According to an October report published by eMarketer, a respected online publication dedicated to the digital marketing industry, the mobile payments service known as Apple Pay is now more popular than its counterpart developed by the Starbucks Coffee Company. Since about 2014, the Starbucks app, which started off as a digital version of its successful gift and rewards card, had been the most widely used mobile payments platform in the United States, but statistics crunched by eMarketer indicate that this is no longer the case.

Top Mobile Payment Apps

More than 27 million purchase transactions and payments were settled with Apple Pay in 2018, a figure that eMarketer expects will increase to 30.3 million by the end of 2019, thus representing a 47.3% share of the “contactless” or Near Field Communications (NFC) payments market. It should be noted that Apple Pay is accepted at Starbucks, whereas the Starbucks mobile app only works at the company’s retail locations equipped with NFC point-of-sale terminals.

The holiday shopping season happens to be very busy for Starbucks, particularly with its pumpkin spice flavors and often controversial choice of coffee cup designs, but this will not allow the company to retake its place atop the mobile payments totem pole. The number of active Google Pay users, who are those making at least one NFC payment within a six-month period, will climb to 12.1 million, less than half of Starbucks mobile app users, who can easily be assumed to be even more active because such is the nature of delicious caffeinated beverages and tasty gourmet treats. Samsung Pay comes in at third place with 10.8%, just a sliver of the market share it holds in places such as South Korea.

Both Companies Benefit

For payment processing analysts, comparing Apple Pay to the Starbucks app is an apples to oranges situation. While it is true that Apple now commands nearly 50% of the American NFC payments market, Starbucks is the true leader because this is a mobile app that can be installed in iOS and Android devices; in fact, it worked on Windows Mobile devices until about 2017. As for Apple Pay, the popularity of the iPhone is what is really boosting this digital wallet, and it could be argued that the Apple Card, which is a very recent product still being rolled out, will likely enhance Apple Pay.

It could be argued that the new Apple Card could very well be the factor that can realistically propel Apple Pay past Starbucks. There is one thing that coffee lovers enjoy as much as coffee itself, and that is being rewarded for their good taste; this is where the Starbucks mobile app excels, and it is what the Apple Card is going for. The current cash-back rewards program offered to Apple Card holders is pretty standard; should Apple spice it up with greater rewards for using the card in conjunction with Apple Pay, it would entice greater use of this iOS digital wallet. In the end, providers of payment processing services stand to benefit from this competition.

Google Pay allows Android phones, tablets or digital watches to make tap-to-pay purchases. Near field communication (NFC) allows the Android device to transfer the credit card information over to a point of sale system, making transactions fast and easy. By saving your cards to your Google Account, you’ll receive the same rewards and discounts when you use Google Pay as you would with a normal credit card. Google Pay also offers peer-to-peer and online payment services. The following are the stores, apps, sites, and transit systems that accept Google Pay:

Which Retailer In The US Accepts Google Pay In 2024?

A store that accepts Apple Pay or Samsung Pay will also accept Google Pay. You might notice the Apple Pay symbol on store entrances, but it’s often used as a general term for all mobile payments. Apple Pay and Google Pay use the same NFC technology, allowing tap-and-pay transactions.

However, it’s worth noting that not all big names in the US have adopted mobile payments. Some smaller businesses haven’t made the switch, primarily due to the costs associated with NFC terminals provided by banks, which can eat into their profits.

You can use Google Pay to buy goods or services at the following retailers:

MTA Metro-North and Long Island railroads New York metropolitan area

Portland Hop Fastpass

What Is Google Pay?

Google Pay is a digital payment service by Google that allows users to make purchases using their Android devices at physical stores and on compatible websites and apps, including the Google Play Store. In 2023, Google Pay is the most trusted mobile payment app with 25.2 million users in the US alone.

To use it, people connect their credit or debit cards to Google Pay. This linked card is then used for both in-person and online transactions. For payments at stores using Android devices, Google Pay employs NFC to communicate with payment terminals. Additionally, when users are logged into their Google account on the Chrome browser, they can use Google Pay on websites offering this payment option.

How Google Pay Works?

