This week, the Official Merchant Services Blog will delve into a three-part comparison of the services offered by Host Merchant Services and Square. We will begin by giving a basic overview of both and then compare how the two companies set up a merchant account. We will then move on to a comprehensive look at the pricing and security aspects, over the next few days.

Mobile Payment Processor Square has been pushing its brand heavily this past year. The startup lets merchants process credit and debit card transactions through their mobile devices, including iPhones, Android smart phones, and even the iPad. The company picked up a lot of attention in August 2012, when it announced a partnership with Starbucks to provide mobile payment ability to 7,000 locations nationwide.

Host Merchant Services has been reporting on the Mobile Payments market for the entire time Square has been making its splash in the industry. HMS has also been marketing its own mobile payment processing solutions — giving its customers the option of accepting credit and debit card payments through iPhone, iPad and Android as well.

So how does the suite of Host Merchant Services Mobile Payment solutions stack up against Square? Today we find out in Part 1 or our three part series, Host Merchant Services vs. Square: The Merchant Account.

The Merchant Account

The first major difference between the two mobile payment processing providers is the most basic: The Merchant Account.

Square does not actually provide a merchant account to its customers. Square provides its customers with processing services, but not a traditional merchant account. Instead, Square acts more like a payment aggregator.

Typically, Merchant Aggregators or Payment Aggregators are service providers through which e-commerce merchants can process their payment transactions. Aggregators allow merchants to accept credit card and bank transfers without having to setup a merchant account with a bank or card association. The Aggregator provides the means for facilitating payment from the consumer via credit cards, stored value accounts or bank transfer to the merchant. The merchant is then paid by the Aggregator.

This is a pretty basic description for how PayPal began — and is also a really solid description for how Square works with its customer base.

Aggregation enables businesses that may be too small or risky to obtain a traditional merchant account to accept credit and debit card transactions anyway. The practice gets controversial among the more traditional sectors of the payment processing industry because it makes it harder for networks to monitor just who generates transactions and, most importantly, the attendant risk.

Some of the drawbacks of Square’s aggregation, such as caps on transaction size and delayed fund dispersal, will be reviewed in Part 2 of our series. Host Merchant Services’ traditional merchant accounts do not place caps on transactions or delay funds for any merchant.

Host Merchant Services offers a traditional merchant account to its customers. This is a noteworthy difference in practice for the merchant. The account is in the merchant’s name, giving the merchant more rights as well as more responsibilities. The traditional merchant account also holds Host Merchant Services to the merchant with added oversight on the transaction process. This is bolstered by Host Merchant Services’ customer service goals, creating a relationship where Host Merchant Services goes all-out for each merchant. The approval process through Host Merchant Services is more extensive up front, however the security and service provided gives merchants more peace of mind and more value for their effort.

In conclusion, Square and Host Merchant Services offer two very different types of merchant accounts. Although both companies allow merchants to accept credit cards, Square does not offer a true merchant account. Host Merchant Services creates a traditional merchant account, and the customer has actual control over aspects of the account. HMS directly links the merchant and their account, without any type of aggregation. This practice allows easier tracking of authorizations and transactions, a streamlined chargeback process, and less risk over all.

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. We want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: we deliver personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is Payment Aggregation.

Typically, Merchant Aggregators or Payment Aggregators are service providers through which e-commerce or mobile payments merchants can process their payment transactions. Aggregators allow merchants to accept credit card and bank transfers without having to setup a merchant account with a bank or card association. The Aggregator provides the means for facilitating payment from the consumer via credit cards, stored value accounts or bank transfer to the merchant. The merchant is then paid by the Aggregator. This practice gets controversial among the more traditional sectors of the payment processing industry because it makes it harder for networks to monitor just who generates transactions and, most importantly, the attendant risk.

With a traditional merchant account, like the ones Host Merchant Services offers, there is a noteworthy difference in practice for the merchant. The account is in the merchant’s name, giving the merchant more rights as well as more responsibilities. The traditional merchant account also holds Host Merchant Services to the merchant with added oversight on the transaction process. The security and service gives merchants more peace of mind and more value for their effort. Payment Aggregators also have discretion over when a merchant receives their funds, another drawback of the aggregation model.

Online payment processor Stripe announced on Friday, that the company is committing to transparency and user rights for its customers, following the lead of Google, Twitter, and Host Merchant Services. For today’s edition of the Official Merchant Services Blog, we will introduce Stripe, as well as discuss what these recent steps mean for the company, and the industry.

