This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is Discount Rate.

Discount Rate

The simple definition of the term Discount Rate as it applies to merchant accounts — it is a combination of the fees charged by the card acquirer to the merchant for processing payment card transactions. So what that’s really saying is the Discount Rate is what the payment processor charges the merchant so that they can make profit off of the transaction — it’s not really a discount in any sense of the word when defined like that.

So let’s break this down a little more to understand this buzzword beyond just the obvious. A Merchant Account has a variety of fees. Some of these fees are charged periodically, such as a monthly service fee. Others can be charged on a per-item or percentage basis, such as a Chargeback Fee. Some fees are set by the merchant account provider.

The majority of the per-item and percentage fees, however, are passed through the merchant account provider to the credit card issuing bank according to a schedule of rates called interchange fees, which are set by Visa, Discover, and Mastercard.

Each merchant services provider has real costs in addition to the wholesale interchange fees, and creates profit by adding a mark-up to all the fees they have to take on to provide their services in the first place. The discount rate comprises the combination of dues, fees, assessments, network charges and that additional mark-up merchants are required to pay for accepting credit and debit cards. The largest of these fees by far is the Interchange fee.

There are a number of pricing models that merchant services providers utilize, but Host Merchant Services uses the Interchange Plus pricing plan.

Interchange Plus pricing means that the acquirer charges you a variable MSC consisting of the cost price plus a fixed markup. Interchange Plus Pricing is exclusively how we quote at Host Merchant Services. Interchange Plus, also known as Cost Plus, pricing gives the customer a fixed rate over published Interchange Fees. This pricing format is normally quoted as a discount rate (percentage fee) along with a per item or authorization fee. The great thing about Interchange Plus pricing is that you always know exactly what you are paying to your processor to services your account. Think of Interchange, and all the associated fees, as an unavoidable cost. No matter who you process with, you have to pay these fees. They may be labeled differently, or wrapped up in a confusing pricing tier, but one way or the other, you are paying Interchange fees. By understanding the markup you pay over Interchange, you know exactly what you pay to your processor and exactly what is going to the card associations. That allows you to make a decision on whether or not the markup seems reasonable for the service you get and choose your processing partner accordingly.

Here’s a small graphic explaining the basics of how Interchange Plus works.

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is Debit Cards.

Debit Cards

A debit card (also known as a bank card or check card) A debit card looks like a credit card but works like an electronic check. The thin plastic card that provides the cardholder electronic access to a bank account at a financial institution. Payments made with Debit Cards are deducted directly from that checking or savings account. If a cardholder uses a debit card at a retail store for example, the cardholder or the cashier can run the debit card card through a scanner — oftentimes the very same terminal credit card purchases are swiped through. This action enables the financial institution to verify electronically that the funds are available and approve the transaction. Most debit cards also can be used to withdraw cash at Automated Teller Machines (ATMs).

Unlike credit and charge cards, payments using a debit card are immediately transferred from the cardholder’s designated bank account. This difference is key in one sense, as it creates a completely different set of protocols and standards for debit transactions in the payment processing industry. This can be seen most recently in the Durbin Amendment of the Dodd-Frank Act. The financial reform legislation set a hard cap on debit card swipe fees. But has absolutely no affect on credit card transactions.

For many consumers, the card they carry can be used as both a credit and a debit card when presenting it at a retail store for purchase or using it online. Oftentimes, a consumer is asked to choose between credit or debit.

For the consumer the distinction can have this impact:

The card’s individual rewards program can vary depending on debit or credit. In many cases, a credit transaction reaps greater points or rewards from these types of programs.

A debit transaction can allow for cash back right at the point of sale.

A credit card transaction can have stronger protection. It takes time before it is “batched” out by the merchant. And the credit cards themselves have more fraud protection layers than debit cards typically have.

For the merchant and for the banks involved the impact is this:

The transaction network that the purchase is run through is separate for debit and credit.

The fees associated with the transaction are different. After Durbin, the fees face a hard cap ceiling on what the merchant can be charged. Credit has no such ceiling and so smaller transactions — say purchases under $10 — can end up costing a merchant a bit more in fees.

The distinction between credit and debit was stronger in the 1980s and 1990s, but it still exists. It’s worth knowing what your options are as both a consumer and a merchant.

Today The Official Merchant Services Blog is going to get a bit personal, for me at least. I’m going to take a moment to talk about print media, and its withering industry. Or, think of it this way: I’ll be talking about the rise to power of E-Commerce — the industry that has helped deliver excruciating body blows to print media over the past decade, knocking it to the mat time and time again.

