The Wall Street Journal, citing a document they obtained on September 20, revealed Bank of America has plans to cut 16,000 jobs by the end of the year.

This move is not exactly surprising news since the company had already discussed plans to shave 30,000 jobs in a plan to trim jobs and cut costs by the end of 2013. The move, however, does accelerate the earlier plan from cost cutting that would take more than a year — and eliminate annual expenses by $5 billion — to cost cutting that will happen right now. The overall plan of cutting 30,000 jobs is designed to help the company offset unprofitable moves such as the 2008 takeover of Countrywide Financial Corp.

In fact, Forbes, in this article reporting the news of the job cuts, characterizes the mortgage section of the bank as something that “has hamstrung the bank” citing specifically the acquisition of Countrywide. The article notes that 3,200 of the job cuts could come from the division overseeing new mortgages.

Overall, these proposed cuts will bring Bank of America’s workforce down to 260,000 overall employees by year’s end — a number that drops the bank from being the biggest employer in the U.S. banking industry. After this round of cuts hits the company’s bottom line, Bank of America would fall behind Wells Fargo and JP Morgan Chase.

The Official Merchant Services Blog is citing these cuts because beyond the issues brought up with Bank of America’s acquisition of Countrywide, one of the other key factors in the bank losing profits was the Durbin Amendment. Back on October 13, 2011 we reported Bank of America felt a huge national backlash based on its reaction to the Durbin Amendment. The bank decided to offset losses it would incur from the legislation’s hardcap on debit swipe fees — losses which Forbes reported in March 2012 to be $441 million in Q4 of 2011 when compared to Q4 2010 — by initiating a $5 monthly transaction fee for using their debit cards.

This type of move was predicted by Host Merchant Services in its Durbin Amendment analysis, and was embraced by a host of large, debit card focused banks, besides just Bank of America. JP Morgan Chase, Sun Trust, Regions Financial Corp., and Wells Fargo all had plans to charge a similar fee. But consumer backslash was intense, media scrutiny was focused, and Bank of American in particular felt the brunt of the Occupy Wall Street movement at the time. So the banks all backed off of the idea to implement these added fees.

The hardcap being what it is, however, left Bank of America with the continued problem: Losses.

So as part of a combination of bad moves, Durbin included, the bank is faced with the decision that to stay profitable they have to cut jobs. Some analysts, such as Anthony Polini, for the investment firm Raymond James, feel these belt-tightening measures are evidence of an agile and healthy company. “The company is doing great,” the analyst said in this article, “It’s another phase of expense control.”

The bank’s stock price took a hit based on the news as shares closed down 0.82 percent to $9.11 on Friday.

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. We want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: we deliver personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access.

Today we will take another look at international processing, and the fees associated with accepting an international card. Yesterday we defined the MasterCard Cross Border Fee, and today we will explain the Visa International Service Assessment.

Visa implemented an international service assessment (ISA) fee of 40 basis points (0.40%) in April of 2008. This fee applies to all transactions involving a U.S. based business and a credit or debit card issued outside of the U.S. The ISA is also separate from interchange rates and from Visa’s standard assessment fee, which is currently 11 basis points (0.11%).

For example, the ISA fee of 0.40% will be added to a transaction where a customer uses a Visa-branded card issued out of the United States to buy something here in Delaware.

The ISA is one of two fees Visa currently charges for international card usage, the other is the International Acquirer Fee, a separate 45 basis point fee (0.45%), which applies under the exact same circumstances as the ISA. Visa began charging the IAF in October 2009.

The total fees Visa charges for a transaction involving an international card processed in the U.S. is the sum of the ISA fee (0.40%), the Visa standard assessment (0.11%), and the International Acquirer Fee (0.45%), which comes to almost a full percent above interchange, 96 basis points (0.96%).

Today The Official Merchant Services Blog gets extra visual with a step by step breakdown of how Credit Card Processing works.

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. We want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today we build off of our previous knowledge base entry on just credit cards. We noticed that we’ve been adding to this database for months now and kind of skipped over some of the most basic elements of the industry. So now that we’ve defined credit cards, we want to take you on a journey through credit card processing, detailing exactly how it happens.

