Today The Official Merchant Services Blog is taking a look at a bill being debated on the U.S. Senate floor this week. Senate Bill 1832, also known as The Market Place Fairness Act could be the cause of the next big debate in the Payment Processing Industry.

The Law of the Land

In 1992 the Supreme Court ruled in the case Quill v. North Dakota that companies without a “substantial nexus” in the state where their customer lived didn’t have to charge sales tax. Seemingly favoring Internet companies, this ruling was actually handed down two years before the first Web browser, and three years before Amazon ever sold it’s first book. This law still stands today, and is the precedent for online retailers not having to pay state taxes on products shipping nation wide. This new bill looks to rectify that apparent “oversight.”

The Act Itself

The Marketplace Fairness Act would pave the way for states to require online sellers from out of state to begin paying the sales tax they’ve escaped for years. Senator Dick Durbin (D-Ill.) said “The Marketplace Fairness Act would level the playing field for small businesses by allowing states — if they so choose — to treat brick and mortar retailers the same as remote retailers.” Durbin, who is sponsoring this bill, is best known for authoring the Durbin Amendment, a piece of legislation that caused much controversy in the Payment Card Industry when enacted.

The National Conference of State Legislatures estimates the lost tax revenue at $23 billion annually. Senator John Rockefeller (D-W.V.) spoke on the issue, attempting to clear up some of the confusion, “To be clear this debate is not about imposing new taxes. Instead it’s just allowing a state to collect taxes they are currently owed under existing law, but are being systemically avoided.” As another benefit to small business owners, the law would only apply to business processing more than $500,000 annually.

Amazon Action

Amazon has been the most vocal in its support of the Marketplace Fairness Act since it’s introduction last year. Speaking before a congressional hearing, Amazon VP of Global Public Policy Paul Misener told lawmakers that the bill would facilitate the collection of one kind of tax that is already due, but goes largely unpaid. Supporting the argument that it is not a new tax increase.

Opposition

Senator Jim DeMint (R-S.C.) published an op-edin the Wall Street Journal entitled “No Internet Taxation Without Representation.” In the piece DeMint argues that citizens should not be taxed by governments in which they have no political voice — in this case states where they or their company are not physically based. I would argue that this is a cost of interstate commerce, which has been reborn as interstate e-commerce.

DeMint does have a point when he mentions the nearly 10,000 state, local and municipal tax jurisdictions businesses would have to comply with nationwide. He forgets to mention, however, that businesses have access to advanced tax software, such as TaxCloud, which can easily compute the sales tax for any state.

The Verdict

Here at The Official Merchant Services Blog, we see the potential savings this offers to the owners of small businesses nationwide. The Marketplace Fairness Act provides an incentive for states to simplify their sales tax laws, as well as increase revenue from the ever-booming e-commerce industry. Hopefully this will decrease the sales tax burden shared by many small businesses. It simply makes it much easier for millions of business owners — and in turn the states — to collect the taxes already due. Only time will tell how much impact this legislation will have on e-commerce and credit card processing. We will stay on top of any new developments on this law, and how they affect you.

Today The Official Merchant Services Blog delves into the intricate and fascinating world of social media marketing and the pitfalls of Click Fraud. Our interest stems from a recent news story: Limited Pressing, an e-commerce company provides a platform for selling digital music and physical items, stated that they are dropping their Facebook page and removing their company’s Facebook presence because it determined that 80% of the clicks it paid for through Facebook advertising were fraudulent.

What is Click Fraud?

Click fraud is an illegal practice that occurs when individuals click through advertisements — either banner ads or paid text links — to increase the payable number of click throughs to the advertiser. The fraudulent clicks could either be performed by having a person manually click the advertising links or more typically by using automated software or Online bots that are programmed to click these ads repeatedly. Click fraud is sometimes perpetrated by individuals who use the tactic to increase their own personal banner ad revenues; but the most common strategy is click fraud gets harnessed by companies as a way to deplete a competitor’s advertising budget.

This is where Limited Pressing’s problems with their Facebook Page comes in. They feel that the click fraud was eating up their ad budget and making the oft-lauded and extremely popular advertising tool too costly and ineffective.

Limited Research

In this article at clickz.com, Limited states that it determined over a one-month testing period that 80 percent of their Facebook ad clicks were performed by bots. The company doesn’t really delve into where the bots come from, and instead focus their criticism on Facebook’s entire ad platform — suggesting its findings indicate Facebook has a big click fraud problem.

Limited detailed the process they used to determine this bold assertion of click fraud:

“A couple months ago, when we were preparing to launch the new Limited Run, we started to experiment with Facebook ads. Unfortunately, while testing their ad system, we noticed some very strange things. Facebook was charging us for clicks, yet we could only verify about 20% of them actually showing up on our site.

