This is the latest installment in The Official Merchant Services Blog’s Knowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is:

Virtual Terminal

A Virtual Terminal is a form of secure online payment processing. Using these web-based applications to create a virtual terminal, a merchant can access over an interject connection all the needed credit card processing capabilities from any computer through a secure, password-protected login.

After logging into the environment, a merchant can manually enter credit card details and perform any credit card processing transaction that a Point-of-Sale Terminal would perform, including authorization, capture and refund.

The process looks a lot like going to a secure web site. It’s flexible and can be used from a variety of locations allowing a merchant to either replace their standard terminals or use this as an option for when they’re out in the field. Virtual Terminals are very easy to use, accessed via Secure Socket Layer Encryption (SSL), enable separate authorization and settlement transactions, connect to Address Verification System (AVS) and Card Verification Value (CVV) fraud tests and support multi-user access with multiple permissions. In short, you can run your entire payment processing protocol through a virtual terminal safely and securely.

For more information, you can review how the process works at this link.

You can also find out more about the virtual terminals Host Merchant Services offers at this link.

Today The Official Merchant Services Blog is here to talk about merchant accounts — specifically ways for business owners to maximize their usage of their merchant accounts.

The Basics

First we’ll address the most basic element of the topic: What is a merchant account?

A merchant account is a type of bank account that allows businesses to accept payments by debit or credit cards. A merchant account is established under an agreement between an merchant services provider, like Host Merchant Services, and a merchant acquiring bank for the settlement of credit card and/or debit card transactions.

Having a merchant account can really boost your business. It gives you more flexibility and lets you obtain revenue from a variety of sources consumers have for purchasing goods and services.

Payment Network Providers and Merchant Services Companies provide a wide variety of services. Host Merchant Services, for example, provides processing for retail merchants directly on their premisses. But HMS also provides e-commerce solutions in the form of online payment gateways — including Host Merchant Services’ very own HMSExpress — as well as mobile payment technology. Merchants have so many different options available to them that they can customize their merchant account to fit their flexible and ever-changing business needs.

Here’s a review of some of the most typical mistakes that business owners make with their merchant accounts, and a look at how Host Merchant Services Guarantee helps you avoid them.

Did Not Ask Questions

A lot of merchants are either lost in the details and fine print of payment processing or they are intimidated by the process and do not ask questions of their processor. Do not be intimidated. Always ask questions about your contract, your fees, your statement — everything. The jargon used in payment processing can sound like technobabble or biz-speak, so make sure you get all the clarification you need. High or hidden fees, bad service, long term contracts with hidden rules or steep penalties can have a negative impact on your business. So make sure you keep on top of the details.

Host Merchant Services provides a variety of online resources to keep merchants in the know.

They are always available to answer your questions and help guide you through the confusing maze that payment processing can be.

Lured in By Free Perks

Many processors offer perks, a common one being Free Equipment. This type of bonus is designed to get your attention, but many processors tack on hefty hidden fees to the deal, covering the cost of the freebie. The payment processing industry can be cutthroat at times and companies use aggressive tactics to board merchants. It’s very important for merchants to be aware of what they are signing up for and the true cost of the merchant services before they get locked into a bad deal.

Host Merchant Services offers a free equipment perk as part of its guarantee. The big difference with HMS and other processors is that HMS does not lock its customers into contracts. HMS also offers a transparent statement, with no hidden fees. The perk is exactly what it claims to be: Free Equipment. What you see is what you get.

Not Shopping Around

A lot of merchants find payment processing dense, sometimes confusing, and certainly a boring topic. So many of them will not comparison shop. This is a very big mistake. Take your time with offers and research the company pitching the offer to you. Read the fine print of each contract and see the differences in the numbers yourself.

Host Merchant Services offers a free statement analysis to every merchant they visit. HMS sales representatives will go over your statement, find the hidden fees and then go over step-by-step how the pricing structure HMS offers is different, and transparent. The HMS Guarantee even offers a free gift card if the company can’t save you money after the statement analysis.

