories, and you’ll see chargebacks and batch header fees and ACH return fees mentioned here. This is why Host Merchant Services says payment processing can be confusing. The statements sometimes overwhelm merchants with tiny fees and cryptic buzzwords. Within that morass, the black hat companies will hide fees that some merchants aren’t aware they are paying or –– even worse –– aren’t aware they don’t even need to pay.

No Hidden Fees Guarantee

Now that some light has been shed upon the statement, and we can see where the fees get hidden and where the confusion takes place, it’s time to take a look at a much simpler way of doing this: Host Merchant Services offers a processing plan with no hidden fees. The company offers its merchants an Interchange Plus pricing plan. So right off the bat, there are no tiered pricing plan issues, so its merchants are not hit with “non-qualified” tier penalties and fees. Host Merchant Services also eschews a long-term contract. So there is no application or set up fee. No annual fee. No Non AVS Adjustment fee. Host Merchant Services does not penalize you with termination fees. Host Merchant Services also does not lock its merchants into contracts for equipment. The company provides free equipment, including free terminal paper. The prices that the company quotes during the application process are grandfathered, and will not increase at all during the lifetime of the business relationship.

It’s a simple and straightforward plan, really. Host Merchant Services shows you exactly what you will be charged on your monthly statement. The company has swept away many of the added charges that other companies hide on statement fees. And then the company sticks to the plan they quoted its merchant. The company will be happy to review your statement and help you find areas where you can save money each month.

So monthly statements may be extremely confusing –– to the point where one thinks it is being done on purpose. But using some of the guidelines put forth here, or using Host Merchant Services itself, you can find your way through the puzzle that is payment processing.

The Official Merchant Services Blog continues its series on Payment Gateways. Yesterday’s blog dealt with the basic question of why your business would want a Payment Gateway in the first place. It also looked at the basic setup and costs of a Payment Gateway and some of the differences in the Payment Gateway options that Host Merchant Services offers.

Today’s blog is going to examine how Payment Gateways work.

How Do They Work?

A Payment Gateway is literally a link between a merchant, the client, the client’s credit card provider and the merchant’s bank. The main job of the gateway is to validate your customer’s credit card securely, make sure the funds are available and get you paid. The system is based on the transaction process you see in your standard retail store, where a credit card is swiped. But it does not require a card to be present to be charged.

Some gateways also require a merchant account –– a specific type of bank account that handles your funds received via credit cards. Host Merchant Services provides its merchants with Payment Gateway options as part of the services that come with opening a merchant account through the company.

Host Merchant Services has created an easy to read, step by step graphic on Payment Gateways. You can view that graphic here.

But to briefly walk you through the process:

1.A customer places an order on a merchant’s website and submits the order through the site.

The website then encrypts the payment information that is to be sent between the browser and the merchant’s webserver. This is done vial Secure Socket Layer (SSL) Encryption.

The merchant then forwards the encrypted transaction details to their payment gateway.

The Payment Gateway forwards the secure transaction information to the payment processor (in this instance, Host Merchant Services).

The processor forwards the information to the card association (be it Visa or MasterCard or Discover).

The credit card issuing bank receives the authorization request and sends a response back to the processor with a response code.

This response gets forwarded to the Payment Gateway.

The Payment Gateway sends the response back to the website where it is interpreted and relayed back to the cardholder and the merchant. This entire process of forwarding the information for a response, and getting the response back takes 2 to 3 seconds typically. Not only will the response of approved or declined be generated but the process also defines why a transaction might fail, and lists the reason.

For an approved transaction, the Merchant then submits all of their approved transactions in a “batch” to the acquiring bank for settlement at the end of its business day. The acquiring bank deposits the total of the approved funds into the merchant’s account. Settlement of “batches” typically takes 2 days with Host Merchant Services.

How Do The Transactions Stay Secure?

The security of these transactions are important. Security is the key reason Payment Gateways exist, as the entire point of the system is to get sensitive payment information transmitted from a customer’s web browser back and forth to a bank for approval of the purchase. Here are some of the technical details that happen with Payment Gateways to ensure the process remains secure:

Since the customer is usually required to enter personal details in the transaction process, the payment gateway is often carried out through HTTPS protocol.

To validate the request of the payment page result, signed request is often used – which is the result of the hash function in which the parameters of an application confirmed by a «secret word», known only to the merchant and payment gateway.

To validate the request of the payment page result, sometimes IP of the requesting server has to be verified.

There is a growing support by acquirers, issuers and subsequently by payment gateways for Virtual Payer Authentication (VPA), implemented as 3-D Secure protocol – branded as Verified by VISA, MasterCard SecureCode and J/Secure by JCB, which adds additional layer of security for online payments. 3-D Secure promises to alleviate some of the problems facing online merchants, like the inherent distance between the seller and the buyer, and the inability of the first to easily confirm the identity of the second.

Up Next

In tomorrow’s entry in this series we will take a look at the costs of a Payment Gateway, specifically the options Host Merchant Services offers and then analyze some of the criteria a merchant needs to consider when choosing a Payment Gateway.

{kind=link}