Apple Pay allows Apple iPhone 6, 6s, 6, 7, 8, 6 Plus, 6s Plus, 7 Plus, 8 Plus, SE, X, XS, XS Max, XR, 11/Pro, 12/Mini/Pro/Max, 13/Mini/Pro/Max and Apple Watches to pay for good and services with a built in NFC chip. Apple Pay has made huge leaps in acceptance in 2021 and 2022, and contactless and NFC payments are gaining traction in general. Here is a list of the retail stores, apps (both retail and transit), colleges and universities, and nonprofits currently accepting Apple Pay in 2021, 2022, and beyond:

Apple Pay allows Apple iPhone 6, 6s, 6, 7, 8, 6 Plus, 6s Plus, 7 Plus, 8 Plus, SE, X, XS, XS Max, XR, and Apple Watches to pay for good and services with a built in NFC chip. While not yet ubiquitous, Apple Pay is getting there. In the meantime, here is a list of the retail stores, apps (both retail and transit), colleges and universities, and nonprofits currently accepting Apple Pay:

You can use Apple Pay to pay for goods at the following stores with millions more:

ACE

Albertsons

Apple

Baskin Robbins

Best Buy

Chick-fil-A

Costco

Crate & Barrel

Disney Store

Duane Reade

Dunkin Donuts

Foot Locker

GAP

Crew

Jersey Mike’s

jetBlue

Levi’s

Macy’s McDonald’s

Nike

Office Depot/OfficeMax

Panera

Petsmart

Pizza Hut

Safeway

Sephora

7 Eleven

Staples

Starbucks

Subway

Target

Trader Joe’s

Walgreens

Walt Disney World

White Castle

Whole Foods

These apps and websites accept Apple Pay, along with many more:

Airbnb

B&H – photo, video, pro audio

Chipotle

Dunkin Donuts

Etsy

Fandango

Groupon

Grubhub

Hotel Tonight

Hotwire

Instacart

Jet

Lululemon

Lyft

MLB

Panera

Seamless

Sephora

Staples

Starbucks

StubHub

Target

Ticketmaster

Wish

Use Apple Pay when using these transit apps:

Caltrain San Francisco Peninsula and Santa Clara Valley

*CTA and Pace Chicago metropolitan area

MBTA Boston metropolitan area

Metrolink Los Angeles metropolitan area

MTA Metro-North and Long Island railroads New York metropolitan area

NJ TRANSIT New Jersey and New York metropolitan area

RTC Las Vegas metropolitan area

RTD Denver metropolitan area

*TriMet, C-TRAN, and Portland Streetcar Portland and Vancouver metropolitan area

Ventra (CTA, Pace, and Metra) Chicago metropolitan area

*Tap and pay via Apple Pay

The following colleges and universities accept Apple Pay:

The University of Alabama

Duke

Oklahoma University

Temple University

*Johns Hopkins University

*Santa Clara University

*Coming later this school year

Donate by way of Apple Pay to the following nonprofits, in addition to others:

American Red Cross

Children’s Miracle Network Hospitals

Chron’s & Colitis Foundation

Global Giving

RED

Jude Children’s Research Hospital

Save the Children

United Way

WNET New York Public Media

WWF

Naturally, these apps that come standard on an iPhone accept Apple Pay:

In the last update regarding the bPay mobile wallet initiative we covered the fact that Host Merchant Services is now partnered with Barclays to grow the adoption of this very innovative and versatile form of payment.

To recap…

bPay is a two pronged application that benefits both businesses and consumers. Merchants can market to consumers with compelling offers directly through the application and SMS marketing. They also have the added value to accept credit cards through a mobile wallet and contactless payment terminal.

Consumers get the convenience of a secure mobile wallet and weekly deals from local businesses. These exclusive offers are just that, exclusive. They are only offered through the bPay app and can only be redeemed by paying with the app as well. They also have the ability to load all of their credit cards into their wallet so that they have the flexibility to pay with many different accounts and not just locked into one.

Now what?

With the previous successes in Wilmington near downtown and Lower Market Street and a strong presence on Main Street and near the UD campus in Newark, Barclays is looking for the next area that is poised to grow and adopt the bPay system to engage and benefit both businesses and consumers alike. One area that both HMS and the team at Barclays believe would benefit the most is the Trolley Square neighborhood. Trolley has a dense concentration of businesses that fit the bPay mobile wallet profile.