The Cancellation Fee

Many merchants ignore or forget about the cancellation fee they face when changing payment processors. Cancellation fees are designed to keep a merchant locked into a contract. Some of these cancellation fees are exorbitant and restrict a merchant’s options. Some processors also tack on equipment fees for having to take back the used credit card processing terminal.

Host Merchant Services offers no cancellation fees. No fees for returning used equipment. And as part of the statement analysis and the sales pitch, the company takes any cancellation fees a merchant faces for switching into account and still finds a way to lower a merchant’s rates and save a merchant money.

Not Getting it in Writing

A salesperson in the ultra-competitive merchant services industry can sometimes make a pitch that sounds too good to be true. Always ask that salesperson to point it out in the contract they offer. In short, get it in writing. One common tactic merchants will find themselves being barraged with is a payment processor will offer a better specific rate. This shows up in Tiered Pricing models. But the way the pricing is structured, the reality is the merchant doesn’t get that savings when their monthly bill shows up. Some really bad examples will go a step further and hide the added fees, so the merchant won’t even know that they are being billed at a rate they weren’t quoted, because of the technical nitty gritty of the plan they signed up for. Hidden fees get abused quite a bit in situations like this.

Host Merchant Services adheres to no hidden fees. The company explains its pricing, and that’s the pricing you get. The company shows you your statement, goes over everything that is in writing and sees to it that you get exactly what you signed up for. It helps that the company utilizes the Interchange Plus pricing plan, which is far more transparent than the Tiered Pricing structure many other processors use.

The Official Merchant Services Blog ran a series on Tiered Pricing versus Interchange Plus Pricing back in 2011. You can review those blogs here and here and here.

That’s pretty much it in a nutshell. Merchants need to be focused and ask a lot of questions of their payment processor. If a merchant is relentless in their pursuit of understanding they will find that they can get quality processing with a good plan and great rates.

Today The Official Merchant Services Blog reacquaints itself with a very important topic: Security. Specifically we’re jumping back into the discussion about PCI Security standards. Consumers are using plastic, especially online, at record rates. But security is still a major concern. Credit card fraud, phishing scams, clickjacking and identity theft are all on the rise and transaction security is an increasing concern for more than just payment network providers — it’s a major issue for merchants as well.

As we’ve reported in past blogs, statistics show that merchants are still having trouble keeping up with PCI Compliance. Our October 7, 2011 Blog cited a study by Verizon that stated 79% of organizations were not fully PCI Compliant. Then our December 15, 2011 Blog cited a further study by Gartner Research that found 18% of merchants are not PCI Compliant at all.

Some Tips That Can Help

To help combat the issues these studies have raised, we’re going to offer five tips that can help merchants reassure customers that their credit card data is safe and secure. Following these tips can help build stronger customer loyalty and just generally promote the feeling of safety that comes with using your business among your consumers.

Start a Security Campaign

You can help assuage anxious customers through a marketing campaign that teaches them to protect their identities. Take the initiative and help them with their own private security. Host Merchant Services Article Archive provides a series of useful resources on combating identity theft here. You can point your customers to those resources, you can send regular emails, tweets and texts to customers that provide privacy tips and fraud-prevention tactics.

Remind Consumers Of Your Security Measures

Keep your own business’ fraud protection features prominent with a mailer or newsletter letting customers know the steps you have taken in the area of security. You can blend this with your security campaign, and keep your customers aware of the security features they have just by patronizing your business. Emphasize privacy rules you have in place and what steps you take to comply with standards like the PCI DSS.

Work With Card Companies

Beyond just PCI DSS, major credit card carriers like Visa offer fraud-prevention measures. Take advantage of these extra measures. And let your customers know you go this extra mile. Everything from regulations that prompt merchants to produce receipts with only partial card data to the use of special “codes” to hide card data on receipts. Every little bit helps.

Get Your Employees On Board

To ease consumer unrest over security issues, it will greatly help you to have your entire staff on board with your security measures and the marketing campaign that pushes those measures. Your employees are customer facing and so having them well versed in the steps you take to make transactions secure will make consumers feel a lot safer during the shopping experience.

Be Ever Vigilant

Just like in Batman or Superman adventures, the war on crime is a never-ending battle. To maintain your security measures and to consistently promote how well you maintain those standards, you need to be like Batman — ever vigilant. Always maintain good records. Keep those records secure. Keep credit card receipts away from the public. Make sure your data that you store is password protected. And always maintain your PCI Compliance.