CREDIT CARD PROCESSING

Host Merchant Services is able to guarantee its customers savings and the lowest rates possible. By understanding how credit card processing works, where the money gets made off of the transactions themselves and where those hidden fees actually are, you can gain some valuable insight into how Host Merchant Services is able to make its guarantee. Here’s a step-by-step breakdown that sheds light on where the fees from each transaction come from:

How Does Credit Card Processing Work?

The way credit card processing companies make money for themselves can sometimes be a confusing labyrinth where fees are hidden, percentages are tied to things not listed on statements and the deal you think you are getting isn’t the best deal you can actually get. Host Merchant Services is dedicated to giving its merchants the lowest price guaranteed, and the company strives to maintain transparency with no hidden fees. So take a walk with us and see behind the curtain as you learn exactly where the money is being made when you swipe a customer’s credit card.

Step One: A customer visits a store.

Step Two: Customer purchases $10 worth of merchandise.

Step Three: The customer swipes his credit card through a payment processing terminal such as a Hypercom T4205 from Equinox Payments to pay for the merchandise.

Step Four: The card reader recognizes who the customer is and contacts the bank that issued the credit card.

Step Five: The customer’s bank sends $10 to the merchant’s bank.

Step Six: Then the merchant’s bank deposits $9.80 to the merchant’s bank account.

Step Seven: That remaining 20 cents, a 2% fee, is taken from the $10 and given to the customer’s bank.

Step Eight: The customer’s bank then splits the 20 cents with the credit card company.*

* Depending on the specific company, country and merchant, the percentage can range from 1% to 6%. The amount the bank gets and the amount Visa gets is a negotiated deal. Also, Visa and MasterCard charge the banks an annual fee to be a part of their network in the first place.

Where The Money Gets Made

Credit Card Companies make money in a variety of ways. Here are the four most common:

One: The most common way credit card companies make money is through fees, such as the annual fee, overlimit fee and past due fees.

Two: Another way credit card companies make money is through interest on revolving loans if the card balance is not paid in full each month.

Three: As explained above, the card issuer (the bank that issued the card and/or the issuer network, be it Visa, MasterCard, Discover) makes a percentage of each item you purchase from a merchant who accepts your credit card. The rates range from 1% to 6% for each purchase.

Four: The card issuer can also make money through ancillary avenues, such as selling your name to a mailing list or selling advertisements along with your monthly billing statement.

SOURCE: Information for this article was gathered from www.creditscore.net, the movie Superman III, Wikipedia and Authorize.net.

Welcome to The Official Merchant Services Blog’sKnowledge Base effort. We want to bring clarity to the payment processing industry’s terms and buzzwords. We want to remove any and all confusion merchants might have about the industry. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today we decided to get as basic as possible. Our term is credit card. No, really, credit card. We noticed that we’ve been adding to this database for months now and kind of skipped over the most basic element of the industry.

Credit card processing hinges on the use of credit cards. So, without further hullabaloo:

Credit Card

A credit card is a payment card issued to users as a system of payment. It allows the cardholder to pay for goods and services based on the holder’s promise to pay for them. The issuer of the card creates a revolving account and grants a line of credit to the consumer (or the user) from which the user can borrow money for payment to a merchant or as a cash advance to the user.

Credit cards are issued by a credit card issuer, such as a bank or credit union, after an account has been approved by the credit provider, after which cardholders can use it to make purchases at merchants accepting that card. Merchants often advertise which cards they accept by displaying acceptance marks – generally on stickers depicting the various logos for credit card companies like Visa, MasterCard and Discover. Sometimes the merchant may skip the display and just communicate directly with the consumer,saying things like “We take Discover” or “We don’t take credit cards”.

When a purchase is made, the credit card user agrees to pay the card issuer. The cardholder indicates consent to pay by signing a receipt with a record of the card details and indicating the amount to be paid or by entering apersonal identification number (PIN). Also, many merchants now accept verbal authorizations via telephone and electronic authorization using the Internet, known as a card not present transaction (CNP).