At first, we thought it was our analytics service. We tried signing up for a handful of other big name companies, and still, we couldn’t verify more than 15-20% of clicks. So we did what any good developers would do. We built our own analytic software. Here’s what we found: on about 80% of the clicks Facebook was charging us for, JavaScript wasn’t on. And if the person clicking the ad doesn’t have JavaScript, it’s very difficult for an analytics service to verify the click. What’s important here is that in all of our years of experience, only about 1-2% of people coming to us have JavaScript disabled, not 80% like these clicks coming from Facebook.

So we did what any good developers would do. We built a page logger. Any time a page was loaded, we’d keep track of it. You know what we found? The 80% of clicks we were paying for were from bots. That’s correct. Bots were loading pages and driving up our advertising costs.”

Clickz.com pressed the company for more details on the process they used and the data Limited obtained. But the company had nothing prepared to share with the site yet.

Facebook Strikes Back

Facebook defended its program and its protocols in response to Limited’s claims. The company has said it is investigating the claims that Limited has made, and noted that it has defenses in place for such kind of fraud. A fake click, Facebook said, would come from a fake account, which would be disabled immediately upon discovery.

This Computer World article details Facebook’s defense that the company supplied in an e-mail. The article reveals that Facebook has systems in place that attempt to detect and filter certain click activity, including repetitive clicks from a single user, clicks that appear to be from an automated program or bot, or clicks that are otherwise abusive. Facebook’s systems also look at whether JavaScript is enabled in the browser. And the company reports that according to recent data, nearly all billable clicks resulting from desktop web browsers have JavaScript enabled.

Also, in a second quarter earnings report conference call Facebook said they are continually making efforts to reduce fraudulent activity and fake accounts by becoming better at detecting duplicate accounts.

As reported by clickz.com:

“On a macro level, Facebook now has independent ROI data from more than 60 advertising campaigns using a variety of third-party methodologies like panels and marketing mix models. The results show that 70 percent of campaigns resulted in a return on ad spend of 3x or better, and 49 percent of campaigns showed a return on ad spend of 5x or better.”

Facebook COO Sheryl Sandberg said during that conference call that “attribution is an issue. Marketers need to tie sales back to multiple touches; they may see on Facebook and search later. Our ads work and the ROI is there, so we’re focusing on education.”

The Big Picture

This issue is an important one for payment processors and merchants alike. Much has been made of social media and marketing. Facebook’s ad service is a huge windfall for the company. Much of what I myself have learned about marketing through social media has come directly from webinars and videos I’ve seen given by Sandberg. So if Limited’s claims are anywhere close to accurate, this could be devastating for Facebook — and equally positive for competitors like Google and its Google+ social media hub that still trails Facebook in popularity.

Essentially Facebook ads are at the forefront of the immense push people have made into spending money on social media marketing campaigns. So if only 20% of that money is doing the job, it’s an extreme waste of resources for businesses.

In Facebook’s Defense

There’s much to be said in defense of Facebook at this time however.

First of all, the company is very diligent in its pursuit of click fraud. In our January blog, we explored the activity called Clickjacking and detailed how Facebook has been fighting to curb that kind of fraud. And since the company is now extremely invested in its own profits after its IPO, it really is common sense that they are being forthright in their responses and really are doing the best job they can to curb fraud.

Secondly, Limited’s credibility takes a hit with the other issue it brought to light in its criticism of Facebook. It claimed that Facebook was allegedly holding Limited’s page name hostage. What Limited said was that it wanted to change its name on its Facebook page and that after repeated attempts to contact Facebook about the issue, Limited received a response. Facebook, Limited alleges, would make the name change for Limited if the company agreed to spend $2,000 a month or more in advertising.

Here’s where Limited’s credibility starts to wane. Limited Pressing wants to change its name to Limited Run. That name has been in use by a magazine since October 2010. So there’s no way Limited could get the name changed. Facebook also states that it does not charge for name changes. Facebook clarified that they have a process that business pages have to go through to get a name changed so that it doesn’t confuse its users if a business repeatedly changes its name or changes it to something unrelated. So Limited’s claims of Facebook holding its desired name hostage don’t seem to really pan out, hurting their credibility with their click fraud data.

And finally, the data itself. Limited’s claims tend to run extremely counter to all data released by Facebook itself and Limited has not shared the data or the services it used or page logger it created. They claim more details are forthcoming, but as we saw with the name change claim, the trustworthiness of the information could be very much in doubt.