Stripe’s recent move is part of an effort to increase awareness of the effects of the legal process on their users. The company is an online payment processor geared toward developers. They offer to handle everything, including storing cards, subscriptions, and direct payouts to your bank account. Although some merchants may find that helpful, it may make refunds, voids, retrievals and chargebacks more difficult, since you do not have direct access to your customers’ payment information. The company also charges unusually high fees for acceptance, in an effort to simplify the process with rates starting at 2.9% and 30 cents for any card type.

Stripe charges such a high rate, in an effort to simplify things for merchants. I would like to point out, however that a standard Debit card, using Durbin Debit rates would qualify for a rate of 0.05% and 22 cents under Interchange Plus pricing, the type of pricing offered here at Host Merchant Services. Since this rate of 5 basis points is so much lower, Stripe’s customers are overpaying by as much as 2.85%. For a transaction of $500, Stripe would charge a merchant $14.5 (2.9%) and an additional 30 cents on a transaction that actually costs them 25 cents (0.05%) and an additional 22 cents, or $0.47 total. In this case, the flat rate of 2.9% charged, is much greater than the Durbin Debit rate that could be applied, if the merchant was using Interchange Plus.

Stripe is moving towards more transparency, because they sometimes receive legal requests from third parties to stop doing business with certain users. Stripe is enlisting help from Chilling Effects, a joint project run by the Electronic Frontier Foundation, Harvard, Stanford, Berkeley, and other law schools that publish copyright takedown notices sent to web companies, and its most prominent contributors are Google, Twitter and GitHub.

It’s not clear how often the payment processor is asked to stop working with a site or on what grounds, however the best example of the lack of transparency by the net’s dominant payment intermediaries was demonstrated in the fall of 2010. Visa, MasterCard and PayPal all cut off WikiLeaks on the grounds it was engaged in illegal activities, after publishing a trove of U.S. diplomatic cables.

Stripe intends to provide transparency reports regularly about how many requests it gets, a practice that was pioneered by Google. Stripe, in regards to a subpoena notification policy also says it’s instituting the same policy as Twitter, committing to informing a user, when not barred from doing so, that someone is subpoenaing their record. This allows the targeted user to try to quash the subpoena in court. Twitter has spent significant resources fighting to allow its users to resist government subpoenas — including winning the right for WikiLeaks associates to try to quash a grand jury subpoena for their Twitter records.

In conclusion, it is a step in the right direction for large Internet companies to be on the side of transparency as well as advocate for the rights of their users. I hope more web companies step forward in the name of full disclosure in the future. Host Merchant Services has been committed to transparency from the start, and we maintain the promise of personal service and clarity for all customers.

Today we enter the realm of mobile payments again for this edition of the Official Merchant Services Blog, as we look at the newest company to enter the already crowded playing field. Daily-deal giant Groupon, Inc. announced the creation of Groupon Payments in late September, a service that will allow merchants to accept credit and debit cards using Apple Inc.’s iPhone or iPod touch.

Groupon is attempting to leverage its existing loyalty services for merchants, and claims to have low card-acceptance prices. The service provides a free card swiper made by Roam Data that plugs into the Apple devices’ audio jacks, or a $100 wrap-around case from Infinite Peripherals for merchants that expect heavier usage.

Merchants who want use Groupon Payments will be charged fees of 2.2% for Visa, MasterCard and Discover transactions plus 15 cents, and 3% and 15 cents for American Express. If a merchant has ever offered a Groupon deal before or has committed to doing one in the future they are eligible for a discount rate for swiped transactions of 1.8% plus 15 cents for Visa-MasterCard-Discover transactions, and 3.0% plus 15 cents for AmEx sales. Groupon also will charge more for keyed, or card-not-present transactions, with rates starting at 2.3% and 15 cents for Visa-MasterCard-Discover and 3.5% and 15 cents for AmEx.

Groupon is one of the leaders among the national daily-deal offering websites. Senior analyst Rick Oglesby of Boston-based Aite Group LLC said of the program, “Overall, I think it all makes sense. Groupon brings on a tremendous amount of value to merchants due to the volume of eyeballs they attract.”

The numbers appear to back that claim up, the company offers a host of other services that reinforce customer loyalty to merchants, including featured daily deals, deals from national merchants, and Groupon Now! a system for instant offerings available online and through mobile devices. With 250,000 merchant relationships worldwide, the company refused to disclose it’s U.S. merchant count. In terms of customer base, a Groupon investment filing shows they had 36.9 million active consumer customers in the first quarter alone.

Groupon’s program is not without downfalls however; one seems to be the risk of slowing the growth of merchants willing to offer heavily discounted deals. The service is currently available only for Apple devices, and the company hasn’t specified if it will cater to Android phones in the future. Also, it is worth noting that the company does not mention a length of contract or if other fees are involved, including possible termination fees for the service, usually a troublesome sign.