Electronic verification systems allow merchants to verify in a few seconds that the card is valid and the credit card customer has sufficient credit to cover the purchase, allowing the verification to happen at time of purchase. The verification is performed using a credit card payment terminal or point-of-sale (POS) system with a communications link to the merchant’s acquiring bank. Data from the card is obtained from a magnetic stripe or chip on the card; the latter system is implemented as an EMV card. For card not present transactions where the card is not shown (e.g., e-commerce, mail order, and telephone sales), merchants additionally verify that the customer is in physical possession of the card and is the authorized user by asking for information such as the security code printed on the back of the card.

Each month, the credit card user is sent a statement indicating the purchases undertaken with the card, any outstanding fees, and the total amount owed. After receiving the statement, the cardholder may dispute any charges that he or she thinks are incorrect. The cardholder must pay a defined minimum portion of the amount owed by a due date, or may choose to pay a higher amount up to the entire amount owed which may be greater than the amount billed. The credit issuer charges interest on the unpaid balance if the billed amount is not paid in full (typically at a much higher rate than most other forms of debt). In addition, if the credit card user fails to make at least the minimum payment by the due date, the issuer may impose penalties on the user.

Merchants

For merchants, a credit card transaction is often more secure than other forms of payment, because the issuing bank commits to pay the merchant the moment the transaction is authorized, regardless of whether the consumer defaults on the credit card payment. In most cases, cards are even more secure than cash, because they discourage theft by the merchant’s employees and reduce the amount of cash on the premises. Finally, credit cards reduce the back office expense of processing checks/cash and transporting them to the bank.

For each purchase, the bank charges the merchant a commission (discount fee) for this service and there may be a certain delay before the agreed payment is received by the merchant. The commission is often a percentage of the transaction amount, plus a fixed fee (interchange rate). In addition, a merchant may be penalized or have their ability to receive payment using that credit card restricted if there are too many cancellations or reversals of charges as a result of disputes. Some small merchants require credit purchases to have a minimum amount to compensate for the transaction costs.

Costs to merchants

Merchants are charged several fees for accepting credit cards. The merchant is usually charged a commission of around 1 to 3 percent of the value of each transaction paid for by credit card. The merchant may also pay a variable charge, called an interchange rate, for each transaction.

Merchants must also satisfy data security compliance standards which are highly technical and complicated. In many cases, there is a delay of several days before funds are deposited into a merchant’s bank account. Because credit card fee structures are very complicated, smaller merchants are at a disadvantage to analyze and predict fees.

Finally, merchants assume the risk of chargebacks by consumers.

I’m back to once again speak about Mobile Payments and their presence in Delaware. In case you missed my last blog, it’s here. It’s really finally here. Barclaycard Mobile Wallet is an active program that participating merchants at the waterfront in Wilmington, DE, and along Main Street in Newark, are using. Right now you can use your phone to buy stuff!

So that’s exactly what I did. I set out to visit some shops and buy some stuff. To give this test run some authenticity, I decided to try and buy things I actually needed. Let’s see how the process works and how useful it is for real-time shopping!

But first, I needed to update my settings. After downloading the application, and adding a credit card to my account, I had noticed I wasn’t seeing any offers. Kara from Barclaycard saw my blog and reached out to help me.

So I needed to add another step in our process for getting the technology up and running. It may seem like a bit much at first, but trust me, it’s fast and easy to initialize.

Kara noted that I needed to add locations to my account to get the offers to show up. ZIP codes are the easiest way to do that. Wilmington’s ZIP is 19801, and Newark’s is 19711.

The Revised Set of Steps

So now, our updated steps to bring the power of mobile purchases right to your hot hands look like this:

Step 1: Visit this site and register for an account. This is key. You can’t just download the app and go. You need to register online first. Since you’re here online reading this blog, you can take a moment to click that link and get that out of the way.

Step 2: You go through the process of setting up an account. Choose a username, password, give your information.

Step 3: You add the card you want the wallet to charge.

Step 4: You can then download the app from the app store or google play store.