The Bottom Line

So what are we to make of all this?

I’m taking it with a grain of salt. The accusation is strong enough and Limited does assure us all that they did a lot of data collection. If it turns out to be on the mark, then this is a really big hit for Facebook and something merchants need to consider in terms of how they go about using social media.

Also, a problem I have with Facebook’s defense is that there’s a loophole in the terminology they’re using in their statements: They say that when they detect fraud from fake accounts, they close the account. Simple right? Fraud, fake account, banhammer, done. But the loophole is that fake accounts need to be verified as fake to get closed. And skilled fraudsters will have these fake accounts looking as real as possible or simply replace it just as quickly as it gets nuked. My own experience with FB “drama” leads me to believe that on the one hand I believe Facebook is diligent in canceling the fake accounts it finds, but that the creation of fake accounts is too easy and too easy to fake properly that Facebook may not be affecting the fraud as much as it claims.

Still, I am very disconcerted by the name change issue as it’s pretty obvious to anyone who uses Facebook that it’s not Facebook’s fault you can’t have the name McDonald’s because McDonald’s already has the name.

In conclusion, I would say Facebook Ads are still right where I thought they were before I read these news articles. The huge push into social media is indeed a very powerful marketing tool that many merchants should embrace and utilize to their own benefit. But it’s a refined and subtle tool. It’s not something you just throw money at and expect clicks to turn to profits for your business. Host Merchant Services has found using Facebook ads increased our following quite a bit, but didn’t give us the targeted following of users that we really wanted. In short, we felt we got a lot of bots.

Part of that was our own inexperience with the tools available — though many video and webinar assistances later from Sandberg and Facebook we know how to use the tools much more effectively — and part of it was the Facebook culture itself. Businesses don’t always fit smoothly into the community. Facebook is far more casual and social so a business to business entity like our company, no matter how tech savvy we are, runs into some obstacles on Facebook. Finding the right people to send the ads to is difficult because our target audience isn’t as neatly confined by the tools Facebook provides — for example we found more success with the interest of “tacos” than we did for “business owners.” The more professional community of LinkedIn or the far more expansive twitterverse has ended up being a bit more successful for us.

I feel this might be part of what Limited was running into. I think there is indeed a substantial presence of fake accounts and bots on Facebook. But I also think that Limited’s target market, because of what they do as a business, isn’t exactly something folks on FB are hot to talk about and link-share. What is the hook that people on FB, already too distracted by pithy quotes and vaguebooking activities of their close knit group of friends, to talk about some business’ offer on stuff one of their affiliates can sell?

The TLDR version?Yeah, Facebook ads have a lot of bots and no Facebook can’t catch em all like Pokemons. But 80%? That number seems a tad high. And Social Media advertising is still a very valid and strong marketing tool for business owners.

Today The Official Merchant Services Blog is here to update our readers on the latest development in the lawsuit against Visa Inc., MasterCard Inc. — the largest antitrust settlement in U.S. history. We broke the story last week when we revealed that the card companies agreed to pay more than $6 billion to settle lawsuits from retailers claiming that the card issuers engaged in anti-competitive practices.

The July 13 settlement still needs to be OK’d by a judge, and today we learned that the decision may be getting held up by plaintiffs who do not want the settlement and the money it brings.

The Opposition and Their Position

The National Association of Convenience Stores (NACS), a class plaintiff in the lawsuit, rejected the settlement offer according to their own website. Because the proposed settlement does not introduce competition and transparency into the broken credit card swipe fee market, the NACS Board of Directors unanimously rejected the proposed settlement agreement.

The settlement is the largest antitrust settlement in U.S. history, but NACS was not impressed because it only amounts to less than two months’ worth of swipe fees, based on the estimated $50 billion in swipe fees collected by the credit card companies on an annual basis. Worse, NACS feels that with the settlement there are no fundamental market changes that would constrain Visa and MasterCard from continuing to raise rates.

Wal-Mart Joins Opposition

The NACS opposition was announced almost immediately after the news of the settlement proposal was revealed. It’s taken a little bit of time, but others have started to join the opposition. Wal-Mart Stores Inc, the world’s largest retailer, joined the growing chorus of merchants opposed to the proposed settlement. Wal-Mart said the $7.25 billion settlement would not change a “broken” system of what credit card companies charge retailers for processing credit and debit card payments, known as “swipe fees.”

For the Record

NACS and Wal-Mart share the same criticism of the settlement.

“Not only does the proposed settlement fail to introduce competition and transparency into a clearly broken market, it actually provides Visa and MasterCard with the tools to continue to shield swipe fees from market forces,” said NACS Chairman Tom Robinson, who is also president of Santa Clara, Calif.-based Robinson Oil Corp.