The part of this that I find the most interesting, is that Groupon decided to shun the existing mobile payments companies and create another. Many retailers have made strategic decisions to partner up with mobile payments processors as they see the emerging mobile payments sector as lucrative. Groupon Payments may develop into serious competition for Square Inc., Intuit Inc.’s GoPayment Service, and PayPal.

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is Discount Rate.

Discount Rate

The simple definition of the term Discount Rate as it applies to merchant accounts — it is a combination of the fees charged by the card acquirer to the merchant for processing payment card transactions. So what that’s really saying is the Discount Rate is what the payment processor charges the merchant so that they can make profit off of the transaction — it’s not really a discount in any sense of the word when defined like that.

So let’s break this down a little more to understand this buzzword beyond just the obvious. A Merchant Account has a variety of fees. Some of these fees are charged periodically, such as a monthly service fee. Others can be charged on a per-item or percentage basis, such as a Chargeback Fee. Some fees are set by the merchant account provider.

The majority of the per-item and percentage fees, however, are passed through the merchant account provider to the credit card issuing bank according to a schedule of rates called interchange fees, which are set by Visa, Discover, and Mastercard.

Each merchant services provider has real costs in addition to the wholesale interchange fees, and creates profit by adding a mark-up to all the fees they have to take on to provide their services in the first place. The discount rate comprises the combination of dues, fees, assessments, network charges and that additional mark-up merchants are required to pay for accepting credit and debit cards. The largest of these fees by far is the Interchange fee.

There are a number of pricing models that merchant services providers utilize, but Host Merchant Services uses the Interchange Plus pricing plan.

Interchange Plus pricing means that the acquirer charges you a variable MSC consisting of the cost price plus a fixed markup. Interchange Plus Pricing is exclusively how we quote at Host Merchant Services. Interchange Plus, also known as Cost Plus, pricing gives the customer a fixed rate over published Interchange Fees. This pricing format is normally quoted as a discount rate (percentage fee) along with a per item or authorization fee. The great thing about Interchange Plus pricing is that you always know exactly what you are paying to your processor to services your account. Think of Interchange, and all the associated fees, as an unavoidable cost. No matter who you process with, you have to pay these fees. They may be labeled differently, or wrapped up in a confusing pricing tier, but one way or the other, you are paying Interchange fees. By understanding the markup you pay over Interchange, you know exactly what you pay to your processor and exactly what is going to the card associations. That allows you to make a decision on whether or not the markup seems reasonable for the service you get and choose your processing partner accordingly.

Here’s a small graphic explaining the basics of how Interchange Plus works.

The Mobile Payments Technology sector has been the topic of overt optimism for quite some time now. We’ve reported multiple times that industry analysts have predicted large gains in Mobile Payments profits over the short- and long-term future. Our article from 2011 showcased three different research groups and their take on the successful future they felt was in store for Mobile Payments.

More pieces of that predictive puzzle have been falling into place. According to a mobile payments survey conducted by IDC Financial Insights, mobile payments use in the United States has doubled. The May 2012 study looked closely at emerging pay method technologies and discovered that 33 percent of respondents had used their devices for mobile payments at least once.

IDC’s practice director, Aaron McPherson, told QRCode Press that “Based on our results, we expect to see continued growth in open-loop prepaid cards and mobile payments next year, and believe that the improvements being offered in electronic-bill delivery will break electronic-bill presentment and payment out of its doldrums as well.”

The Next Big Affirmation for Mobile Payments

Visa is convinced new payment tech, including mobile payments, are definitely the trend of the future — so much so that the card association giant is poised to showcase the power of the future in the spotlight of the 2012 Olympic Games in London. One of the new technologies Visa is thrusting into the public eye at the Olympics is EMV Chip Cards — something we highlighted back in February. Visa is heavily invested in Smart Card technology so it’s no surprise the company is using its Olympic Games partnership to point some attention at its EMV efforts. But right alongside that EMV push, Visa is also Mobile Payment Technology as a safe and convenient payment option for consumers throughout the London games.

Jim McCarthy, Head of Products at Visa Inc., said “This summer we will be demonstrating the future of payments in London – a future where most consumers will rely on mobile devices, tablets and PCs to manage their daily financial lives.” Visa’s Olympics marketing push for the future of Mobile includes:

Visa Mobile Payments and Services: A limited edition of the Samsung GALAXY S III, Samsung’s Olympic Games Phone during the London 2012 Games, will be provided to Visa sponsored athletes and trialists. The device will feature an Olympic-branded version of Visa’s mobile payment application, Visa payWave. To make purchases, consumers simply select the Visa icon on the Samsung device and hold the phone to a contactless payment terminal to pay.