My history with print media goes back. Way back. All the way back to the beginning of my own career. I’ve worked for four different newspapers, the most high profile being the Asian Edition of the Wall Street Journal at the turn of the millennium. I’ve illustrated various comic strips and published my own comic book. I’ve worked for a printing company in Delaware. Along the way I’ve essentially learned how to make a printed publication from beginning to end; the only skill I lack is the ability to actually push the buttons on a printing press. But every other step, from concept to creation to pre-production to layout and design to editorial to post production I’ve done during my career.

And all of these skills are endangered because of E-Commerce. (Well not really; most the skills translate easily into the virtual media world which is why I’ve been able to transition my career; but everything involving production kind of gets tossed out the window, replaced with skills revolving around web safe colors, pixel sizes and screen ratios).

A really vast, somewhat oversimplified recap of the internet’s impact on newspapers, comic books and book publishing can be summed up by my own career. One of the companies I used to work for, Gannett (publisher of the USA Today), used to have an empire built on small to mid-size suburban community newspapers. They were everywhere. Including Lansdale, PA — where I worked for a time. Gannett was slow to embrace online news though. And the transition from the late 1990s to the aughts left Gannet in a position to streamline and essentially drop a lot of those small and mid-size papers from its stable.

At the same time, I was trying my best to get some traction going in my quest to be a freelance illustrator for comic books. Things didn’t quite work out. I never became the regular artist on The Flash or Spider-man like I dreamed of doing when I was younger. I did however get paid for doing a few projects and got quite a bit of my art published.

Still, steady work was hard to find. And the comic book industry appeared to be dying because of the problems that all of print media now faced.

The major publishers (DC Comics and Marvel Comics) were no longer selling millions of copies of their books. In fact, sales these days are horribly low, with top books barely cracking 100k in sales volume. This reduction in volume can be linked to its distribution channel. Comics stopped appearing in mainstream outlets because the sole distributor of the material, Diamond, only catered to specialized direct market hobby shops (comic book shops). You couldn’t find them at the local supermarket or the local 7-11 anymore. The comic book “rack” was gone. I’d go so far as to make the claim that today, in 2012, the two major comic book companies are really just stables for intellectual properties. Disney and Time Warner wanted Marvel and DC not so much for their ability to publish millions of paper periodicals every month. Instead they wanted the comic book companies for the properties that could at any moment be turned into $100 million blockbuster movie franchises.

So the comic book industry ended up being sold as a niche hobby, and stopped being made as a mass medium periodical. Big companies bought the two biggest publishers of those comics just to keep the ideas and licensing on ice for future movie potential. Print media, it is dying.

And then then there was the issue with comic strips. Newspapers shrunk the comics section over decades. When Action Comics first appeared in newspaper print in thge 1940s, the comic strip took up half a broadsheet, which back then was much larger than the broadsheet sizes for newspapers of today. But by the time Bill Watterson and Gary Larson gave up on two of the most popular comic strips of all-time (Calvin and Hobbes and The Far Side), the newspaper strip had shrunk to 3 tiny postage stamp sized panels shoved into the back end of the feautres/lifestyle sections of most papers.

Then the internet hit newspapers big time, as people went online for their news. They got the stories for free. And newspapers could no longer compete. Comic strips were a casualty of that shift in media.

So right now, survival instinct is kicking in for the comic art form. The internet allows both the strip and the comic book format room to breathe, and easier distribution. Penny Arcade is what I feel to be the best example of the modern comic strip, giving renewed life to the art that newspapers were choking out of their shrinking pulp empire. Penny Arcade can publish in color (because it’s online), can publish unorthodox sizes (because it’s online) and offer their content for free (online). They then make a killing selling collected editions (many sales being made … online) of the same content daily readers get for free. They adapted and brought the art form onto a new stage. Meanwhile … print media continues to not adapt.

Comic Books are starting to finally embrace the changing landscape. ComiXology offers Marvel, DC and independent publishers through their mobile application. You can purchase and download all of your favorite comic books directly to your iPhone, Android, iPad or Kindle. You no longer need to go to direct order hobby shops. Your comic books no longer need to take up physical space. They’re right there at your fingertips — your entire collection just a thumbtap away. While they may be a bit unwieldy and tiny on the smartphones, they look rather luxurious and eye-popping on a larger device like a Kindle (where, not so surprisingly, I’ve been reading my comic books in 2012).

That brings me to the Kindle — or more generally, the reader devices and THIS BLOG HERE from Michael Essany at Daily Deal Media. The article resonates with me. A number of my close friends used to work at Borders Books and Music in their twenties. Last year the local Borders closed up shop. And all we currently have in our local area is a Barnes and Noble located in the Christiana Mall.

The most striking thing about their store in the mall is when you walk in their front door you are immediately overwhelmed by their eBook section, with large signage telling you all about the Nook (their version of the Kindle).