Mirroring the NACS criticism, Wal-Mart said in a statement released by the company, “the proposed settlement would not structurally change the broken market or prohibit credit card networks from continually increasing hidden swipe fees, which already cost consumers tens of billions of dollars each year.”

Robinson also said, “this proposed settlement allows the card companies to continue to dictate the prices banks charge and the rules that constrain the market including for emerging payment methods, particularly mobile payments. Consumers and merchants ultimately will pay more as a result of this agreement — without any relief in sight.”

Wal-Mart again mirrored the NACS statements and went further when it said the settlement would not “prohibit credit card networks from continually increasing hidden swipe fees, which already cost consumers tens of billions of dollars each year,” and would “also constrain emerging payments innovation.” These innovations the opposition keeps referring to most likely include mobile wallets that allow consumers to pay using their smartphones.

Stay on Target

Joining Wal-Mart and NACS as vocal opponents of the settlement was Wal-Mart competitor Target. In a July 20 statement, Target used the now familiar language that the united opposition is using when it said in a statement that: “The proposed settlement would perpetuate a broken system, restrict retailers from any future legal action and offer no long-term relief for retailers or consumers.”

The NACS, Wal-Mart and Target were also joined by SIGMA, an association representing independent motor fuel marketers and chain retailers, in opposing this settlement. And then the National Grocers Association jumped on the anti-settlement bandwagon on July 27. “NGA joined the lawsuit on behalf of its independent retail grocer members over seven years ago to bring about real reform of the anticompetitive credit card swipe fee system,” said NGA president and CEO Peter Larkin in a statement. “This proposed settlement agreement fails in this regard by allowing Visa and MasterCard to continue their dominant anticompetitive practices.”

The Final Word

So as opposition mounts, it may be all for naught. The final decision still rests with a judge. It will be up to U.S. District Court Judge John Gleeson to approve or reject the settlement, a process that will play out in Brooklyn federal court over the next few months.

For today’s installment of The Official Merchant Services Blog, we are bringing you the most recent developments of the now infamous Global Payments Data Breach.

Back in March

When we first reported the breach, it had supposedly affected 50,000 cardholders and revolved around a taxi and parking garage company in the New York City area. Over a short time, media outlets hyped up the story until the alleged number of affected cardholders hit 10,000,000. Global CEO Paul Garcia estimated that closer to 1.5 million card numbers were compromised. Garcia also said that the breach was “self-reported” and “absolutely contained.”

In a quick response to the breach, Visa decided to remove the Atlanta-based processor from its list of “compliant service providers.” This meant for the first time, Global would no longer be Payment Card Industry (PCI) compliant, a major problem for one of the world’s largest payment processors. However, more consequences were to come for Global.

Update # 2

In May we learned that the breach might have actually dated back to June of 2011, a full eight months earlier than previously predicted. Global stuck by it’s story that that the breach only affected 1.5 million cards or less, and occurred in February 2012. The initial source of the breach, however, Brian Krebs and his blog krebsonsecurity.com revealed that “a hacker break-in at credit and debit card processor Global Payments Inc. dates back to at least early June 2011, Visa and MasterCard warned in updated alerts sent to card-issuing banks in the past week.” Krebs also found that Visa and MasterCard were sending periodic alerts to the banks about cards that may need to be re-issued following a security breach at a processor or merchant.

The 3rd time’s the charm

Global Payments executives estimated Thursday that the data breach revealed earlier this year could cost them upwards of $120 million to fix. A large part of which is an $84 million dollar charge from the fourth quarter of fiscal year 2012 to cover fines and initial remediation costs from the payment card networks. Global CFO David Mangum said that the company also anticipates breach-related expenses and insurance payments in fiscal 2013 that could total $28 million or more. All the while, Global is working with a ‘Qualified Security Assessor’ in order to regain the PCI compliance certification they lost when the breach went public.

Tracking Track Data

Track data, is the raw cardholder data contained in a magnetic strip in a credit or debit card. In late May, Global asserted that only Track 2 data had been lost in the breach, which contains account numbers and expiration dates. Track 1 data contains cardholder names, addresses and other crucial data. Global seemed to be insisting that this would lead to less fraud since the thieves could not produce counterfeit cards with the stolen data. Union Savings Bank, based in Danbury, Conn was one of the banks alerted by Visa and MasterCard early, about potential fraud. Visa alerted USB that about 1,000 of its debit accounts were compromised in the Global Payments breach. These details show how Track 2 data alone was enough for criminals to encode the card numbers and expiration dates onto any card equipped with a magnetic strip. These cards can then be used at any merchant accepting signature debit, any transactions that do not require the cardholder to enter a PIN number.