Step 5: Activate the app on your phone, and go through the log in process. You’ll be asked for your passcode, and to log in with your username and password, and even one of the additional security questions.

Step 6: Go to settings — the gear icon — and go to offer locations. Add locations. Use the ZIP code that works best for you (I used both). Then you go to …

Step 7: BOOM! Start buying stuff!

The Buying Stuff Part

Thanks to Kara’s timely advice, I had offers streaming through my phone immediately. Armed with mobile purchasing power and enthusiastic curiosity, I leapt from my centralized blogging and news update headquarters — taking this story live and direct to the macadam of Main Street Newark.

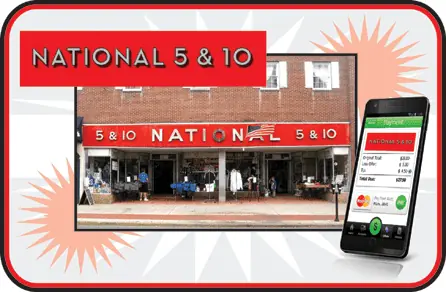

My first target was National 5 and 10, located on 66 E. Main Street. Boasting the world’s largest selection and lowest prices for University of Delaware merchandise, I decided to zero in on … art supplies. I needed a sketch book and a new pencil and eraser set to continue to design and draw projects like this more than I needed a new Blue Hens ball cap.

So I went to work racking up an impressive spree of supplies:

Mechanical Pencil with lead refills, 0.5 mm fine point lead size. For the nitty gritty line work.

Hi-Polymer Pentel white plastic art eraser. Because they take the pencil marks away but leave the ink behind.

5.5 x 8.5″ sketchbook, to help me rough out all my creative ideas.

And to get my purchase up over $10, four 5 x 9″ bubble mailer envelopes, so I can send slick prints of my best portfolio pieces to people interested.

Total: $11.24

I took this stash of artistic loot to the one counter that was open. When it was my turn I happily stepped up and asked if I could purchase these with the Barclaycard app, and flashed my phone at the cashier. This caused quite a stir, as it seems I was the very first customer to utilize this technology. Excitement buzzed in the air. We moved this transaction over to the other side of the area where the Barclaycard Mobile Wallet Terminal was kept. Another cashier took over the transaction, but a crowd began to form. The owner came over to see this landmark purchase of a pencil, eraser, sketchbook and some envelopes take place. Customers took notice. And then it happened.

The cashier rang up the items. I had my phone out and the app open. I was prompted to scan the QR Code on the terminal. The app took over and in a flash my payment was recorded. I approved it with the click of a button. The cashier printed out my receipt and just like that it was over. Payment made. Stuff bought. Once the wow factor wears off, the process will turn out to be very easy. As fast as swiping a credit card, with none of the hassle of keeping a card on you in your wallet. Mobile wallet finally lives up to the hype. I take my phone everywhere, as do most people. I need it for emergencies — but also to keep up with work and friends while on the go. So tucking this payment power into it just consolidates everything, making shopping a seamless part of the package.

But Wait, There’s More

I made the effort to obtain a purchase of $10 or more to take advantage of the offer I saw on my screen. But it didn’t seem to take. Later in the day I found out the offer might not be live yet. So I moved on to my next stop: Switch Skateboarding, located on 54 E. Main Street. No worries here about finding an item over $10 in price, but there were no visible offers for Switch anyways, so I put that out of my mind and focused on finding something I actually needed — wrist guards.

I haven’t been on a skateboard since I was 15 years old. But I’ve needed items that Switch sells almost regularly for the past four years because I’m a roller derby referee. I picked up a pair of Destroyer wrist guards. I chose them primarily because I already have a pair of 187 wrist guards and an old pair of pro-tec, so wanted to see if these fit any more comfortably. They cost $17.