ApplePay, GooglePay, and other contactless payments are gaining acceptance.

To start using Google Pay, download the Google Pay app and link it with your preferred payment method, such as a credit or debit card. While many banks, credit unions, and other financial services support Google Pay, confirming if your specific card is compatible is essential.

Once set up, Google Pay allows you to make online and in-store payments. For in-person transactions, tap your phone on the payment terminal, similar to a contactless card. When shopping online, choosing the Google Pay option at checkout streamlines the process by automatically filling in your payment and shipping details, eliminating the need for manual entry each time you make a purchase.

Safety Features of Google Pay

When transacting with Google Pay, it uses a special encrypted number instead of revealing your credit card details. This adds an extra layer of security.

Plus, if you ever lose your device, you can use Google’s Find My Device feature to erase any important data remotely. For added security, you also have the option to log into your Google Pay account from another device and remove any linked cards or bank accounts.

Understanding Google Pay Fees

Google itself doesn’t impose any fees when you use Google Pay for tap-and-pay or online transactions. However, it’s essential to note that your card issuer might have charges associated with your purchases.

Transaction Charges:

While Google Pay doesn’t have transaction fees, any fees applicable to your physical card usage still stand. For instance, standard interest charges and penalty fees may apply if you use a credit card via Google Pay and don’t clear your bill on time.

However, Google Pay is rolling out some additional “convenience fees” for some specific transactions. As of 2023, the stance Google has around the charges by its application is unclear. Apart from this, there are no charges currently charged by the application Google Pay.

Credit Card Linked With Google Pay:

When you link a credit card to Google Pay, remember that your credit card company might charge the merchant a fee of up to 4%.

Some merchants may then pass this fee to you, adding it to other transaction charges. This could mean you end up paying as much as 6% extra for your purchase. To avoid unexpected costs, asking merchants about fees before using Google Pay is a good idea. A linked debit card or bank account can help sidestep these higher charges.

Using Google Pay Abroad:

If you use Google Pay while traveling or making purchases in a foreign currency, be aware of potential fees from your bank or card provider.

These include foreign fees, typically around 3%, applied to non-USD transactions. Remember that these fees can vary based on the specific card you have linked to Google Pay.

Conclusion

In 2023, Google Pay emerged as a versatile digital payment solution, trusted by millions in the US. Offering convenience across various platforms—from retail giants like Costco and Macy’s to popular apps like Airbnb and Doordash—it simplifies transactions with robust safety measures.

While it generally doesn’t impose fees, users should consider potential card issuer charges and international transaction fees. Overall, Google Pay is a reliable tool for seamless and secure payments across various outlets.

Frequently Asked Questions

Q: Where can I use Google Pay for transactions?

Absolutely! You can use Google Pay or Google Wallet wherever you spot those handy contactless or Google Pay symbols. Keep an eye out for them on the payment terminal screen or cash register during checkout.

Q: Can I use Google Pay for purchases at Walmart in 2023?

Currently, Walmart doesn’t accept Google Pay as a payment method. It’s always good to check for your preferred stores’ most current payment options.

Q: How do I get started with Google Pay?

Setting up Google Pay is a breeze. Locate the app on your phone, and if it’s not already there, just grab it from Google Play. Add your card linked to your Google account by confirming a few details. You can even snap a picture to add a new card. Once everything’s set, unlock your phone, tap, and you’re ready!

Q: Is Google Pay secure?

Absolutely! Google Pay offers enhanced security compared to traditional magnetic-stripe cards. It’s not just convenient; it’s also swift. Unlike chip card transactions that may take a bit, contactless payments with Google Pay process in a flash. Plus, you get a handy payment confirmation on your phone, making it easy to spot any fishy activity. In case of loss or theft, you can lock your device using Android Device Manager, securing your info.

Q: Can Google Pay be used for payments at Target?

Yes, you sure can! Target happily accepts any contactless payment, be it contactless credit/debit cards or digital mobile wallets. Simply tap your contactless card or mobile device over the payment terminal and follow the prompts on the reader screen.

Q: Does Walgreens support Google Pay?