Host Merchant Service’s PCI Compliance Initiative

Looking at the threat of a data breach, Merchants must wonder what the solution can be. Is there protection available?PCI Compliance is a great foundation for transaction security. The standards and protocols set up by the PCI-DSS Council are the first step a merchant needs to take to protect their data. And Host Merchant Servicesoffers a PCI Compliance Initiative that helps its merchants quickly and seamlessly take that step.

Also, one thing to consider if you are a merchant and you are worried about data breaches affecting your bottom line: Host Merchant Services Data Breach Security Program. Click that link to download a PDF explaining the value-added service HMS provides its merchants that goes above and beyond just simple PCI Compliance and helps ensure a merchant’s peace of mind.

The Mobile Payments Technology sector has been the topic of overt optimism for quite some time now. We’ve reported multiple times that industry analysts have predicted large gains in Mobile Payments profits over the short- and long-term future. Our article from 2011 showcased three different research groups and their take on the successful future they felt was in store for Mobile Payments.

More pieces of that predictive puzzle have been falling into place. According to a mobile payments survey conducted by IDC Financial Insights, mobile payments use in the United States has doubled. The May 2012 study looked closely at emerging pay method technologies and discovered that 33 percent of respondents had used their devices for mobile payments at least once.

IDC’s practice director, Aaron McPherson, told QRCode Press that “Based on our results, we expect to see continued growth in open-loop prepaid cards and mobile payments next year, and believe that the improvements being offered in electronic-bill delivery will break electronic-bill presentment and payment out of its doldrums as well.”

The Next Big Affirmation for Mobile Payments

Visa is convinced new payment tech, including mobile payments, are definitely the trend of the future — so much so that the card association giant is poised to showcase the power of the future in the spotlight of the 2012 Olympic Games in London. One of the new technologies Visa is thrusting into the public eye at the Olympics is EMV Chip Cards — something we highlighted back in February. Visa is heavily invested in Smart Card technology so it’s no surprise the company is using its Olympic Games partnership to point some attention at its EMV efforts. But right alongside that EMV push, Visa is also Mobile Payment Technology as a safe and convenient payment option for consumers throughout the London games.

Jim McCarthy, Head of Products at Visa Inc., said “This summer we will be demonstrating the future of payments in London – a future where most consumers will rely on mobile devices, tablets and PCs to manage their daily financial lives.” Visa’s Olympics marketing push for the future of Mobile includes:

Visa Mobile Payments and Services: A limited edition of the Samsung GALAXY S III, Samsung’s Olympic Games Phone during the London 2012 Games, will be provided to Visa sponsored athletes and trialists. The device will feature an Olympic-branded version of Visa’s mobile payment application, Visa payWave. To make purchases, consumers simply select the Visa icon on the Samsung device and hold the phone to a contactless payment terminal to pay.

Visa Mobile Prepaid: During the London 2012 Games,Visa Inc. will also showcase its newest product – Visa Mobile Prepaid – the first mobile-based Visa product providing consumers in developing countries a payment account that offers Visa’s high standards of security, reliability and global interoperability. By accessing their Visa Mobile Prepaid account on their mobile phone, consumers can send and receive international remittances, pay bills, top-up wireless minutes, and access Visa ATMs.

Setting New Standards

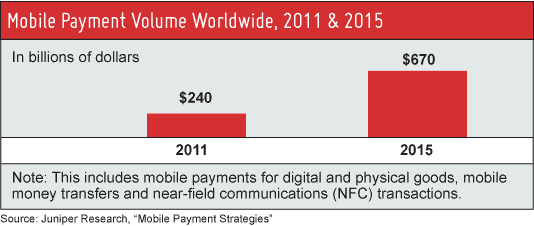

Looking at last year and then at this year’s statistics, Mobile Payments are doing their best to meet the bold predictions analysts have lined up for the future. The sector is growing rapidly and consumers in both the U.S. and around the world are embracing the convenience that the technology brings to their shopping habits. Juniper Research, a company that specializes in the identification and appraisal of high growth opportunities in various mobile telecommunications and applications sectors, put out a publication on July 5, 2011, titled “Mobile Payment Strategies.” Juniper predicted worldwide mobile spending would jump from $240 billion in 2011 to $670 billion in 2015.

Well Juniper is back with a new forecastthat focuses on Near Field Communication (NFC) and this study predicts that in just five years the NFC Mobile Payments market will will exponentially increase and eventually exceed $180 billion — a whopping seven times what it is today. The study forecasts that one in four people from Western Europe and the United States will use NFC as a payment mechanism by 2017.