Businesses and customers both benefit from the increased speed of bPay transactions. For the business, there is no need for the cashier to swipe a card, verify ID, print out a receipt and get a signature. Multiply this over the course of hundreds of transactions a day and the time savings is huge.

For the customer, the time savings is minimal but the focus is more around convenience. The ability to choose which card he would like to pay with by just a few taps on his smartphone and then quickly scanning the barcode. This eliminates the need to dig in his pocket to fish out his George Castanza wallet and then try and find which card to use.

The bottom line here is that mobile payments and more specifically mobile wallets like bPay clearly have added value for both consumers and business owners alike. The technology and adoption is no longer the fledgling product of just a few years ago and moving forward is only going to grow. That makes right now an ideal time for businesses and consumers to adopt the system.

For businesses in the Wilmington and Newark, DE area that are interested in getting more information please email us at admin@hostmerchantservices.com.

This week, the Official Merchant Services Blog will delve into a three-part comparison of the services offered by Host Merchant Services and Square. We will begin by giving a basic overview of both and then compare how the two companies set up a merchant account. We will then move on to a comprehensive look at the pricing and security aspects, over the next few days.

Mobile Payment Processor Square has been pushing its brand heavily this past year. The startup lets merchants process credit and debit card transactions through their mobile devices, including iPhones, Android smart phones, and even the iPad. The company picked up a lot of attention in August 2012, when it announced a partnership with Starbucks to provide mobile payment ability to 7,000 locations nationwide.

Host Merchant Services has been reporting on the Mobile Payments market for the entire time Square has been making its splash in the industry. HMS has also been marketing its own mobile payment processing solutions — giving its customers the option of accepting credit and debit card payments through iPhone, iPad and Android as well.

So how does the suite of Host Merchant Services Mobile Payment solutions stack up against Square? Today we find out in Part 1 or our three part series, Host Merchant Services vs. Square: The Merchant Account.

The Merchant Account

The first major difference between the two mobile payment processing providers is the most basic: The Merchant Account.

Square does not actually provide a merchant account to its customers. Square provides its customers with processing services, but not a traditional merchant account. Instead, Square acts more like a payment aggregator.

Typically, Merchant Aggregators or Payment Aggregators are service providers through which e-commerce merchants can process their payment transactions. Aggregators allow merchants to accept credit card and bank transfers without having to setup a merchant account with a bank or card association. The Aggregator provides the means for facilitating payment from the consumer via credit cards, stored value accounts or bank transfer to the merchant. The merchant is then paid by the Aggregator.

This is a pretty basic description for how PayPal began — and is also a really solid description for how Square works with its customer base.

Aggregation enables businesses that may be too small or risky to obtain a traditional merchant account to accept credit and debit card transactions anyway. The practice gets controversial among the more traditional sectors of the payment processing industry because it makes it harder for networks to monitor just who generates transactions and, most importantly, the attendant risk.

Some of the drawbacks of Square’s aggregation, such as caps on transaction size and delayed fund dispersal, will be reviewed in Part 2 of our series. Host Merchant Services’ traditional merchant accounts do not place caps on transactions or delay funds for any merchant.

Host Merchant Services offers a traditional merchant account to its customers. This is a noteworthy difference in practice for the merchant. The account is in the merchant’s name, giving the merchant more rights as well as more responsibilities. The traditional merchant account also holds Host Merchant Services to the merchant with added oversight on the transaction process. This is bolstered by Host Merchant Services’ customer service goals, creating a relationship where Host Merchant Services goes all-out for each merchant. The approval process through Host Merchant Services is more extensive up front, however the security and service provided gives merchants more peace of mind and more value for their effort.

In conclusion, Square and Host Merchant Services offer two very different types of merchant accounts. Although both companies allow merchants to accept credit cards, Square does not offer a true merchant account. Host Merchant Services creates a traditional merchant account, and the customer has actual control over aspects of the account. HMS directly links the merchant and their account, without any type of aggregation. This practice allows easier tracking of authorizations and transactions, a streamlined chargeback process, and less risk over all.

Today The Official Merchant Services Blog turns its tech-obsessed eyes once again to the Mobile Payment Solution sector. Recently, Host Merchant Services became fully mobile and able to offer a mobile payment solution for Android and iPhone devices. This expansion continues, and HMS now also provides a payment processing solution for iPads as well. You can read about the expanded HMS Services in our April 9, 2012 Blog Entry.