That sight at my own local big box book store really drives home Essany’s second paragraph, when he writes, “Although many avid readers are mourning the noticeable loss of traditional big box and mom-and-pop book retailers, the economics of eCommerce and the popularity of eBooks are quickly dispatching publishing companies, paperback publications, and even print magazines to the trash receptacle of history.”

The point Essany is making was driven home even further when I attempted to make a quick trip to that Barnes and Noble for a book on a work-related topic: Web Design. I knew the right section of the store to go to, but couldn’t find the title I was looking for. I used their interface terminal in the store to look that title up. Apparently it was in stock as an eBook. And I could order a regular print version of it from there, but had to order it as an online purchase and have it delivered to my house days later. The entire point of my trip was to get the book that day, otherwise I’d have gone online when I got home from work instead. So I kept browsing, and found every single book they had under the topic of web design was only available either through an online purchase or as an eBook.

E-Commerce is winning

In terms of printed media E-Commerce is absolutely dominating. Essany cites a statistic to back up this outlook, writing that according to the Yankee Group (a research company we’ve cited ourselves when they made projections on The Future of Mobile Payments), consumers will purchase approximately 381 million eBooks next year with an average selling price of $7.

Most impressive

My own research for this very blog during last year’s holiday shopping season demonstrated what to me has become a very obvious aspect of the economy: shopping online is a common thing for people to do. That means E-Commerce is making buckets of money. Each one of those transactions are part of the payment processing industry. The foundation is there. People have found the convenience of shopping online so powerful that it outweighs the risk of fraud. So more and more people have taken to solving their shopping problems online. I know that I myself do this. It’s so much easier to look for a product online and know you’re getting what you want with a few clicks, than it is to go trudging out to a store that may or may not have the item you want.

Last year in a Blog Post about the upcoming holiday shopping season, I reported “A 2010 survey conducted by Google and OTX found that 35% of internet users start their holiday shopping prior to the end of summer, months ahead of Black Friday. This trend is only continuing to grow as consumers find online shopping convenient to their shopping habits, easy to do, and the wide selection lets them find great deals on price.”

This trend in shopper behavior combines with the rise of virtual media like eBooks like Voltron to form a very powerful lion-fisted, right-left combo to the solar plexus of Print Media’s crumbling empire.

And you know what? I’m OK with this.

I’m a voracious reader. But I’m also under the thrall of the convenience of online shopping. I truly do turn to the internet first for most products I’m interested in. This is heightened when I want to purchase a book, a magazine or a comic book. It’s just so much easier. The only time I’ve wanted to wander into a book store to buy a book was when I wanted it right then, with no wait on delivery. And I found the remnants of the only big chain bookstore in my local area to have already forced the decision upon me: If I wanted a book about web design, I needed to go directly to the web to get it.

I’ve been using the ComiXology app this year. And when the company that I once worked for (Valiant Comics) as a production intern returned to the comic book industry after a long hiatus, publishing a comic book I once did post production work for (X-O Manowar), I immediately jumped onto my phone to purchase it. I find that I read more web comic strips than I ever read in a newspaper. I find I go to the web for my news. Or my phone. I’ve even found myself reading straight up only published electronically eBooks this year. I still prefer printed books, but for me they’ll be online purchases. I’ll buy the collected editions of comics I like, but do so online. I’ll buy printed books of titles I really just want to curl up with and turn the pages of, but I’ll make the purchase online. It’s gotten so pervasive in my life that I now buy tickets to sporting events online, brands of tea I can’t find at my local supermarket online, all of my roller derby referee equipment and rules books online. I even bought my ticket to The Avengers on my phone through Fandango and had it delivered to my phone as a mobile ticket.

E-Commerce is where it’s at. And publishers of the written word need to embrace this shift. Maybe it’s easier for me to do so because I work in the payment processing industry and get to see firsthand how big and booming E-Commerce is.

The Official Merchant Services Blog begins our second year of blogging with a look at one of our favorite topics: E-Commerce.

2011 saw huge gains for online shopping. As reported in The Official Merchant Services Blogon Cyber Monday, online shopping was strong on Black Friday. IBM research unit Coremetrics stated that 20% more consumers shopped online Black Friday 2011 than did in 2010. The data collected also states that 39% more online shopping happened on Thanksgiving Day 2011. The ease of online shopping is infiltrating the traditional brick-and-mortar retail event and Host Merchant Services‘ analysis of it held true –– sales numbers across the board rose from 2010, so overall Black Friday had a boost for retail, but clicks from e-commerce continue to grow and cut into the sales from bricks.