Absolutely! Walgreens is all in for contactless payments. Whether tap-to-pay credit cards, Apple Pay, or Google Pay, they’ve got you covered. Just wave your contactless card or mobile device over the payment terminal and follow the prompts on the reader screen.

Generation Z represents a whopping 32% of the world’s population. As the first “digital native” generation that has never lived without the internet and technology, Gen Z sets itself apart in many ways. When it comes to the world of payments, Gen Z has very different expectations than even millennials and overwhelmingly prefers cashless payments — although with much higher standards for design, convenience, and security than other generations.

How Popular Are Digital Payments?

According to a U.S. Mobile App Report from 2017, 70% of consumers in Gen Z have made app-based mobile payments in the last year, surpassing all other generations. A more recent survey by BillTrust found that 79% of Gen Z responders use a digital payment service at least once every month.

Generation Z Is Price Sensitive

Generation Z, and young millennials too, are much more concerned with price than older adults, and much less likely to show any brand loyalty. As many as 80% of participants said that price was the most important factor to them when making a purchase.

Having grown up during the Great Recession of the late 2000s and early 2010s, many Generation Zers watched their parents struggle, which has led to something of a more frugal and pragmatic attitude. This more price sensitive attitude plays into the strengths of the financial tech companies as they can offer services at a low cost.

Generation Z Cares More About Security

Surveys have also found that Generation Z cares strongly about security, with as many as 33% of respondents to one survey claiming that they would stop dealing with a company immediately were their data breached. On top of this, 67% of surveyed Gen Zers would adopt name brand products when they need to seek assurance that their standards will be met.

Gen Zers hold privacy, ethics, and security seriously and demand transparency when it comes to cashless payments.

Generation Z Isn’t Tolerant of Friction

Having grown up in a world that’s fully accepted digital technology, Generation Z is completely at home with digital and real-life experiences coexisting. Because of this, studies have found that they will expect things to run smoothly, and they will be less tolerant than others when things don’t. With the rise of mobile payments, this plays into this generation’s hands and provides them with a system they’re perhaps more comfortable with.

A clunky user experience or an overly complicated system could be enough to lose this generation as a customer. After years of technological revolution and refinement, this is a generation that expects the best.

What Generation Z Is Looking for in Credit Card Processing

It would seem that what is most important to Generation Z when it comes to payments is a seamless, frictionless experience that fits easily around their lifestyles. This means customized credit card processing and payment solutions, transparency, security, and convenience. Having instant, seamless payments is of huge importance, especially when looking to win their loyalty and trust.

The next platform that caters to Generation Z will likely combine all forms of financial services in one from digital payments and banking to investments and loans to further capture the interest of this digital generation.

Using near-field communication (NFC), a Galaxy smartphone (or even smartwatch) that supports Samsung Pay allows you to make quick and easy retail purchases. All without having to fumble around with your wallet or purse. When you launch the Samsung Pay app on your phone, you simply hold the phone above the credit card terminal and then tap-and-go.

Here’s what really puts Samsung Pay ahead of the competition. Existing card readers recognize Samsung Pay. For terminals that do not support NFC, Samsung Pay also works with MST (Magnetic Strip Technology), enabling consumers to make a contactless payment on a terminal even with the old school magnetic strip technology. The MST technology differentiates Samsung Pay from Apple Pay and Android Pay, both of which are only equipped to use NFC technology. While the other mobile wallet apps are limited to merchants who provide NFC technology, Samsung Pay can be used anywhere traditional credit and debit cards are accepted.

How to set up Samsung Pay:

Open the app on your phone

Scan your credit card

Use your fingerprint or PIN to secure the account along with an authorization code provided by the app

Once you’re ready to use Samsung Pay, swipe up from the bottom of the display

Swipe left or right to choose the card to use

Verify your fingerprint for the app or enter your PIN

Touch the back of your phone on the reader or hover your phone over the reader

Your phone will vibrate indicating payment

The following banks and services support Samsung Pay:

American Express

Mastercard

Visa

Bank of America

Chase

Citi

JP Morgan Chase

PNC

US Bank

Samsung Pay has expanded to the following countries and regions:

The expected global rollout of 5G technology is predicted to bring many changes to today’s connected global economy. With real-time, high-speed data flow, 5G is likely to fuel even further expansion of mobile payments and change the credit card processing industry on a fundamental level. Here’s what 5G may mean for the future of mobile payment technology.