Mobile devices are ingrained in the lives of consumers these days. Like the recurring ad sarcastically states, the smartphone beta test is over. And people are wandering around everywhere with their phone bringing their social media, camera, and buying power with them.

Suri, the voice of the iPhone, is holding the hands of stars from Samuel L. Jackson to Zooey Deschanel, helping them manage such difficult life tasks as making gazpacho to putting off cleaning till the next day on one’s calendar.

Coming with this ingratiation into our daily lives are two key elements.

We’re really just one artificial intelligence glitch/accident/sabotage away from launching the type of dystopian sci-fi worldview found in Terminator, The Matrix or Magnus Robot Fighter.

We’re flying full force into a world where we’ll also start to wave our phones around like a Hogwarts Magic Wand, paying as we go from place to place, store to store.

Mobile Payments are brisk and bustling because people are buzzing to take advantage of the convenience they offer. Here’s a graphic based on data compiled by the AITE Group showing the trend in spending via smartphone in a 5-year stretch:

But it’s not all phones-n-roses. As one might expect, the state that’s home to Cyberdyne Systems and our eventual AI-overlords Skynet, has a university — the University of California — that did a study titled “Mobile Payments: Consumer Benefits and New Privacy Concerns.”

The bottom line of this study is that American consumers are still wary of what this convenient technology will bring. The study found some interesting answers to questions about consumer thoughts on their privacy.

The study found that respondents overwhelmingly oppose the revelation of contact information to merchants when making purchases with mobile payment systems and an even higher level of opposition exists to systems that track consumers’ movements through their mobile phones.

This article by Kit Eaton at Fastcompany.com dissects the numbers in the study. Eaton states that: “The numbers are stark. When asked if they thought their phones should “share information with stores when they visit and browse without making a purchase,” 96% objected to the tracking, 79% said they definitely would forbid it, and 17% said they “probably” wouldn’t allow it–meaning just 4% were indifferent or positive about the idea. When the question was instead about information sharing (phone number, address, and so on) at the actual point of sale, 81% objected to phone-number sharing–a mere 15% said they’d probably allow it and 3% definitely so. Similar figures emerged when the information shared was respondents’ home address. “

This is all well and good and you can download the study here at this link. But what the study seems to overlook is exactly how many people, many of the people most likely polled in that very study, are already well past the point of no return in terms of their privacy concerns.

Any of those who object to tracking are likely already being tracked by Google and Facebook, social media they use with ease and frequency from their smartphones.

All those who object to sharing contact information may have already shared this information easily and readily when making an online purchase in the past few years. And statistics indicate that e-commerce is booming and replacing brick and mortar in the retail sales tug-of-war.

Eaton catches on to this flaw in the study, and states in her article: “And that’s the key to unraveling this problem right there: When you do use a current-tech store loyalty card you are effectively voluntarily giving the store your personal information, and “tracking” yourself. It’s why the cards exist, of course–they’re partly there as a sales incentive, to get customers back in the door via money-off offers, but mainly so the store can collate information about customers and work out what kind of products to stock, what offers to run, and what future products to plan for.”

And Eaton even points out that in a Pew Research Survey, 71% of Americans use the internet for shopping — meaning that they’ve already typed in their personal contact information.

So essentially, Mobile Payments seem primed to take advantage of the marketplace. The worry over security is still genuine to some extent — identity theft and phasing scams and data breaches abound as we get more and more tech ingrained. But in the end, the American consumers already dove headfirst into this when they fell in love with social media. The tweets, the +1’s and the Likes have already been tracking you. So when Facebook transforms itself into Skynet, or simply when Facebook and Google go toe-to-toe with Visa in the titanic tussle for your smartphone swipes … your dollars will be as easy to find as your latest status update or check-in.

The Official Merchant Services Blog begins our second year of blogging with a look at one of our favorite topics: E-Commerce.

2011 saw huge gains for online shopping. As reported in The Official Merchant Services Blogon Cyber Monday, online shopping was strong on Black Friday. IBM research unit Coremetrics stated that 20% more consumers shopped online Black Friday 2011 than did in 2010. The data collected also states that 39% more online shopping happened on Thanksgiving Day 2011. The ease of online shopping is infiltrating the traditional brick-and-mortar retail event and Host Merchant Services‘ analysis of it held true –– sales numbers across the board rose from 2010, so overall Black Friday had a boost for retail, but clicks from e-commerce continue to grow and cut into the sales from bricks.