That’s the basics of helping your customers feel safe about transactions. Go the extra mile, be ever vigilant, and let them know what you do for their benefit.

Earlier, The Official Merchant Services Blog began a series on free Open Source E-Commerce solutions that are available. We cited this article by Nova Scotian writer Vangie Beal, which lists her top 10 free online shopping carts. Today we finish up our review of Beal’s list.

Before We Get Back to the List

Before we pick up where we left off yesterday, we’d like to take a moment to look at some of the wealth of information on e-commerce that Host Merchant Services offers through this blog and its article archive.

You can read the HMS Overview of E-Commerce here.

You can learn about the HMSExpress Payment Gateway here, and read about why it’s useful for a budding online business in the September 20, 2011 blog here.

This September 22, 2011 blog details 8 easy steps for starting an online business.

You can learn about the customizable e-commerce and payment processing solutions that Host Merchant Services provides here.

Our January 3 blog gives a review and preview of E-Commerce from 2011 to 2012.

You can sign up for a merchant account with Host Merchant Services and get started with your online business here.

And now, back to Beal’s list. We left off yesterday with number five on the list, Magento. So let’s move on to number six …

Number Six: OpenCart

OpenCart arrives on Beal’s list as number six. This shopping cart, according to Beal, is quick and easy to install. Storeowners can select a template, add products and start taking orders online seamlessly after the download. The built-in template system lets merchants switch up quickly or migrate their site’s current design into OpenCart, giving added flexibility. Other features are a mutli-store capability to manage more than one store from one administrator interface, tax zones, shipping method controls, back-end store administration tools and support for a variety of payment gateways and languages.

OpenCart, says Beal, is a free open source software published under the GNU GPL License and its server requirements include Web Server — preferably Apache — PHP 5.2 or higher, MySQL, Curl and Fsock.

Number Seven: osCommerce Online Merchant

The osCommerce Online Merchant comes in at number seven on Beal’s list. This e-commerce solution is a free offering that comes with features and tools to help merchants manage the front-end catalog and back-end administration of an online store.

This software is released under the GNU General Public License and version 2.3.1 provides a basic template layout structure to customize the catalog. The Administration Tool, according to Beal, lets merchants configure the online store, insert products for sale, manage customers and process orders. The software is supported by a large community of more than 256,000 storeowners, developers, service providers and enthusiasts, as well as additional support from mailing lists and the osCommerce Newsletter. Server requirements for this software include PHP v4 or better — though 5 or higher is recommended — and MySQL v3 or higher.

Number Eight: PrestaShop

PrestaShop cracks Beal’s list at the number eight spot. This customizable, PCI compliant, e-commerce solution will handle everything from Web store set-up to managing customers and orders according to Beal. Storeowners create and manage the front-end catalog as well as marketing campaigns. They can customize orders and change shipping options. PrestaShop is available in English, French and Spanish — and also offers an additional 41 translations. This software is published under the Open Software License v3.0 and its server requirements include Linux, UNIX or Windows, Web Server — Apache 1.3 or later, IIS 6 or later — PHP 5.0 or later and MySQL 5 or later.

Number Nine: Zen Cart

Zen Cart makes it onto Beal’s list as the number nine entry. One of the draws of Zen Cart is this software is a free and open source shopping cart designed by a group of show owners, programmers, designers and consultants — essential it’s designed by the people that use it for the people that use it. It has the similar setup that a lot of the above mentioned carts have. It uses a template system to select a design and configure product categories, discounts, shipping options and payment options. The cart incorporates a WYSIWYG page editor for modifying non-database pages. Since it’s a bit of a community derived product itself, Zen Cart’s support is through its community contributed additions and documentation as well as its online forum found on its website.