Also, mobile payments saw a huge increase during the holiday shopping season. According to this article from Seeking Alpha, mobile payments business increased 500% from 2010 on Black Friday. According to the article, PayPal mobile reported the huge increase, coming in at 511% to be exact. PayPal Mobile also noted that there was a 350% increase in mobile shopping on Thanksgiving 2011 when compared to 2010.

The Numbers Keep Coming In

This article by Internet Retailer demonstrates that Black Friday was just the beginning. There were more than 3,000 transactions totaling $141.6 billion in 2011 in the marketing, media, technology and service industries according to data collected by investment banking firm Petsky Prunier LLC. Of those transactions the E-Commerce and digital media segment was the most active, with 1,159 deals valued at more than $44 billion.

All of this activity demonstrates strength in the E-Commerce industry, and suggests that 2012 is a year primed for continued growth and success — which combines with the already rampant predictions of success for Mobile Payments within the E-Commerce industry.

Comparing the recent success to the success of internet companies in 2000 and 2001, the article tries to figure out if the bubble will burst like it did back then for tech companies. The author’s opinion is that the similarities are only on the surface, and that the two situations are vastly different — suggesting that in the end, it’s not a bubble that is going to burst but rather an industry that is going to grow and evolve. The article looks specifically at the E-Commerce sector in India, but does spend time detailing the big picture globally.

Online Shopping is Now Commonplace

To really underscore the potential growth that E-Commerce has in 2012, this article from Daily Deal Media talks about how popular online shopping is becoming with moms. The article cites a BabyCenter survey which suggests that: “71% of moms regularly turn to websites such as shopping engines and review sites to compare prices. Another 56% admit to searching for coupons or digital discount opportunities on a regular basis.”

This is a compelling point in regards to the overall picture of E-Commerce. It has become more and more commonplace in everyday life for shoppers around the world. Mothers are turning to it for the convenience of being able to get shopping done quickly and efficiently, according to the article. And it is just become an ingrained part of our economy, fueling the potential for further growth.

Mobile Payments Big Problem

The potential growth for Mobile Payments is huge. But the one thing holding it back in the U.S. is security. Just as online shopping has become more and more commonplace, people have gotten comfortable with making payments online. That brings risk, as phishing scams and credit card fraud has increased. But security standards like the PCI DSS have helped to make the mainstream comfortable with clicking the pay button and giving out their payment information.

Mobile Payments, however, are not quite there yet in terms of acceptance. This article from the Chicago Tribune discusses the looming security issues that the mobile payments market faces. As the article states: “While the first mobile virus dates back to June 2004, risks from hackers remained limited because of the relatively small size of the market. But this has changed with the surge in the smartphone segment, which this year outgrew the PC market, and the new dominance of Google’s Android software. The emergence of mobile payments, which allows shoppers to swipe their phones at a cash register, is whetting the interest of hackers and data thieves.”

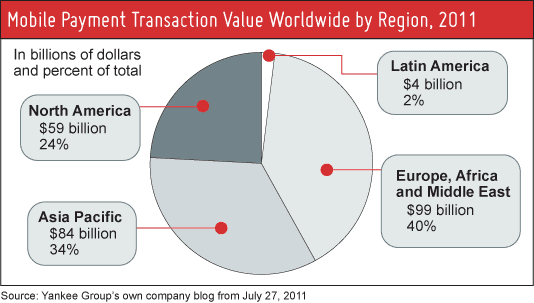

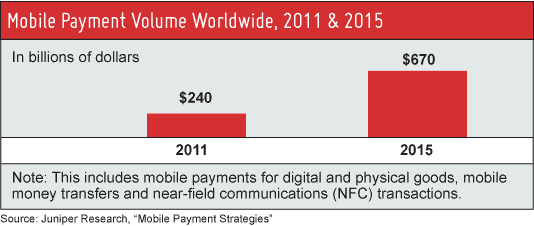

The article states that fewer than 5% of smartphone users have security software installed on their device, according to Juniper Research — the same Juniper Research that predicts Mobile Payments will increase to a $670 billion industry by 2015. And a study by Deloitte cited in the article suggests that for companies in the technology, media and telecom sector expect data stored on staff mobile devices to be their biggest security headache in 2012.

Essentially that’s the biggest obstacle holding back the Mobile Payments industry. The sheer convenience the technology brings to the payment industry is extremely powerful and so despite security concerns it continues to be developed and pushed. 2012 will see growth in the industry, despite the security issues. And as consumers get more and more familiar and comfortable with the phone swipe style of payment, the industry will boom.

A List for 2011

And just for fun, here’s a list from Mashable.com detailing who they think were the biggest winners and losers from 2011 in E-Commerce.

Their winners include: Amazon, Apple, Wal-Mart and Gilt Groupe.

Their losers include: Barnes and Noble, HP, Netflix and Sony.

{kind=link}

{kind=link}

{kind=link}