Once again I stepped up to the counter and announced my intention to purchase this item with the Barclaycard app. There was decidedly less of a fuss about it as the staff at Switch seemed to be both more chilled out in general and ready to handle the unusual request. However, just like at National 5 and 10, there was a swapping of cashiers in terms of who handled the transaction. Switch uses a different setup than 5 and 10. The skateboard shop is working a completely virtual system, running transactions through a computer. The payment seemed even more seamless than at 5 and 10. All that was involved was opening up their gateway in their browser, inputting the details of the transaction, scanning the item’s barcode and then it was up to me. Switch has a static, standing QR Code on a card atop its counter. I had my app open and ready. When prompted I clicked the button and my phone scanned the barcode. Once again it was lightning fast. And after clicking my approval of the sale, the transaction ended.

Success. I was now armed with a fully operational mobile payment telephone, a pair of brand new wrist guards and some art supplies that I needed. This took the idea of buying things with a wave of my phone from concept to cold, hard reality. I found myself wanting to do this everywhere.

The Only Downside

As far as I was concerned I came away from this excursion with only one negative — there just wasn’t enough visible presence to let consumers know this existed. At 5 and 10, I created a crowd, but I knew going into the store I could buy things this way. The terminal itself stands out as it is different from other terminals. But I wonder if it’s all that visible since it’s not exactly a place where consumers actually look. I’m reminded of the time I spend standing in line at places like Wawa or 7-11, where I’d really like to just swipe my phone and go. I don’t even look at the terminal until I have to. How do you let people know they can do this now? Do you start to ask them, “Credit, Debit or Mobile?”

Or do you just get the word out there with more and more buzz, like this blog or a demonstration in the store at key high traffic times? Do I just keep telling my friends, “Hey, check out what I can do?”

It’s probably a mixture of all of those ideas. The technology is now here. It works. And it’s very easy to use. The ball is rolling. It just needs to pick up speed and add more snowy mass as it rolls along.

The Official Merchant Services Blog again looks into the mobile wallet world today, by introducing the new product from Visa, Inc. called V.me. Last week we discussed in detail the BarclayCard mobile wallet system, which has come here to Delaware at participating locations in Newark and Wilmington.

Visa plans to roll out its own version of a mobile wallet solution by the end of this year. Although the Card Issuer is the largest in the world, the entrance seems late in a game filled with tough competitors. Visa has been testing a beta of the program with five large online retailers. Buy.com, Bidz.com, Cooking.com, Modnique and PacSun are the retailers currently offering the e-commerce side of the service on their web sites. Customers have the option when checking out to sign up for the program, set up the account and add a card, all without leaving that merchant’s site. Buy.com went live with V.me first in May; the others followed suit a few months after.

The program will eventually allow mobile device users to pay for goods from participating merchants at physical locations, most likely by the end of 2012. V.me uses a ‘hybrid’ security system of the device’s secure element, as well as cloud servers to store customers’ card credentials. This technique is reportedly more secure than the Isis system of storing card information directly on a device’s SIM card. In August, Google decided to upgrade to a cloud based system of storing card data, however they kept reliance on the phone-based element to house a prepaid virtual card that initiates transactions and identifies users.

Visa will also include a location-based offers service with V.me, that will likely use geo-tagging to identify customers most visited locations, and market offers accordingly. Competitor Google Wallet, while nearly a year old, has struggled due to the reliance on NFC-based technology that is not wide spread enough yet. Other companies such as Apple Inc., and MasterCard have also announced their entrance into the mobile payment game. Apple, with its Passbook wallet feature expected in the new iOS 6 will feature QR code reading technology. MasterCard announced a mobile wallet program in May, called PayPass wallet service that claims to be open to third parties for development and flexible to a wide variety of payment brands.

In summary, Visa’s V.me is one of the mobile wallets that I’ll be eagerly waiting for, however it seems a long way off from implementation now. For Delawareans, Barclays’ Barclay Card Mobile Wallet app seems to be the only one to hit the ground running here in the First State. A watchful eye will be kept on this close race of Banks, Card Issuers and Credit Card Processors to see who will be the one to win Mobile Wallet Dominance.

Barclaycard Mobile Wallet is an active program that participating merchants at the waterfront in Wilmington, DE, and along Main Street in Newark, are using. Right now you can use your phone to buy stuff!