What Is 5G?

A major technology shift is occurring that will bring a big update to the wireless technology that delivers data to cell phones. 5G refers to the fifth-generation cellular network which will be a big step ahead of today’s wireless technology, 4G, by offering incredibly fast mobile internet speeds that will allow users to download movies within seconds. That’s about 20 times faster than the 4G experience. 5G technology won’t just bring faster speeds; it will also reduce latency or lag which happens when signals pass between different carrier switching centers.

In addition to cell phones, the technology will also impact security systems, drones, and even vehicles. To get the full benefits of 5G, once the rollout is complete, users will need a compatible new phone and cell phone carriers will need to upgrade to new transmission equipment.

How Will 5G Technology Change Credit Card Processing?

The payment processing industry is expecting a big shakeup when 5G technology is finally rolled out. With dramatically faster speeds and reduced latency, 5G can:

Streamline transaction processes

Increase transaction speeds

Improve the accuracy of fraud prevention

Support a more user-friendly experience

5G technology can revolutionize the mobile shopping experience. For example, it makes it easier to support virtual reality shopping to allow consumers to see what an item will look like in their home before buying or go through every step of buying a car — including the credit check, receiving personalized financing options, and funds availability — with mobile technology.

Increased speeds won’t just improve customer experience; speed also supports better fraud prevention. Fast data transmission allows banks to quickly verify data like geolocation and merchant ID to avoid errors. These factors can increase consumer confidence in digital payment technology to potentially sway more people to change how they pay.

All of these benefits may support increased adoption of mobile payments, especially in the United States which is far behind China and other areas of the world in terms of adopting mobile payment technology.

While China boasts a mobile payment usage rate of more than 80%, the adoption rate in the U.S. is less than 10%. In the United States, debit and credit cards are much more widely accepted than in other regions of the world, offering an alternative to paying without cash.

To accept a mobile payment, merchants need the right hardware which are tailor-made for mobile businesses. By improving security and transaction speeds while opening the door to more advanced mobile payment options, 5G may just help increase the adoption rate of mobile payment technology in the U.S.

As the debate in the United States rages on over gun laws, some companies have been taking sides by choosing to take action. Visa, however, is one company that has refused to wade into the political fray. Instead, it has opted to continue along doing business as it has been in regards to mobile payments.

An announcement from the company came in early August that it would not block mobile payments for gun purchases. Visa Chairman and CEO Alfred Kelly made the announcement after back-to-back mass shootings in Texas and Ohio thrust issues surrounding guns back into the news. It is not a change of course for the company; instead, it was merely a confirmation that things will not be changing in regards to gun purchases.

The company’s stance regarding mobile payments for gun purchases is a different one than some of its competition has taken. PayPal and Square have opted to not allow their services to be used for such purchases.

The rationale expressed by Visa CEO Alfred Kelly as to why the company will continue to support mobile gun purchases essentially comes down to it being simply a matter of not dictating morality to the company’s customers. It is legal for people to buy guns in the United States; therefore, the company will continue to process those purchases- just as it does other things that are legal but may be considered controversial by some.

That is not to say, however, that Alfred Kelly does not hold views regarding gun legislation in the United States. In an interview with CNBC, he expressed an interest in seeing lawmakers do more in regards to gun laws. However, no matter his personal views, he is not currently interested in applying them to the company that he heads up.

The company is not alone in this view, either, in regards to not dictating morality to its customers. Mastercard has also taken a similar stance. Its CEO Ajay Banga expressed similar sentiments as those of Alfred Kelly- refusing to determine what is right or wrong. As far as he is concerned, if it is legal to own an item his company will help customers purchase it.

Meanwhile, CEOs at other companies have taken a less neutral stance regarding guns. Apple CEO Tim Cook is one notable example of this. After the shootings in El Paso and Dayton, he took to Twitter demanding action.

The Japanese government and Visa have teamed up in an effort to bring mobile payments to the 2020 Olympics in Tokyo.