Juniper cites last year as a turning point for NFC payments and suggests that major consolidation of the technology is the impetus for the predicted growth in the market as consistent standards and protocols will help fuel rapid growth and assuage the security concerns of consumers. Juniper says that in 2011 major technology infrastructure standards were finalized within the NFC Mobile Payments market so that many mobile network operators committed to the market and NFC payment pilots from both mobile operators and financial institutions transitioned to commercial service. And the research firm pointed to NFC-enabled smartphone models being announced by almost all handset manufacturers and Google as a key factor for igniting interest in the mobile payment usage in the U.S.

“This is a critical time for the NFC retail payments market,” said report co-author Dr. Windsor Holden. “Despite the significant progress being made today, the full potential of the market can only be fulfilled if all ecosystem players are equally committed and mobile wallet consortia remain in place.”

Today, The Official Merchant Services Blog is going to tackle a big picture topic in the world of credit card processing. Two weeks ago there was a proposed settlement of a lawsuit against Visa Inc., MasterCard Inc. Lawyers involved in the case claim it is the largest antitrust settlement in U.S. history. The card companies agreed to pay more than $6 billion to settle lawsuits from retailers claiming that the card issuers engaged in anti-competitive practices.

The July 13 settlement proposal — which still needs the OK by a judge — has stipulations that drop requirements that retailers charge the same price for cash and credit purchases. This opens the way for millions of businesses to add checkout fees when customers pay with plastic. In short, the settlement lets retailers push the cost of swipe fees off of them and onto the consumer directly.

A Paradigm Shift

This decision has really started to hit home for me personally. Just last week I was in the emergency room at Christiana Hospital waiting for a family member to be admitted. I got there around 5 a.m. and was in a rush so didn’t really bring much of anything with me. Hours later, I was hungry and in need of a snack. And I didn’t have any cash on me. But the vending machines at this hospital are state of the art. Which means they have fully equipped credit card swipers, allowing you to purchase snacks from them without pocket change or single dollar bills. That realization hit home with me as I noted both the power of credit card processing to be present in all aspects of my own life, and just exactly how much closer we’ve really gotten to being a cashless society. One of the last holdovers from the previous generation’s use of coins — vending machines — were now accepting credit cards. It was convenient and really helped me out in a time where I was far too worried about everything but having cash on me.

It will allow merchants the power to offset their processing fees in a very direct fashion that gives them control and power.

It will give the consumers themselves the incentive to start using cash again.

That first bullet point is good for the credit card processing industry as it allows merchants to feel more in control of their business and lets credit card processors offer more attractive savings directly to potential merchant accounts. But that gets offset by the second bullet point, as the consumer is then the direct decision maker on the purchase and has the power to affect the entire credit card processing industry by not using the plastic at all.

So Something’s Gotta Give, Right?

This boils down to an issue of convenience for the consumer. Plastic has always been the more convenient option. It’s easier to carry around than cash. And with a huge push still being made by Mobile Payment Processing Technology to make it even easier than plastic, cash still seems like it can be on the way out as we still careen quickly toward a cashless society.

But when faced with a choice between using cash and saving money, or using plastic and taking the hit on added surcharges directly, there will be a lot of consumers who will gladly switch back to cash. It won’t be that hard an adjustment to ease back into one’s daily life for shopping habits.

But, E-Commerce

The thing is, though, there’s still a really big chance these surcharges are going to hit consumers hard as too much advancement has been made in the technological infrastructure of a cashless society — namely the rise of e-commerce. Consumers today have taken to shopping online, and all of those sales utilize a credit card. A Rasmussen Reports poll in April 2012 showed that 43% of Americans said they have gone through a full week without paying for anything in cash or coins. And The Official Merchant Services Blog has reported avidly on how pervasive and commonplace online shopping has become for the typical U.S. Consumer. A move back to cash may simply not be all that effective now that people are used to the convenience and control that online shopping — and mobile shopping — provides.

Don’t Forget Durbin

This decision is the second major event concerning limitations placed on swipe fees in credit card processing. Last year the Durbin Amendment to the Dodd-Frank Act took effect. This amendment placed a hard cap on debit card swipe fees. And it’s affect is still rippling through the payment processing industry as big banks, the credit card associations, and processors all try to figure out ways to recoup the billions of dollars in projected losses that stem from having the swipe fee capped at 24 cents or so.

The one thing we can learn from the Durbin Amendment, however, is that the use of convenient swiping that debit cards provide has not been ground to a halt by Durbin, and e-commerce is still booming. It seems unlikely that this settlement concerning credit card swipe fees will curb the growth of e-commerce to the point where we take a huge step back into a cash-filled society.