Number Ten: ZeusCart

Rounding out Beal’s top 10 list of open source e-commerce solutions is ZeusCart, a web-based PHP/MySQL shopping cart that boasts a rich user interface and an easy-to-use shopping cart that meets the cutting edge of Web 2.0 evolution. ZeusCart, according to Beal, is targeted toward small and medium storeowners and offers inventory management, attribute-driven product catalog services, category management, built-in CMS and SEO-friendly URLs. It also comes with the standard features such as discounts, taxation, shipping options, integration with multiple payment gateways and e-mail templates. It is licensed under GPL 2 and can be installed on any server where a PHP interpreter, MySQL database server and a web server is present.

That’s Beal’s top 10 list. What other open source e-commerce shopping carts do you know of? Have you any experience with the ones on this list? Feel free to share you experiences in our comments section.

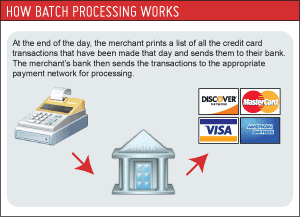

As part of an ongoing series covering the basics of payment processing, The Official Merchant Services Blog is going to discuss Batch Processing today. You may have seen the term come up before –– possibly in reference to your statement or when your merchant account representative first met you.

What is Batch Processing?

Providing quick and efficient service is key to a successful enterprise. This is also applicable to the process of accepting credit card payments as processing your transactions quickly will also ensure prompt and timely receipt of payments for your products. And that’s where Batch Processing comes in.

Batch processing is the mass processing of dozens of credit card transactions. It tends to be much more convenient to batch process hundred of orders at a certain time during the day, instead of each and every time they are received. A lot of merchants process their batch at the end of business. E-commerce businesses have batch processing built into their payment gateways. In fact, Step Five of our “How Payment Gateways Work” graphic details the daily “batch.” In fact, using a payment gateway will help simplify your batch credit card processing as it will help you coordinate the many functions that are necessary to process your payments. This form of card processing also has the benefit of being secure and this will certainly be a value added to your customer service.

How does Batch Processing Work?

Here’s an infographic that explains the batch process as it happens:

Batch credit card processing works well with small businesses where several credit card transactions are processed simultaneously, in the batch. With this, there is a definite lower risk of credit card fraud and you will be able to offer your customer and your business the assurance of transaction security.

The one con to Batch Processing

On occasions where there is a problem with the credit card payment, the seller may not know till the next day. Batches get processed with a lag. Host Merchant Services has 2 day processing. So there can be some issues with payments due to that lag. But the company has a qualified representative available 24 hours a day, 7 days a week, to help you with any issues you encounter in processing your transactions.

The Official Merchant Services Blog tackles the topic of Debit Card processing today. While the blog has extensively delved into the Durbin Amendment and the affects the legislation is having on merchants, one topic we’ve overlooked is Debit Card processing –– specifically PIN Debit vs. Swipe Debit.

Difference Between Credit, Debit, and Check Cards

First thing we need to do is define debit cards. True debit cards can only be accepted when a merchant is able to accept a personal identification number (PIN) from customers using a PIN pad. So for true debit cards, the only option is PIN Debit.

Buttransaction processing has been evolving. Most debit cards today are actually check cards that are mistakenly referred to as “debit cards.” The difference between a debit card and a check card is that a check card has a Visa or MasterCard logo in the lower right-hand corner where a true debit card does not. These cards are hybrids and can work as either a credit card or a debit card when used in a transaction. Amerchant account allows a merchant to accept debit, credit and check cards.

Price Comparison

Prior to the Durbin Amendment taking affect, PIN Debit was the most cost effective choice for debit card/check card transactions. Swipe, or Signature-based, debit transactions carried higher interchange ratesthan PIN debit transactions for many years.

Once the Durbin Amendment took affect on October 1, 2011, the fees for both PIN Debit and Signature Debit were balanced. Swipe Debit now costs as much as PIN Debit for banks that are capped by the Durbin legislation. Swipe Debit is also, in rare cases, less expensive than PIN Debit in situations where the bank is exempt from Durbin rules. The change that the Durbin Amendment brought on has many merchants asking the question: If Signature and PIN debit are now capped at the same interchange fee, do I still need my PIN Pad?

Continue Reading – PIN Debit vs. Swipe Debit, Part 2

The Official Merchant Services Blog completes its three-part series on Payment Gateways. Today’s installment discusses the pricing structure of Payment Gateways and takes a detailed look at the pricing options for the Payment Gateway Solutions that Host Merchant Services offers.