The payment giant is preparing new payment experiences for visitors, athletes, and citizens attending the 2020 Olympics, an effort that will support the “Cashless Japan” campaign that is designed to boost mobile payments to 40% by 2045 from today’s 20%.

Visa is currently working to increase acceptance of digital payments with merchants ahead of the Summer Games, especially in quick-service restaurants and convenience stores, while connecting athletes with the concept. Mobile payments technology will be featured at the Olympic Village, Olympic venues, and throughout Japan in an effort to improve the experience for fans.

In a press release, the payment network stated that Japan is a unique opportunity with “the world’s third-largest economy” with commerce that “remains predominantly cash-based.”

About one-fifth of payments in Japan are digital compared with 60% in the United States, 70% in China, and 90% in South Korea, which has one of the highest adoption rates in the world.

The payment technology sponsor for the Olympics is also planning unique innovations for the Summer Games, including wearable technology, new mobile applications that use digital cards, and biometric payment authentication.This isn’t the first time the payment giant has worked to improve digital payment acceptance for the Olympics. In 2016 at the Rio Olympic Games, payment-enabled rings were provided to athletes. These rings used NFC technology and microchips made by Gemalto. The rings were water-resistant and did not need batteries or charging. Nearly 4,000 NFC-enabled point-of-sale terminals were implemented for the wearables and also to boost mobile payment acceptance at important Olympic venues in the city.

The Japanese government and payment network hope that improving access to digital payment technology will give the typical Japanese person more reason to use digital payments in the future.

Japan has been slowly moving toward the global cashless trend for the last few years. Japan has made the “Cashless Japan” effort such a priority to reduce the need for manpower at retail stores as the country faces a declining and aging population and labor shortage.

The government has another incentive for boosting digital payment technology: shifting away from cash improves transaction transparency and makes it easier and more efficient to collect taxes. In 1997 after a financial crisis, South Korea was able to successfully push forward cashless transactions to boost its economy and control taxes by offering a tax deduction for credit card purchases, among other incentives.

In Japan, however, cash has remained king thanks to a low crime rate that allows citizens to feel safe carrying even large amounts of cash, readily available ATMs, and high trust in cash.

Making the shopping experience easier for the consumer is the goal of new e-commerce tools. Every year, the e-commerce industry is dynamically transforming, moving in the direction of personalization and new sleeker customer experiences, especially with the increasing integration of AI. Streamlining payment processes and providing multiple avenues of payment are only part of a merchant’s strategy in making paying for products online as easy as possible.

PWA = Progressive Web App

With mobile conversions on the rise – a whopping 55% increase in mobile sales for 2018, eCommerce is shifting. By 2022, it’s predicted retail sales via smartphone will reach $175.4bn. With this shift, retailers are dropping mobile apps for PWA entirely. PWA, or progressive web app, leverages web capabilities to deliver an app-like experience to consumer. Indexed by search engines, URL-accessible, PWA’s are deployed to servers, making the user experience more robust and dynamic.

W3C = World Wide Web Consortium

The W3C, or World Wide Web Consortium – the international community working to ensure the long-term growth of the Web, is aiming to simplify online payments for the sake of decentralization. Allowing browser native UIs to use previously saved data such as an address and card information to make web payments is the ambition of the W3C. “Web Payments” is the name of the standard and will enable consumers to tap a few times versus filling out the same information on every new site.

Multi-Currency

Rather than paying conversion rate fees, consumers now can choose multiple currency options on sites like Shopify. Instead of restrictions via a retailer’s local currency, consumers can use the currency they are accustomed to. Multi-currency options are gradually being rolled out.

Voice-Command Currency

With over 20% of search queries made via voice command, e-commerce has a huge opportunity for growth in the order-by-voice future. By 2020, experts predict 50% of searches will be done by voice command and so on. Retailers should start focusing on long-tail keywords and structured product data now to accommodate the future.

B2B = Business to Business

80% of B2B organizations accept orders and payment through their website, according to a BigCommerce survey of 500 such businesses. This data not only indicates the growth of e-commerce payments in B2B industries but also demonstrates the complexity of a B2B e-commerce channel, which also accepts payments via quote, ACH, terms, check, and PO.