HostingCon2012 is in full swing, and Host Merchant Services is in the thick of the action. Here’s a picture from today:

That’s our very own dynamic duo Ken and Justin Hemmel working the booth with our partner OpenSRS.

This partnership — which began in April — brings Host Merchant Services, the premier provider of payment processing and e-commerce services for small businesses and medium businesses, to OpenSRS Offers, the platform that allows OpenSRS Resellers to extend valuable third-party offers and discounts to their customers.

The partnership is bolstered by HMS’ experience with the web hosting industry and HostingCon is a perfect venue for the company to present its ongoing initiative to provide E-Commerce focused companies a robust solution for processing credit cards online.

“We don’t write a business off as high risk just because it sells its products or services online,” says Host Merchant Services CEO Lou Honick. “HMS understands the needs of e-commerce merchants and works tirelessly to provide them with the right services at the best possible rate.”

Also, don’t forget that Honick will participate in a panel discussion on the topic of Best Practices for Payment Processing at 9 a.m. on Wednesday July 18. The panel offers hosting providers tactics for reducing payment processing costs and reducing risk. Honick is part of a panel of payment processing industry experts addressing the conference.

This is the latest installment in The Official Merchant Services Blog’s Knowledge Base effort. Well we want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’ we’re going to break from the norm, and provide a definition for a term from the web hosting industry: Cloud Hosting. We’re breaking from the norm for two reasons.

First, Host Merchant Services is at HostingCon 2012 this week. Second, Cloud Hosting is an integral aspect of the future of E-Commerce, something Host Merchant Services specializes in.

Cloud Hosting

Cloud Hosting is a type of hosting platform that allows customers powerful, scalable and reliable hosting based on clustered load-balanced servers and utility billing. Web hosting services allow individuals and organizations to make their website accessible via the World Wide Web.

Web hosts are companies that provide space on a server owned or leased for use by clients, as well as providing Internet connectivity, typically in adata center. Web hosts can also provide data center space and connectivity to the Internet for other servers located in their data center, called colocation. Host Merchant Services CEO Lou Honick — who is speaking at HostingCon 2012 this year — founded and ran a successful Web Hosting company prior to beginning his credit card processing venture with HMS. This experience gives HMS an edge in terms of understanding the needs of E-Commerce merchants.

Cloud hosting gets its name from the use of a cloud-shaped symbol as an abstraction for the complex infrastructure it contains in system diagrams. Cloud hosting entrusts its data, software and computation over a network — the cloud.

A cloud hosted website can be more reliable than alternatives since other computers in the cloud can compensate when a single piece of hardware goes down. Also, local power disruptions or even natural disasters are less problematic for cloud hosted sites, as cloud hosting is decentralized. Cloud hosting also allows providers to charge users only for resources consumed by the user, rather than a flat fee for the amount the user expects they will use, or a fixed cost upfront hardware investment. Alternatively, the lack of centralization may give users less control on where their data is located which could be a problem for users with data security or privacy concerns.

HostingCon 2012 is right around the corner. And The Official Merchant Services Blog is pleased to announce that Host Merchant Services CEO Lou Honick will be there to participate in a panel discussion on the topic of Best Practices for Payment Processing. The discussion, scheduled for 9 a.m. Wednesday July 18, offers hosting providers tactics for reducing payment processing costs and reducing risk. Honick is part of a panel of payment processing industry experts addressing the conference.

“As a three-time keynote panelist, I’m excited to return as a speaker this year,” said Honick of his speaking engagement. “Panel discussions at HostingCon have been consistently excellent at packing a high level of knowledge and experience into a single session. Having been the CEO of a hosting company for 11 years, and now at the helm of Host Merchant Services for three years, I’m able to bring a great perspective on best practices for credit card processing in hosted services.”

HostingCon, celebrating its 8th anniversary, is the foremost conference and trade show for the hosted services industry. The best and the brightest from the industry will be attending the event from July 16 – 18 at the John B. Hynes Veterans Memorial Convention Center in Boston, MA.

“As a specialist in partnering with web hosting companies, I’m glad to share my experiences from both sides of the table to help attendees reduce costs, decrease fraud, comply with regulations, and maintain security.”

Host Merchant Services specializes in providing world-class customer service and support to its credit card processing customers. The company takes a different approach to merchant services, focusing on delivering the industry’s lowest processing rates while providing industry-leading service and support. Host Merchant Services, headquartered in Newark, Delaware, specializes in partnering with web hosting and other professional services companies to offer payment processing to their customers.