Also, mobile payments saw a huge increase during the holiday shopping season. According to this article from Seeking Alpha, mobile payments business increased 500% from 2010 on Black Friday. According to the article, PayPal mobile reported the huge increase, coming in at 511% to be exact. PayPal Mobile also noted that there was a 350% increase in mobile shopping on Thanksgiving 2011 when compared to 2010.

The Numbers Keep Coming In

This article by Internet Retailer demonstrates that Black Friday was just the beginning. There were more than 3,000 transactions totaling $141.6 billion in 2011 in the marketing, media, technology and service industries according to data collected by investment banking firm Petsky Prunier LLC. Of those transactions the E-Commerce and digital media segment was the most active, with 1,159 deals valued at more than $44 billion.

All of this activity demonstrates strength in the E-Commerce industry, and suggests that 2012 is a year primed for continued growth and success — which combines with the already rampant predictions of success for Mobile Payments within the E-Commerce industry.

Comparing the recent success to the success of internet companies in 2000 and 2001, the article tries to figure out if the bubble will burst like it did back then for tech companies. The author’s opinion is that the similarities are only on the surface, and that the two situations are vastly different — suggesting that in the end, it’s not a bubble that is going to burst but rather an industry that is going to grow and evolve. The article looks specifically at the E-Commerce sector in India, but does spend time detailing the big picture globally.

Online Shopping is Now Commonplace

To really underscore the potential growth that E-Commerce has in 2012, this article from Daily Deal Media talks about how popular online shopping is becoming with moms. The article cites a BabyCenter survey which suggests that: “71% of moms regularly turn to websites such as shopping engines and review sites to compare prices. Another 56% admit to searching for coupons or digital discount opportunities on a regular basis.”

This is a compelling point in regards to the overall picture of E-Commerce. It has become more and more commonplace in everyday life for shoppers around the world. Mothers are turning to it for the convenience of being able to get shopping done quickly and efficiently, according to the article. And it is just become an ingrained part of our economy, fueling the potential for further growth.

Mobile Payments Big Problem

The potential growth for Mobile Payments is huge. But the one thing holding it back in the U.S. is security. Just as online shopping has become more and more commonplace, people have gotten comfortable with making payments online. That brings risk, as phishing scams and credit card fraud has increased. But security standards like the PCI DSS have helped to make the mainstream comfortable with clicking the pay button and giving out their payment information.

Mobile Payments, however, are not quite there yet in terms of acceptance. This article from the Chicago Tribune discusses the looming security issues that the mobile payments market faces. As the article states: “While the first mobile virus dates back to June 2004, risks from hackers remained limited because of the relatively small size of the market. But this has changed with the surge in the smartphone segment, which this year outgrew the PC market, and the new dominance of Google’s Android software. The emergence of mobile payments, which allows shoppers to swipe their phones at a cash register, is whetting the interest of hackers and data thieves.”

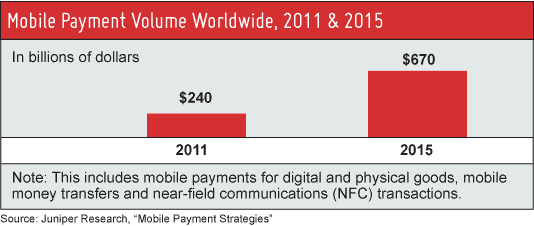

The article states that fewer than 5% of smartphone users have security software installed on their device, according to Juniper Research — the same Juniper Research that predicts Mobile Payments will increase to a $670 billion industry by 2015. And a study by Deloitte cited in the article suggests that for companies in the technology, media and telecom sector expect data stored on staff mobile devices to be their biggest security headache in 2012.

Essentially that’s the biggest obstacle holding back the Mobile Payments industry. The sheer convenience the technology brings to the payment industry is extremely powerful and so despite security concerns it continues to be developed and pushed. 2012 will see growth in the industry, despite the security issues. And as consumers get more and more familiar and comfortable with the phone swipe style of payment, the industry will boom.