For Me, This is Big

Normally I try to maintain some composure and tact when scribing The Official Merchant Services Blog but I’m a little too excited to keep calm. Mobile Payment Processing– as I noted in my last blog entry about how long it was taking Near Field Communication to get here — is a topic I’ve been fascinated with my entire time working in this industry. And I’ve reported how each new take on the technology has been inching forward, how the pieces are in place for X, Y or Z to finally break through and for U.S. consumers to be able to start waving their phones around like lightsabers, cha-chinging their way through purchases.

Got the Ball Rollin’

For the most part it’s been tiny test markets using the things that are active — test markets nowhere near me or my shopping stomping grounds. And then there’s been other technology riddled with delays. And then there’s been discussions about security issues. It just seemed like this crazy new purchasing power was not going to come to a store near me anytime soon. The Magic 8-Ball Blog I wrote back on October 18, 2011 seemed to have encapsulated the entire issue.

Me: When will Mobile Payments get here?

Magic 8-Ball: Ask Again Later.

And even just the other day I was stuck in the same morass of Mobile Payments taking too long to get going, as I reviewed the status of NFC and looked at Isis getting ready to finally hit test markets — in Utah and Texas.

Then I found out about Barclaycard and their Mobile Wallet. It’s here. It’s live. It’s working in the areas where I shop.

So Let’s Get Started

All I had to do was sign up and start trying this technology out. This blog is as close as I will probably get to real-time reporting on the Credit Card Processing Industry. I’m going through the steps to acquire this purchasing power right now. Here’s what I’m doing:

Step 1: Visit this site and register for an account. This is key. You can’t just download the app and go. You need to register online first. Since you’re here online reading this blog, you can take a moment to click that link and get that out of the way.

Step 2: You go through the process of setting up an account. Choose a username, password, give your information.

Step 3: You add the card you want the wallet to charge.

Step 4: You can then download the app from the app store or google play store.

Step 5: Activate the app on your phone, and go through the log in process. You’ll be asked for your passcode, and to log in with your username and password, and even one of the additional security questions. But then you go to …

Step 6: BOOM! Start buying stuff!

Now Where do I go to Buy Stuff?

I now wanted to witness the firepower of this fully armed and operational battle station … I mean Mobile Wallet. Here’s a list of participating merchants:

Newark

SAS Cupcakes

MainStream Nutrition

Switch Skateboarding

National 5 and 10

Caffe Gelato

Coming Soon to Newark:

Gecko Fashions*

Over Easy*

Moxie Boutique*

Cosi*

Wilmington:

Al’s Sporting Goods

Harry’s Fish Market & Grill

Dryrock Café

Veritas

FireStone

eeffoc’s

Water Street Deli

Olde World Cheese Steak Factory

Cosi

Bella Vista Pizzeria

Zaikka Indian Grill

Riverfront Produce

Harry’s Seafood

Extreme Pizza

But Wait, There’s More!

This is more than just a way to buy things with your phone instead of your wallet. This program is a combination of sales promotion and mobile payment power. Now that I’m signed up and active, I will be able to pay with mobile and receive special offers from local merchants. That’s the added value — merchants who participate in this mobile wallet community will be able to offer me deals and specials. Think of it like this: It’s a mobile wallet with a built in groupon. It’s merging the best aspects of QR-Code technology and consumer convenience.

The app functions off of the QR-Code technology that we’ve discussed multiple times in the past. This technology was already ahead of other options as it had been harnessed for marketing purposes in the previous few years. In fact, it’s the one mobile payment option I’ve already had the good fortune of experiencing back in May through Fandango. These mobile payment solutions are generally pretty straightforward. They usually consist of an application on a merchant’s device that allows them to scan a barcode, or a QR Code. The QR Code scanning is becoming extremely popular, giving companies the ability to run marketing promotions as well as purchases through the use of the QR Code and its ability to capture information. Fandango’s Mobile Ticket program allows you to purchase your movie ticket through their application and then just scan the QR Code they send to your device when you arrive at the theater. This program has been gaining increased success and popularity this summer, and as we reported, set record highs for the company with the release of the blockbuster Avengers Movie.