Influencers – The Social Media Swipe Up

E-commerce businesses also need to embrace social media influencers and the “swipe to buy” revolution. Not only do e-commerce merchants need to be available by mobile, they need to be available by social – social media that is. If an influencer markets a merchant’s goods and services while marketing their personalities, that merchant better make it easy for consumers to tap to purchase. Social media influencers can make a brand. They shape the future of the social media industry, as well as the social media presence of the products and services.

Modern E-commerce is the next revolution in the American economy. Exponentially growing and innovating, e-commerce will not wait for merchants who can’t or won’t keep up. Being accessible on mobile devices is only the start for merchants. Catering to the smartphone consumer in a myriad of ways is the only path to success for the modern entrepreneur.

There are many recent advancements in merchant services and credit card processing, but one in particular that is gaining significant interest is mobile wallets. Once considered only a niche service, mobile wallets have greatly expanded and are now widely used by consumers. In fact, 24% of consumers use mobile wallets for their transactions daily. Mobile wallet transactions exceeded $4.250 billion in 2018 and are expected to reach $13.979 billion by 2022. Innovations and improvements will only continue with advancements expected in security and ease of convenience. Below are the top five mobile wallet trends that merchants, credit card processors and consumers should keep an eye on.

Mobile Banking

The first mobile wallet was created by Apple with their Apple Pay mobile wallet. Other companies came up with their own mobile wallets, like Google Pay and Samsung Pay built by competitors. Banks and other financial institutions are adjusting to cashless transactions and are creating their own digital wallets with notable names like Zelle and Venmo in the industry.

Biometrics

Biometrics have been available for many decades, but were mostly included in high security access systems. The component costs of this technology have dropped significantly making it easier for product manufacturers to include biometrics in smartphones. Fingerprint scanners and facial mapping are now available features in many of today’s phones. This technology helps provide additional layers of security to facilitate mobile wallets and seamless transactions.

Payment Terminals

NFC, or Near Field Communication allows two devices, one a POS system and a smartphone to communicate. Upon checkout, a customer will hold their phone near the terminal and the NFC chip will facilitate the transaction without revealing any card numbers. This technology has enabled greater acceptance of mobile wallets and cashless transactions.

Artificial Intelligence

While Artificial Intelligence (AI) has had little impact in mobile wallets thus far, the promise of automating and enhancing customer experience is sure to become mainstream. AI can be used for chatbots to help facilitate transactions and to interpret users’ voice commands like with Siri or Alexa. Mobile wallet providers will take advantage of AI to interact with customers in a smarter way and reduce the need for additional staff at businesses.

Blockchain and Cryptocurrency

Blockchain technology is used to let people share valuable data in a secure way that can’t be tampered with. While blockchain is the foundation of cryptocurrency, it can also be used separately to facilitate more secure transactions. Broader acceptance of blockchain will drive the enhanced security that leaves many consumers wary of using mobile payments to begin with. Numerous mobile apps already support cryptocurrencies such as Bitcoin and their inclusion into mobile wallets is nearly inevitable.

Loyalty Programs

Customers always appreciate loyalty programs and business love them for customer retention. Mobile wallets will continue to incentivize consumers for frequent purchases at their favorite restaurants, coffee shops and other retail stores. Look for this trend to definitely continue with broader acceptance of mobile wallets.

These are the top mobile wallet trends to expect over the next few years. Consumers will continue to become more technologically savvy and demand that business take mobile wallet payments.

Google Pay and Apple Pay offer a convenient and secure way to pay for goods and services with nothing more than your smartphone. But, how to find stores that accept Apple Pay and Google Pay in 2023?

If it’s been a while since you gave them much thought, you’ll be surprised to learn they are both accepted at thousands of stores from major retailers and websites to smaller businesses. If you’re looking to accept Apple Pay for your business you can get started here.

Before you leave your wallet behind, it’s a good idea to double-check that the store will actually accept one of these payment options. Here’s how to easily find stores that accept Apple Pay and Google Pay.