Visa Mobile Prepaid: During the London 2012 Games,Visa Inc. will also showcase its newest product – Visa Mobile Prepaid – the first mobile-based Visa product providing consumers in developing countries a payment account that offers Visa’s high standards of security, reliability and global interoperability. By accessing their Visa Mobile Prepaid account on their mobile phone, consumers can send and receive international remittances, pay bills, top-up wireless minutes, and access Visa ATMs.

Setting New Standards

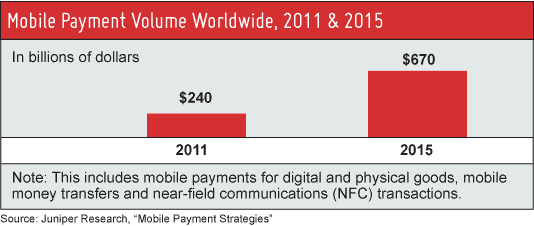

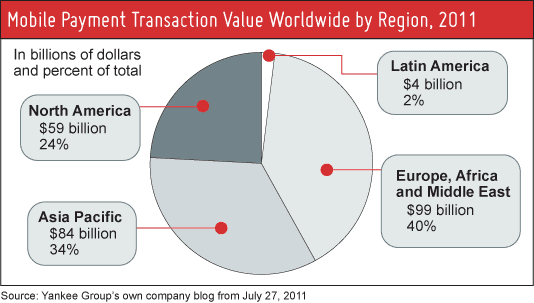

Looking at last year and then at this year’s statistics, Mobile Payments are doing their best to meet the bold predictions analysts have lined up for the future. The sector is growing rapidly and consumers in both the U.S. and around the world are embracing the convenience that the technology brings to their shopping habits. Juniper Research, a company that specializes in the identification and appraisal of high growth opportunities in various mobile telecommunications and applications sectors, put out a publication on July 5, 2011, titled “Mobile Payment Strategies.” Juniper predicted worldwide mobile spending would jump from $240 billion in 2011 to $670 billion in 2015.

Well Juniper is back with a new forecastthat focuses on Near Field Communication (NFC) and this study predicts that in just five years the NFC Mobile Payments market will will exponentially increase and eventually exceed $180 billion — a whopping seven times what it is today. The study forecasts that one in four people from Western Europe and the United States will use NFC as a payment mechanism by 2017.

Juniper cites last year as a turning point for NFC payments and suggests that major consolidation of the technology is the impetus for the predicted growth in the market as consistent standards and protocols will help fuel rapid growth and assuage the security concerns of consumers. Juniper says that in 2011 major technology infrastructure standards were finalized within the NFC Mobile Payments market so that many mobile network operators committed to the market and NFC payment pilots from both mobile operators and financial institutions transitioned to commercial service. And the research firm pointed to NFC-enabled smartphone models being announced by almost all handset manufacturers and Google as a key factor for igniting interest in the mobile payment usage in the U.S.

“This is a critical time for the NFC retail payments market,” said report co-author Dr. Windsor Holden. “Despite the significant progress being made today, the full potential of the market can only be fulfilled if all ecosystem players are equally committed and mobile wallet consortia remain in place.”

Payment processing can be confusing even for the experts in the industry. The system seems to be purposely designed to be difficult to understand even the most basic things, like what exactly your rate is and what fees are associated with accepting credit cards.

But accepting credit cards has become a necessity for businesses today. People are shifting toward a paperless society quickly, and online shopping has become a staple to even the most resistant consumer. As a business owner you need to become an expert on payment processing and do so quickly if you wish to keep ahead of the curve and not get burned by hidden fees and surcharges that cut directly into your profits.

Which credit card processing company should you get your merchant account from? Credit card processing fees, transaction fees, statements fees, PCI DSS fees, annual fees, all pile up. And these fees vary a lot from processor to processor.

Today, The Official Merchant Services Blog is going to give our faithful readers a quick and effective guide on how to compare and evaluate credit card processing companies.

Not All Processors Are Alike

There are many processors that offer merchant accounts and let small, medium and large businesses accept credit cards in brick and mortar locations as well as online through their website. There’s even a huge push today for mobile payments — letting merchants accept payments directly through their mobile phone from just about anywhere. With the wide variety of options, business owners may feel overwhelmed when trying to find the processor that suits them best.

Finding a processor and getting a merchant account isn’t easy.

For starters, the card associations — Visa, MasterCard, Discover and American Express — all have their own rate sheets know as Interchange Reimbursement Fees. These fees make up the majority of what a merchant pays to their processor and they vary greatly depending on the card type accepted. The rates and categories are complex, and confusing to follow for just one of the card companies. All of them together combine to make a maze of fees and categories that most merchants get lost in.