What Barclaycard is doing is in-line with this description. You will use QR Codes to make purchases with your phone. But the app also seamlessly fuses the marketing power into the experience. As a Barclaycard Mobile Wallet user, I have access to exclusive offers available and redeemable only through the wallet. Offers will update at least once a week. I currently have no offers, but I just signed up 10 minutes ago so I will have to check back.

When I first started writing for this website, and The Official Merchant Services Blog, a topic I was both fascinated with and completely astounded by was Near Field Communication (NFC). It seems fitting that on the eve of the National Football League’s 2012-2013 season debut — a rare Wedensday Night Football game — which features a gridiron battle between the Dallas Cowboys and New York Giants, two mainstays of the National Football Conference (NFC), that I would once again be tackling the topic of NFC. The first time I saw the acronym I thought it was talking about football.

It wasn’t.

It was talking about technology that was poised to revolutionize payment processing and make everyone’s phone their wallet. We were going to be radically transformed from a cashless society relying on plastic cards with magnetic stripes into a cashless society relying on waving around your smartphone at registers and terminals who pick up your signal and magically charge your account. One swipe of the phone, and no hassle whatsoever, as Near Field Communication did all of the talking back and forth between devices while you figured out what you were going to buy next.

But over the past couple of years, the dominance of NFC has pretty much mirrored the Dallas Cowboys own dominance of the NFC in which they play. A lot of hype, but not a lot of tangible financial results. The biggest proponent of NFC has been Google Wallet, but another giant of the NFC industry-in-waiting has been Isis. Just like the NFL season, Isis — the mobile-payment joint venture backed by AT&T Inc., Verizon Wireless and T-Mobile USA Inc. — is poised to get underway in September too.

VeriFone Systems Inc., a maker of payment terminals that Host Merchant Services offers for free to qualifying merchants that sign up with them, is working on the Isis project. Chief Executive Officer Doug Bergeron said in an interview with Bloomberg that VeriFone is preparing to introduce Isis in Salt Lake City and Austin, Texas.

Isis had initially planned to roll out its NFC-based mobile payment service in the first half of 2012. The joint venture tweaked its strategy last year, opting to use credit-card companies to handle transactions rather than the carriers themselves. This shift has taken time to implement because its been focused on ensuring payments can be made securely — the single biggest fear that consumers have voiced about mobile payments.

Are You Ready for some Mobile?

So now that Isis is on the cusp of kicking off NFC-fueled mobile payments in select areas, is this validation for the technology? It doesn’t seem that way. Google Wallet’s NFC-integration still hasn’t come to my local shopping areas. But many other mobile payment options have. I can and have bought movie tickets on my phone. This was done using the QR-Code technology which seems to have had a quicker integration into the U.S. Economy at large. It was something that many companies were already using for their marketing so utilizing the technology to work for payments was faster as it relied on infrastructure already in place, and consumer fears of security were lower since consumers had already opted in with the codes.

Toss Square’s partnership with Starbucks and PayPal’s partnership with Discover into the mix and it seems like the Mobile Payments industry has decided it wants to score an industry-wide touchdown with or without the help of NFC. In fact, Devindra Hardaware suggests in a column for VentureBeat that the industry could still make use of the ideas in NFC, but completely bypass the ground game entirely by going with an aerial assault guaranteed to score big with consumers: “There’s still plenty of room for mobile wallets to disrupt the way we pay — just look at the Pay with Square with app, which lets merchants charge you just based on your name and face. In many cases, you won’t even need to pull your phone out of your pocket.”

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is Network Access and Brand Usage (NABU) Fee. We chose this today because of all of the recent changes to Interchange fees released by the major credit card companies.

Network Access and Brand Usage Fee

The Network Access and Brand Usage (NABU) fee was created by MasterCard in 2009, and is fee imposed by MasterCard for all U.S. issued card transactions settled with MasterCard by a U.S. merchant. Effective January 8, 2012 MasterCard’s NABU fee was applied to authorization transactions instead of settlement transactions. MasterCard charges $0.0185 on all settle or refunded credit and signature debit card transactions for its Network Access Brand Usage fee. Revenue generated from the NABU fee goes directly to MasterCard. It is not collected by credit card processors or issuing banks.