What Are the Costs of Payment Gateways?

The costs that you will have to pay for a Payment Gateway break down like this:

Discount Rate

Monthly Fees

Per Transaction Fees

Setup Fee

Discount Rate

A discount rate is the percentage of each transaction that you pay to your card processor for processing your credit card sales. These fees are largely influenced by the percentage that MasterCard and Visa charge processors. Discount rates are usually in the 2-6% range, but do vary greatly depending on the payment gateway/merchant account specifics that you choose.

With Host Merchant Services, you do not have to pay a discount rate for any of their Payment Gateway Solutions.

Monthly Fees

Typically Payment Gateways that require a merchant account charge a monthly fee. It is part of the merchant account application process, and the prices can vary depending on what add-on services you may choose with your account. A very popular add-on feature, for example, is fraud detection. With many Payment Gateways, the merchant is offered a number of tools to help guard against fraud, such as filters to define the scope of people or places you receive payments from. Authorize.net, one of the Payment Gateway solutions Host Merchant Services offers, has an Advanced Fraud Detection suite available. These types of tools can help reduce chargebacks.

Per Transaction Fees

Most Payment Gateways charge fees for each transaction you process. This fee is usually a flat fee and under $0.50 per transaction. There is some variance in how much that fee can be. For example, the Authorize.net option that Host Merchant Services provides with its Merchant Accounts only has a 5 cents per transaction fee. And the HMSExpress option that Host Merchant Services provides is rare in that it has no added frees for individual transactions.

Setup Fee

A lot of Payment Gateway options also charge a one-time setup fee. Host Merchant Services, however, does not charge a setup fee for its Payment Gateway solutions with its Merchant Accounts.

So that’s an overview of the fees that are involved with Payment Gateways. Lined up together like that you get a picture of what the cost of convenience and security could be for your online business. You also see that Host Merchant Services strives to offer competitive rates with less fees than other Merchant Account providers.

Host Merchant Services offers two basic Payment Gateway options: Authorize.net, and HMSExpress. Authorize.net, which is one of the three largest Payment Gateways offered, costs HMS Merchants a base fee of $10.00 a month and 5 cents per transaction. HMSExpress, the new virtual terminal solution that HMS offers, costs its merchants $10 a month and has no added fees for individual transactions.

What Criteria Should Merchants Consider when Choosing?

Here are some factors merchants need to consider when choosing a Payment Gateway. Keep in mind that the overall goal is to find what works for your business, so don’t let this decision overwhelm you.

How many transactions to you expect to process per month?

If you expect a low volume of online payments each month, then you would want to consider avoiding monthly fees and a high setup cost, as it will take you longer to turn a profit.

Do you plan to utilize auto-billing?

If your business has a need for storing your customers’ payment information, and you need to charge them on a recurring basis, then you need to make sure that you choose a Payment Gateway that gives you this option.

How international is your business?

If your business plans on processing payments from all over the world, you need to choose a Payment Gateway that allows you to do so. Not all options out there can handle international currencies smoothly and seamlessly.

Don’t forget support.

Technical support and customer support are something you can’t overlook when choosing your Payment Gateway. After considering the costs and the setup, the issue of support becomes paramount for the long-term viability of your processing capabilities. When things go wrong, or when there are issues with chargebacks and fraud, you want a Merchant Services provider to be readily available to assist you. With Host Merchant Services, you get 24x7x365 support available to you. The company has its own fraud prevention specialists available to assist you above and beyond what the payment gateway add-ons can provide. And most importantly, when you call in with a problem you get to talk to a person instead of being routed through a phone-tree maze.

The Choice is Yours

As a merchant you want to find the best service tempered by the most affordable rates, when it comes to your Payment Gateway options. It’s important to consider how important the ability to take online payments can be for your business. It opens you up to a wider customer base. It also gives you fast, secure transaction processing. Feel free to shop around and compare the options available to you, and keep in mind that Host Merchant Services provides Payment Gateway solutions with its Merchant Accounts that have less fees than a lot of the other choices you will come across.