Second, many banks don’t offer merchant accounts directly to small businesses, so those businesses need to go through third party providers for a merchant account. These third party processors have different fee structures among themselves and different rules. So business owners face a lot of confusing variety from both the card association as well as the processor.

To add even more layers to this, businesses that process credit card orders online need to pass their transactions through an online gateway system. Whatever shopping card software is used has to interface with that gateway, so integration from shopping cart to gateway to processor is extremely important.

So let’s dig right in and see what’s what from the processor side of things.

First: Their Rates and Fees

For payment processors, a variety of things about you and your business can influence the discount rate and various fees they charge you for accepting charge cards as payment. Some of those factors include:

The number of years you’ve been in business

The percentage of your sales that are made over the phone or the internet

The type of business you are in

Your personal credit rating

The average dollar amount of each sales transaction

Your monthly sales volume

Keeping all of that in mind, discount rates tend to range from 2.24 to 3 percent for home run and small businesses that accept Mail Order/Telephone Order transactions. These transactions are higher risk and carry higher fees. To find out more, read our knowledge base article on MO/TO.

You’ll find in your search for a processor, however, that many processors advertise discount fees less than 2 percent. These lower fees are for swiped transactions — sales made by running the customer’s credit card through a machine. These card present transactions are more secure and much less risky so fees and penalties tend to be much lower. And online transactions through secure payment gateways also carry less fees and penalties than card-not-present transactions. Keep all that in mind when comparing pricing and rates between offers from payment processors.

Another key to rates and pricing was touched on before by The Official Merchant Services Blog when we compared Tiered Pricing to Cost Plus Pricing. To recap, Cost Plus Pricing tends to end up costing the merchant less because the merchants don’t get dinged for higher surcharges from other rate buckets. So a tiered pricing rate offer will seem lower than it actually ends up being.

Second: Other Fees

The discount rate isn’t the only fee to consider when comparison shopping. Business owners should also consider the application fees, the initial cost of equipment, per-transaction fees (a fee you pay on top of the discount rate for each transaction you process), monthly minimums that affect your fees, voice verification charges, address verification fees (if extra), monthly statement fees and any other added costs a processor will charge you. Something to always keep in mind, processors are very flexible in how they present your proposal and they could offer you a much lower discount rate with a higher per-transaction fee if your average ticket price is low but your transaction volume is high.

Also pay close attention to the cost of equipment and/or software for processing the transactions. Equipment can vary in cost between different processors by hundreds of dollars, even for the exact same piece of equipment. Merchants should try their best to not lease equipment or software. Buy the items outright. By leasing a credit card terminal you lock yourself into a term-contract that may not be something you can cancel without a heavy penalty. And you pay more for the item than its actual cost in the long run.

Third: Read the Fine Print

Be sure to read all application forms and contracts presented to you very carefully. Read all of the small print. Some processors will attempt to charge you if you want to stop processing charges through them in less than two or three years — termination fees. That termination fee can also be completely separate from any penalties you incur when canceling a lease of a terminal. If you plan to do a lot of MO/TO, pay careful attention to what the contract says about the percent of transactions you can process as phone orders (non-swiped). What the salesman says to you during the pitch process may not be what the application actually says because the offer is being given to you at a best case scenario and isn’t taking into account details like added surcharges for card-not-present transactions. At the end of the day, the contract carries the weight over the salesman’s pitch.

Also take into consideration what conditions the company can terminate your account and whether or not there are monthly minimums and maximums. Much of the juggling between different rate buckets in a tiered pricing proposal hinges on being able to surcharge you for details like exceeding a monthly maximum or failing to reach a minimum.

Fourth: The Application Process

Some companies will eagerly attempt to send a representative directly to your place of business — including your home if that’s where you do your business from. Part of this is to pitch the services to you in person. But another part is to be present on site, and to take a photograph of your location. This is part of the application process and is done to verify that you are at the location you say you are. Some other companies can do online site surveys or accept photos and information you yourself provide.

During the process of applying for a merchant account you should be prepared to furnish these items to the company:

A copy of your business license or certificate of doing business

Your driver’s license

Profit and Loss Statements

Copes of previous years’ tax returns

A photo of your office

All processors require two-way access to your bank account once you are accepted. This allows the processor to deposit funds into your account and also allows them to withdraw funds if there are chargebacks.

Comparison: Host Merchant Services

Just for comparison’s sake, here’s quick rundown of Host Merchant Services in the context of the tips we just provided you.