MasterCard began charging the NABU fee is April of 2009. Prior to the $0.0185 charge, MasterCard assessed a $0.005 Acquirer Access Fee to transactions run through its network.

Since revenue from the NABU fee goes directly to MasterCard, most processors assess the fee to businesses at cost. However, in the case of tiered pricing the NABU fee is bundled with a business’s general qualified, mid-qualified and non-qualified rates. Although uncommon, it is possible for processors to markup the NABU fee even for businesses that are billed via more transparent interchange plus pricing.

To avoid confusion, the NABU fee is NOT related to:

Breaking News from The Official Merchant Services Blog: MasterCard and Discover have announced interchange increases and modifications to take effect October 2012. Specific association modifications such as these are beyond the control of payment processors like Host Merchant Services. They come directly from the big card associations themselves. These changes affect all merchant card processors and their customers, meaning these changes in fees and rates travel in a straight line from Visa, MasterCard and Discover to the merchants.

The Meat and Potatoes

MasterCard will be reducing the Consumer Debit rate from 1.64% + $0.16 to 1.60% + $0.15. MasterCard will increase the Small Ticket Debit rate from 1.30 + $0.02 to 1.30 + $0.03.

Discover Card will be enacting several changes to their PSL Public Services interchange fee programs. Rates will increase from 1.50% +$0.10 to 1.55% + $0.10. Discover PSL Card-Not-Present/E-Commerce Premium Plus will increase from 2.30% + $0.10 to 2.35% + $0.10. Discover will also increase Key Enter Premium Plus from 2.10% + $0.10 to 2.15% + $0.10.

Add These Fees to the Pile

These changes come on the heels of a series of changes we reported back in February. Visa’s new Fixed Acquirer Network Fee and Transaction Integrity Fee made all of the headlines back then, but MasterCard also implemented its new annual Acquirer License Fee. This fee took effect in July 2012. MasterCard also implemented a new annual Type III Third Party Processor (TPP) Registration Fee in July 2012.

MasterCard based these fees on a full year of 2011 volume for each merchant, and for 2012 only the fees are 50% of the total fee calculated — since they cover only half of the year. MasterCard passed these fees through on a pro-rata basis and all acquired MasterCard credit and signature debit volume was utilized to determine the annual volume for both programs. PIN debit volume was excluded.

The changes to Discover Card’s PSL Public Services interchange fee programs are also in addition to a series of changes Discover announced back in February. Discover introduced a US Commercial Large Ticket Interchange program, increasing its assessment fee by .005%. Discover also changed existing card present Interchange rates for transactions less than $15 for Express Service merchants (Local Commuter, Bus Lines, Toll & Bridge Fees, Restaurants, Fast Food Restaurants, News/Dealer Stands, Laundries, Dry Cleaners, Quick Copy & Reproductions, Parking Lots/Garages, Car Washes, Motion Picture Theaters and Video Entertainment Rentals) and less than $25 for Taxi/Limo merchants.

Pay Attention to Your Statement

As stated above, these changes are made directly to Interchange rates from the Card Associations. Unlike Visa’s much ballyhooed FANF, which is a completely new fee and not subject to regulation from the Durbin Amendment, these fees fall under the scope and purview of Interchange, and thus Durbin.

Merchants will begin to see the following text on their August Statements to explain the changing fees:

Visa, MasterCard, Discover Card Services have announced category introductions and modifications to their current interchange structures. These changes may affect your current pricing effective October 2012. Further detail specific to these changes and impacts to your merchant account will be detailed on your September merchant statement. As previously disclosed on your February and March merchant statements, MasterCard introduced the new MC licensing fee. Beginning in August 2012, the new licensing fee of $.005 will be included with the MasterCard NABU billing and appear as “MC assoc NABU/license fee”. Thank you for your continued business.

{kind=link}

{kind=link}