The Official Merchant Services Blog continues its series on Payment Gateways. Yesterday’s blog dealt with the basic question of why your business would want a Payment Gateway in the first place. It also looked at the basic setup and costs of a Payment Gateway and some of the differences in the Payment Gateway options that Host Merchant Services offers.

Today’s blog is going to examine how Payment Gateways work.

How Do They Work?

A Payment Gateway is literally a link between a merchant, the client, the client’s credit card provider and the merchant’s bank. The main job of the gateway is to validate your customer’s credit card securely, make sure the funds are available and get you paid. The system is based on the transaction process you see in your standard retail store, where a credit card is swiped. But it does not require a card to be present to be charged.

Some gateways also require a merchant account –– a specific type of bank account that handles your funds received via credit cards. Host Merchant Services provides its merchants with Payment Gateway options as part of the services that come with opening a merchant account through the company.

Host Merchant Services has created an easy to read, step by step graphic on Payment Gateways. You can view that graphic here.

But to briefly walk you through the process:

1.A customer places an order on a merchant’s website and submits the order through the site.

The website then encrypts the payment information that is to be sent between the browser and the merchant’s webserver. This is done vial Secure Socket Layer (SSL) Encryption.

The merchant then forwards the encrypted transaction details to their payment gateway.

The Payment Gateway forwards the secure transaction information to the payment processor (in this instance, Host Merchant Services).

The processor forwards the information to the card association (be it Visa or MasterCard or Discover).

The credit card issuing bank receives the authorization request and sends a response back to the processor with a response code.

This response gets forwarded to the Payment Gateway.

The Payment Gateway sends the response back to the website where it is interpreted and relayed back to the cardholder and the merchant. This entire process of forwarding the information for a response, and getting the response back takes 2 to 3 seconds typically. Not only will the response of approved or declined be generated but the process also defines why a transaction might fail, and lists the reason.

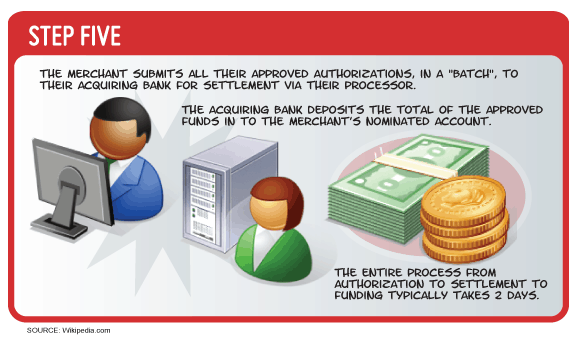

For an approved transaction, the Merchant then submits all of their approved transactions in a “batch” to the acquiring bank for settlement at the end of its business day. The acquiring bank deposits the total of the approved funds into the merchant’s account. Settlement of “batches” typically takes 2 days with Host Merchant Services.

How Do The Transactions Stay Secure?

The security of these transactions are important. Security is the key reason Payment Gateways exist, as the entire point of the system is to get sensitive payment information transmitted from a customer’s web browser back and forth to a bank for approval of the purchase. Here are some of the technical details that happen with Payment Gateways to ensure the process remains secure:

Since the customer is usually required to enter personal details in the transaction process, the payment gateway is often carried out through HTTPS protocol.

To validate the request of the payment page result, signed request is often used – which is the result of the hash function in which the parameters of an application confirmed by a «secret word», known only to the merchant and payment gateway.

To validate the request of the payment page result, sometimes IP of the requesting server has to be verified.

There is a growing support by acquirers, issuers and subsequently by payment gateways for Virtual Payer Authentication (VPA), implemented as 3-D Secure protocol – branded as Verified by VISA, MasterCard SecureCode and J/Secure by JCB, which adds additional layer of security for online payments. 3-D Secure promises to alleviate some of the problems facing online merchants, like the inherent distance between the seller and the buyer, and the inability of the first to easily confirm the identity of the second.

Up Next

In tomorrow’s entry in this series we will take a look at the costs of a Payment Gateway, specifically the options Host Merchant Services offers and then analyze some of the criteria a merchant needs to consider when choosing a Payment Gateway.

{kind=link}