Host Merchant Services offers cost plus pricing. This is transparent pricing where we show and explain all of the fees you are charged. The company also guarantees to offer you the best rate, claiming that if the company can’t save a merchant money they will give them a $100 gift card for their time. And the company guarantees that it will not raise its merchant’s rates. Ever.

The company has no hidden fees. Host Merchant Services also cuts off a lot of the fees that other processors charge — there’s no annual fee, no application fee, no monthly minimums, and the lowest PCI Fee int he industry.

The company provides free equipment — both a credit card terminal and receipt paper.

Host Merchant Services provides customer support for integration of payment gateway services. The company has a variety of gateway options that will integrate with almost all of the shopping carts out there — and will help its merchants get integrated. HMS also offers its own in-house gateway with no transaction fees and full AP for custom integration with any software package.

This is the latest installment in The Official Merchant Services Blog’s Knowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s terms are Revenue Share and Strategic Partnership.

Revenue Share

At its most general definition, Revenue Sharing refers to the sharing of profits among different groups. One form shares between the general partner(s) and limited partners in a limited partnership. Another form shares with a company’s employees, and another between companies in a business alliance.

When applied to the Payment Processing Industry, revenue sharing is a bit more specifically involved in a cost per sale sharing of profits and accounts for about 80% of affiliate compensation programs. E-commerce web site operators using revenue sharing pay affiliates a certain percentage of sales revenues generated by customers whom the affiliate refer via various advertising methods. Another form of online revenue sharing consists in people working together and registering online in a way similar to that of a corporation, and sharing the proceeds.

A third form of revenue sharing on the internet consists of enticing internet users to sign up and create content by offering a share of advertising revenue.

Strategic Partnership

A strategic partnership is a formal alliance between two commercial enterprises, usually formalized by one or more business contracts but falls short of forming a legal partnership or, agency, or corporate affiliate relationship. Typically two companies form a strategic partnership when each possesses one or more business assets that will help the other, but that each respective other does not wish to develop internally.

The Official Merchant Services Blog has some breaking news to report. Host Merchant Services is offering its very first Webinar. On Tuesday June 12, 2012, at 10 a.m., CEO Lou Honick will be giving a 30-minute presentation on the Host Merchant Services Partnership Program as well as a quick introduction on how credit card processing works. After the presentation there will be a 10-minute Q&A period. The webinar is absolutely free to any and all interested in attending.

You can find the

registration form here AT THIS LINK.

What is the Partnership Program?

The Partnership Program that Host Merchant Services has devised is a way for businesses to expand their monthly revenue through referrals. It goes beyond the normal lead-referral system however, and as such gives the partners a larger share of the revenues. With the Host Merchant Services partnership program, HMS helps its potential partners earn monthly revenue through the business transactions of their very own customers. HMS does all the work on its own to set up the partner’s customers for credit card processing. The company provides the partner’s customers with a complete payment processing and financial transaction service quickly and easily. Once the customer has their merchant account set up and has begun processing, the partner then begins to earn a steady and consistent stream of shared revenue with each and every monthly processing statement.

Happy Customers are the Key

Host Merchant Services makes it easy for its partners to find leads and generate revenue. The company does this through the features of its HMS Guarantee. Each lead a partner brings to Host Merchant Services is offered these features:

Great Rate. HMS saves its customers money on their processing. The company pledges that if it can’t save one of its partner’s referrals money on processing, the company will give that referral a $100 Gift Card for their time.

Great Service. Host Merchant Services is about bringing trust to the payment processing industry and the company strives to go the extra mile with its commitment to superior customer service. The company has live people available 24x7x365 to take technical support and customer service calls. As company CEO Lou Honick says, “We pledge that if our customers have a problem, we will fix it.”

No Hidden Fees. Host Merchant Services offers a pricing model that has no annual fee, no application fee, no monthly minimums and the lowest PCI Fee in the industry.

Lifetime Rate. Host Merchant Services offers a straightforward “cost plus” pricing model and the rate is guaranteed. The company grandfathers that rate and will not raise it. The only time the rates change is when the card associations — MasterCard, Visa and Discover — raise the rates for everyone.

No Contracts. Host Merchant Services does not lock its customers into a term contract or charge them early termination fees. As CFO Dan Honick likes to say, “Our customers stay with us because they are happy with our service.”

This combination of features adds plenty of enticement to a partner’s customer base to add Host Merchant Services as its credit card processor. Making Host Merchant Services a reliable company for the partner to refer to its customer base. Host Merchant Services does all of the work to set the referral up with a merchant account, to install a robust payment processing solution, and to keep the customer happy with superior customer service month after month. It’s a safe and easy way for a business to add more revenue to its bottom line each month.