How to Find Stores That Accept Apple Pay And Google Pay

Using Apple Pay To use Apple Pay, you will simply need to hold your iPhone up to a wireless credit card machine at the store and use Touch ID to complete the transaction. You don’t need to launch the Wallet app or even wake up your iPhone — it will happen automatically when it’s in range of the wireless terminal – this is called contactless payments.

Apple Pay is accepted in so many places, it’s hard to maintain a complete list. You can use this payment system in boutique stores, hotels, grocery stores, retailers, many apps, and participating websites with supporting merchant services.

A sample of stores that accept the payment include:

Restaurant and fast food chains such as Jamba Juice, Jersey Mike’s, Jimmy John’s, Baskin Robbins, McDonald’s, and White Castle

Target accepts Apple Pay in the US at all locations.

Retailers like Gamestop, Disney Store, Best Buy, Kohls, Five Below, Petco, and Petsmart

Office supply retailers Staples, Office Depot, and OfficeMax accept Apple Pay

Gas stations such as Chevron, Texaco, and ExxonMobil

Major drug stores including CVS and Walgreens

Grocery stores like Publix, Meijer, Albertsons, Trader Joe’s, and Whole Foods

Costco accepts Apple Pay but only Visa and Visa Debit cards linked to the Apple Pay wallet.

Notably, Walmart still does NOT accept Apple Pay and is unlikely to accept it in the future. Major discounters such as Dollar Tree and Dollar General DO NOT accept Apple Pay. Home improvement stores Home Depot and Lowes also do not take Apple Pay as of 2021. Kroger is another notable major retailer that does not accept Apple Pay in 2021.

The Apple Pay payment system is now accepted in 21 countries and it is supported by dozens of U.S. banks, credit unions, and credit card issuers.

Finding Stores That Accept Apple Pay Unfortunately, locating stores near you that accept this payment system still isn’t straightforward. Aside from looking for the Apple icon on a drive-through or store window, there are two main options available.

The first is to open the Apple Maps app on your iPhone and search for a store. After tapping on the store’s name, you can bring up more information. The Useful to Know section usually displays the Apple icon if the store accepts the payment method.

Another option is the Pay Finders app which uses crowd-sourced data from users of the payment system and information provided by business owners. You can view nearby stores on a map or search their database.