A List for 2011

And just for fun, here’s a list from Mashable.com detailing who they think were the biggest winners and losers from 2011 in E-Commerce.

Their winners include: Amazon, Apple, Wal-Mart and Gilt Groupe.

Their losers include: Barnes and Noble, HP, Netflix and Sony.

The Official Merchant Services Blog continues its ongoing coverage of the upcoming holiday shopping season and how it will impact the thriving E-Commerce industry. Yesterday’s blog took a look at some of the statistics revolving around 2010’s holiday shopping profits as well as detailing a trend among online shoppers to begin their holiday shopping in the summer months. We also promised that today’s blog would show how gift cards and gift certificates were being taken a step forward.

Mobile Gift Cards

Gift Cards are going digital this year, with the onslaught of a variety of providers who will give people purchasing power of gift cards sent directly to their mobile phones. This Fox News story touts mobile gift cards as the “cool” and “sophisticated” new gift giving idea. The article cites the success of coffee giant Starbucks this year with Mobile Gift Cards, and suggests that others are following that blueprint. Starbucks had some compelling numbers to underscore the success of their mobile gift card program according to the article:

“”Within nine weeks of the national launch of mobile payment, customers paid more than 3 million times using our mobile payment application in stores and this number continues to grow at a steady rate,” says Adam Brotman, senior vice president of digital ventures for Starbucks Coffee Co.”

A mobilesyrup article features the Mobile Gift Card for apps from Toronto-based Mobiroo. And a San Francisco Chronicle article looks at Giftly and its Mobile Gift Card product. It’s a new trend that looks to make a big splash in the 2011 holiday season.

How Do They Work?

The standard way Mobile Gift Cards are designed to work is: The card is sent via email, Facebook or text. The recipient is notified that he or she has a Gift Card, and can take their smartphone into the store and use it immediately. The store clerk simply scans a bar code from the recipient’s phone, and the card is applied to the balance.

Unfortunately, as has been pointed out by Host Merchant Services in previous posts about Mobile Payments not quite taking hold in the U.S., this standard process doesn’t always work out. Many retailers are not physically equipped to handle such a process. So if the bar code can’t be scanned, Mobile Gift Cards can still be used by consumers if they print out the coupon prior to going shopping, or if they input the gift card number at a website or point-of-sale terminal.

The obvious convenience of Mobile Gift Cards is that they work seamlessly with e-commerce and online shopping. You get a coupon code on your mobile device, and then can input that number at the website where you are shopping.

Follow the Leader

The Fox News article noted that Applebee’s, California Pizza Kitchen and Target all offered Mobile Gift Card options this year. The mobilesyrup article about Mobiroo cited the old school hook of the idea, stating that “Gift cards are a symbol of a bygone time when analog ruled and retailers yielded more to foot traffic than mouse clicks. But according to Mobiroo CEO Vinay Chopra, old is new again.”

Mobiroo, according to Chopra, sees Mobile Gift Cards having quite a lot of potential in the marketplace because of smartphones themselves, specifically the apps people use and purchase for their phones. But Mobiroo is still using a physical Gift Card, with a scratch-off area that gives a code to redeem for use in an App store, and Chopra sees this as a stocking stuffer item for the holiday shopping season.

Giftly, on the other hand, is following the example set by Starbucks and others, and makes a completely digital process available. According to the San Francisco Chronicle article: “When a Giftly card is purchased, the buyer’s credit card is charged. When the recipient opens the card on their mobile phone in the store, Giftly check their location. Once Giftly confirms that the recipient is at the right venue, the gift money is unlocked. Giftly then send the money as a credit card reimbursement to the recipient. The recipient then purchases the product at the cash register per usual. The merchant doesn’t have to be told about the Giftly — the service is completely a location-based redemption. Unlike most gift cards, Giftly allows the buyer to select up to three venues where the recipient can spend the money.”

All Giftly cards are delivered via e-mail and redeemed on a mobile phone. They allow you to send gifts unbound by location. It adds convenience to the shopping process, which is a core element that is going to make it popular with consumers. By allowing consumers to digitally forward purchasing power to friends and family wherever they happen to be, the shopping process gets that much faster and easier, making mobile gift cards an attractive option for holiday shoppers.

Tomorrow we’ll touch on a topic brought up by this blog, taking a closer look at apps as gifts in the upcoming holiday season.

{kind=link}