For More Information

You can visit our Partnership FAQ Page HERE AT THIS LINK to get more information. Or contact the company at 1-877-571-4678.

Or you can Register for the Free Webinar and get walked through the entire process, see how the partnership works, and learn about how Host Merchant Services will make you money and keep your customers happy.

Today The Official Merchant Services Blog is going to get a bit personal, for me at least. I’m going to take a moment to talk about print media, and its withering industry. Or, think of it this way: I’ll be talking about the rise to power of E-Commerce — the industry that has helped deliver excruciating body blows to print media over the past decade, knocking it to the mat time and time again.

My history with print media goes back. Way back. All the way back to the beginning of my own career. I’ve worked for four different newspapers, the most high profile being the Asian Edition of the Wall Street Journal at the turn of the millennium. I’ve illustrated various comic strips and published my own comic book. I’ve worked for a printing company in Delaware. Along the way I’ve essentially learned how to make a printed publication from beginning to end; the only skill I lack is the ability to actually push the buttons on a printing press. But every other step, from concept to creation to pre-production to layout and design to editorial to post production I’ve done during my career.

And all of these skills are endangered because of E-Commerce. (Well not really; most the skills translate easily into the virtual media world which is why I’ve been able to transition my career; but everything involving production kind of gets tossed out the window, replaced with skills revolving around web safe colors, pixel sizes and screen ratios).

A really vast, somewhat oversimplified recap of the internet’s impact on newspapers, comic books and book publishing can be summed up by my own career. One of the companies I used to work for, Gannett (publisher of the USA Today), used to have an empire built on small to mid-size suburban community newspapers. They were everywhere. Including Lansdale, PA — where I worked for a time. Gannett was slow to embrace online news though. And the transition from the late 1990s to the aughts left Gannet in a position to streamline and essentially drop a lot of those small and mid-size papers from its stable.

At the same time, I was trying my best to get some traction going in my quest to be a freelance illustrator for comic books. Things didn’t quite work out. I never became the regular artist on The Flash or Spider-man like I dreamed of doing when I was younger. I did however get paid for doing a few projects and got quite a bit of my art published.

Still, steady work was hard to find. And the comic book industry appeared to be dying because of the problems that all of print media now faced.

The major publishers (DC Comics and Marvel Comics) were no longer selling millions of copies of their books. In fact, sales these days are horribly low, with top books barely cracking 100k in sales volume. This reduction in volume can be linked to its distribution channel. Comics stopped appearing in mainstream outlets because the sole distributor of the material, Diamond, only catered to specialized direct market hobby shops (comic book shops). You couldn’t find them at the local supermarket or the local 7-11 anymore. The comic book “rack” was gone. I’d go so far as to make the claim that today, in 2012, the two major comic book companies are really just stables for intellectual properties. Disney and Time Warner wanted Marvel and DC not so much for their ability to publish millions of paper periodicals every month. Instead they wanted the comic book companies for the properties that could at any moment be turned into $100 million blockbuster movie franchises.

So the comic book industry ended up being sold as a niche hobby, and stopped being made as a mass medium periodical. Big companies bought the two biggest publishers of those comics just to keep the ideas and licensing on ice for future movie potential. Print media, it is dying.

And then then there was the issue with comic strips. Newspapers shrunk the comics section over decades. When Action Comics first appeared in newspaper print in thge 1940s, the comic strip took up half a broadsheet, which back then was much larger than the broadsheet sizes for newspapers of today. But by the time Bill Watterson and Gary Larson gave up on two of the most popular comic strips of all-time (Calvin and Hobbes and The Far Side), the newspaper strip had shrunk to 3 tiny postage stamp sized panels shoved into the back end of the feautres/lifestyle sections of most papers.

Then the internet hit newspapers big time, as people went online for their news. They got the stories for free. And newspapers could no longer compete. Comic strips were a casualty of that shift in media.

So right now, survival instinct is kicking in for the comic art form. The internet allows both the strip and the comic book format room to breathe, and easier distribution. Penny Arcade is what I feel to be the best example of the modern comic strip, giving renewed life to the art that newspapers were choking out of their shrinking pulp empire. Penny Arcade can publish in color (because it’s online), can publish unorthodox sizes (because it’s online) and offer their content for free (online). They then make a killing selling collected editions (many sales being made … online) of the same content daily readers get for free. They adapted and brought the art form onto a new stage. Meanwhile … print media continues to not adapt.

Comic Books are starting to finally embrace the changing landscape. ComiXology offers Marvel, DC and independent publishers through their mobile application. You can purchase and download all of your favorite comic books directly to your iPhone, Android, iPad or Kindle. You no longer need to go to direct order hobby shops. Your comic books no longer need to take up physical space. They’re right there at your fingertips — your entire collection just a thumbtap away. While they may be a bit unwieldy and tiny on the smartphones, they look rather luxurious and eye-popping on a larger device like a Kindle (where, not so surprisingly, I’ve been reading my comic books in 2012).