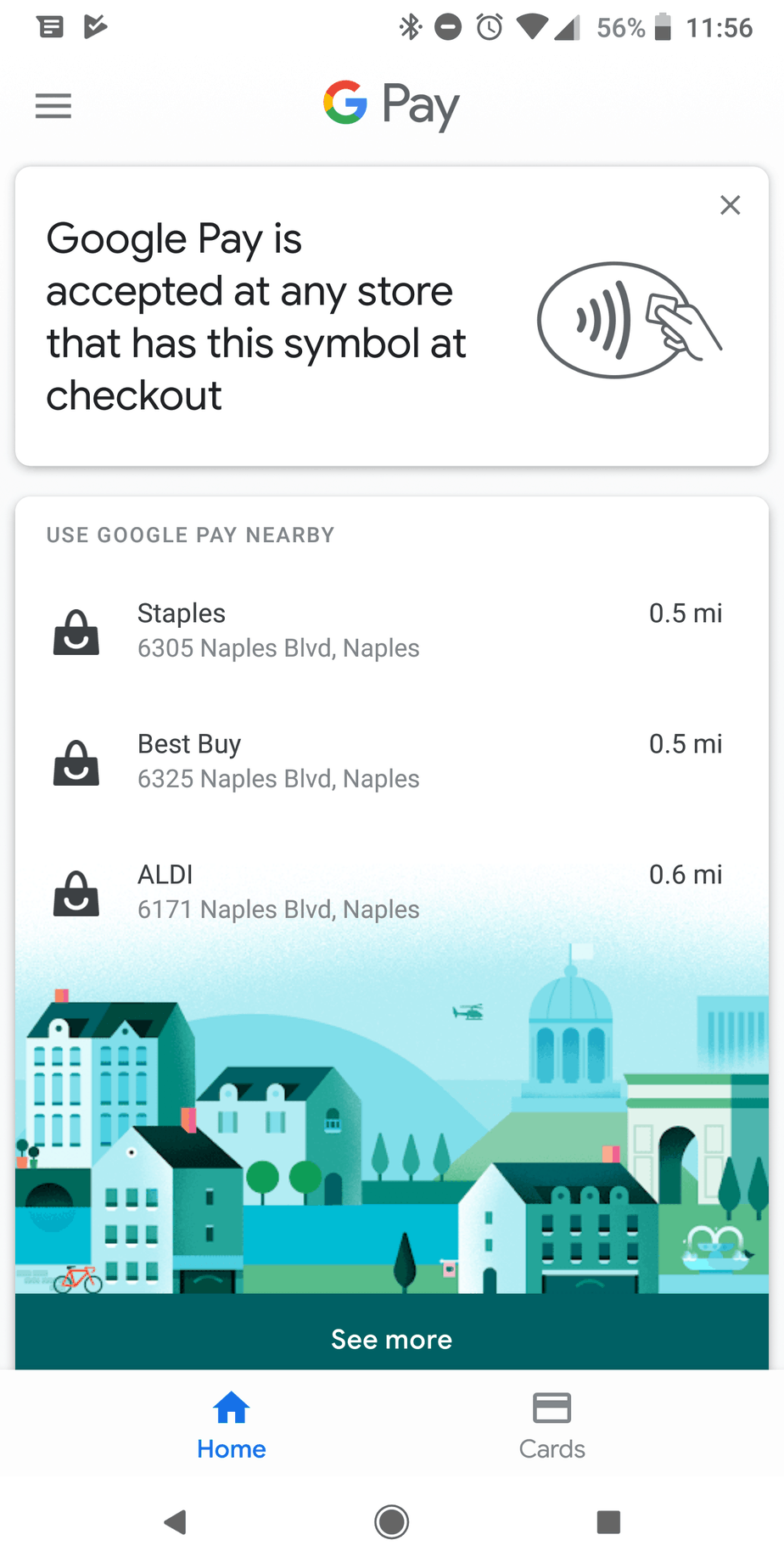

Finding Stores That Accept Google Pay Google Pay has now replaced Android Pay which a redesigned app that makes it easier than ever to find stores nearby that let you checkout with your phone. Once you have cards added to your account, you can find nearby retailers from the Home tab of the app. When you reach the list of cards, pay attention to the last two.

The second-to-last card is an informational card with the NFC payment icon that allows you to use your phone as a digital wallet when Google Pay isn’t accepted. The last card is labeled “Use Google Pay Nearby.” When you select this option, it will automatically show the three closest stores that accept the payment method. You can also choose “See More” for a longer list. The list will include everything from fast food chains and retailers to gas stations and grocery stores.

An ever-growing number of retailers are adopting NFC-compatible payment technology to improve customer convenience and credit card processing security. With greater efficiency, shorter lines, convenience, and security, mobile payments are certainly here to stay with benefits for customers and merchants alike. And it is not difficult anymore to find stores that accept Apple Pay and Google Pay.

The rationale expressed by Visa CEO Alfred Kelly as to why the company will continue to support mobile gun purchases essentially comes down to it being simply a matter of not dictating morality to the company’s customers. It is legal for people to buy guns in the United States; therefore, the company will continue to process those purchases- just as it does other things that are legal but may be considered controversial by some.

The rationale expressed by Visa CEO Alfred Kelly as to why the company will continue to support mobile gun purchases essentially comes down to it being simply a matter of not dictating morality to the company’s customers. It is legal for people to buy guns in the United States; therefore, the company will continue to process those purchases- just as it does other things that are legal but may be considered controversial by some.

Finding Stores That Accept Google Pay

Finding Stores That Accept Google Pay Pay Nearby.” When you select this option, it will automatically show the three closest stores that accept the payment method. You can also choose “See More” for a longer list. The list will include everything from fast food chains and retailers to gas stations and grocery stores.

Pay Nearby.” When you select this option, it will automatically show the three closest stores that accept the payment method. You can also choose “See More” for a longer list. The list will include everything from fast food chains and retailers to gas stations and grocery stores.