That brings me to the Kindle — or more generally, the reader devices and THIS BLOG HERE from Michael Essany at Daily Deal Media. The article resonates with me. A number of my close friends used to work at Borders Books and Music in their twenties. Last year the local Borders closed up shop. And all we currently have in our local area is a Barnes and Noble located in the Christiana Mall.

The most striking thing about their store in the mall is when you walk in their front door you are immediately overwhelmed by their eBook section, with large signage telling you all about the Nook (their version of the Kindle).

That sight at my own local big box book store really drives home Essany’s second paragraph, when he writes, “Although many avid readers are mourning the noticeable loss of traditional big box and mom-and-pop book retailers, the economics of eCommerce and the popularity of eBooks are quickly dispatching publishing companies, paperback publications, and even print magazines to the trash receptacle of history.”

The point Essany is making was driven home even further when I attempted to make a quick trip to that Barnes and Noble for a book on a work-related topic: Web Design. I knew the right section of the store to go to, but couldn’t find the title I was looking for. I used their interface terminal in the store to look that title up. Apparently it was in stock as an eBook. And I could order a regular print version of it from there, but had to order it as an online purchase and have it delivered to my house days later. The entire point of my trip was to get the book that day, otherwise I’d have gone online when I got home from work instead. So I kept browsing, and found every single book they had under the topic of web design was only available either through an online purchase or as an eBook.

E-Commerce is winning

In terms of printed media E-Commerce is absolutely dominating. Essany cites a statistic to back up this outlook, writing that according to the Yankee Group (a research company we’ve cited ourselves when they made projections on The Future of Mobile Payments), consumers will purchase approximately 381 million eBooks next year with an average selling price of $7.

Most impressive

My own research for this very blog during last year’s holiday shopping season demonstrated what to me has become a very obvious aspect of the economy: shopping online is a common thing for people to do. That means E-Commerce is making buckets of money. Each one of those transactions are part of the payment processing industry. The foundation is there. People have found the convenience of shopping online so powerful that it outweighs the risk of fraud. So more and more people have taken to solving their shopping problems online. I know that I myself do this. It’s so much easier to look for a product online and know you’re getting what you want with a few clicks, than it is to go trudging out to a store that may or may not have the item you want.

Last year in a Blog Post about the upcoming holiday shopping season, I reported “A 2010 survey conducted by Google and OTX found that 35% of internet users start their holiday shopping prior to the end of summer, months ahead of Black Friday. This trend is only continuing to grow as consumers find online shopping convenient to their shopping habits, easy to do, and the wide selection lets them find great deals on price.”

This trend in shopper behavior combines with the rise of virtual media like eBooks like Voltron to form a very powerful lion-fisted, right-left combo to the solar plexus of Print Media’s crumbling empire.

And you know what? I’m OK with this.

I’m a voracious reader. But I’m also under the thrall of the convenience of online shopping. I truly do turn to the internet first for most products I’m interested in. This is heightened when I want to purchase a book, a magazine or a comic book. It’s just so much easier. The only time I’ve wanted to wander into a book store to buy a book was when I wanted it right then, with no wait on delivery. And I found the remnants of the only big chain bookstore in my local area to have already forced the decision upon me: If I wanted a book about web design, I needed to go directly to the web to get it.

I’ve been using the ComiXology app this year. And when the company that I once worked for (Valiant Comics) as a production intern returned to the comic book industry after a long hiatus, publishing a comic book I once did post production work for (X-O Manowar), I immediately jumped onto my phone to purchase it. I find that I read more web comic strips than I ever read in a newspaper. I find I go to the web for my news. Or my phone. I’ve even found myself reading straight up only published electronically eBooks this year. I still prefer printed books, but for me they’ll be online purchases. I’ll buy the collected editions of comics I like, but do so online. I’ll buy printed books of titles I really just want to curl up with and turn the pages of, but I’ll make the purchase online. It’s gotten so pervasive in my life that I now buy tickets to sporting events online, brands of tea I can’t find at my local supermarket online, all of my roller derby referee equipment and rules books online. I even bought my ticket to The Avengers on my phone through Fandango and had it delivered to my phone as a mobile ticket.

E-Commerce is where it’s at. And publishers of the written word need to embrace this shift. Maybe it’s easier for me to do so because I work in the payment processing industry and get to see firsthand how big and booming E-Commerce is.

{kind=link}

{kind=link}

{kind=link}