This approach stems from Honick’s experience in the web hosting industry. Honick got his start in the hosting industry as the founder of HostMySite.com, growing it from a two person operation in 1997, to an industry leader with 240 employees and over 100,000 customers at the time it was acquired by a private equity firm in June of 2008. He transferred the same successful approach to the credit card processing industry when he began Host Merchant Services in 2009.

To learn more about HostingCon 2012 visit their website.

Host Merchant Services will also be there in force to promote their special offer program with partner OpenSRS. OpenSRS partnered with Host Merchant Services back in April.

This partnership brings Host Merchant Services, the premier provider of payment processing and e-commerce services for small businesses and medium businesses, to OpenSRS Offers, the platform that allows OpenSRS Resellers to extend valuable third-party offers and discounts to their customers.

The partnership is bolstered by HMS’ experience with the web hosting industry and HostingCon is a perfect venue for the company to present its ongoing initiative to provide E-Commerce focused companies a robust solution for processing credit cards online.

“We don’t write a business off as high risk just because it sells its products or services online,” added Honick. “HMS understands the needs of e-commerce merchants and works tirelessly to provide them with the right services at the best possible rate.”

Today The Official Merchant Services Blog wants to review the details of VISA’s newFixed Acquirer Network Fee (FANF). On April 1, 2012, Visa began charging this new fee. But it has taken about this long for it to catch up to merchants and their statements. The process sort of knocked its way down like dominoes falling — The fees went in effect in April, but were based on May’s activity, so didn’t show up until June’s statements, that many merchants are now noticing here in July.

These fees are new, and start to show up on statements where they hadn’t appeared before and they have the appearance of being hidden fees. This development goes against the Host Merchant Services policy of no hidden fees. Which is why we’ve attacked this story so vigorously in our blog, trying to keep our readership up to date on these new card association fees affecting the credit card processing industry.

The HMS Guarantee

Host Merchant Services wants to assure its customers that it sticks by its guarantee. HMS will never increase their fees for their customers. HMS continues to offer the guaranteed lowest rate. And that rate is frozen. Unfortunately, Card Association Fees are new, and are not part of any current pricing model. They are also mandated and initiated by the credit card companies themselves — Visa, MasterCard and Discover. All processors everywhere will be adding them to their pricing structure. So your statement will start showing new fees moving forward. But we here at Host Merchant Services will help explain what they are, where they come from and why they’re just now appearing on your statement. So please feel free to contact us if you have any questions about your statement.

Now About Those Fees

FANF is the most high profile of the new fees. But it’s name is a bit misapplied, as the fee itself is not “fixed” in any sense of the word. The FANF is a monthly fee that will affect all merchants to a varying degree. For card present businesses like retailers, the amount of the Fixed Acquirer Network Fee will be based on the number of locations a business has. For card not present businesses like e-commerce operations, the FANF will be based on gross Visa processing volume. So the “Fixed” fee’s actual amount varies based on multiple factors. Those variables are:

Merchant Category Code (MCC)

The merchant category code used to classify a business plays a role in the amount of the FANF charged each month. However, the impact of the MCC is very minimal, amounting to a difference of $0.90 – $1.10 for most businesses (less than fifty locations).

Acceptance Method

The main factor in determining the amount of the FANF is whether a business processes the majority of its transactions in a card present or card not present environment.

Card Present Businesses

(Excluding Fast Food Restaurants / MCC 5814) The amount of the Fixed Acquirer Network Fee for card present businesses will be based number of locations. Businesses with one location will be charged $2 – $2.90 a month, up to $85 a month for businesses with 4,000 or more locations.

Card-Not-Present Businesses

(As well as Fast Food Restaurants / MCC 5814) For card-not-present businesses, the amount of the FANF will be based on gross Visa processing volume. Card-not-present businesses will see a greater impact from the FANF than card-present businesses due to the fee being determined by volume.

For example: card-not-present business processing between $8,000 and $39,999 will be hit with a Fixed Acquirer Network Fee of $15 a month opposed to just $2 for a card present business with similar volume and one location.

Other Fees

Besides FANF, Visa also is implementing a Transaction Integrity Fee and making revisions to its Network Acquirer Processing Fee. Visa’s Transaction Integrity Fee is a new $0.10 fee that will apply to U.S. domestic regulated and non-regulated purchase transactions made with a Visa Debit card or Visa Prepaid card that fail or do not request Custom Payment Service (CPS) qualification. On the other hand, the Network Acquirer Processing Fee on Visa-branded signature debit will be reduced — going from $0.0195 per authorization to $0.0155 per authorization. The fee for credit card authorization will remain $0.0195 per authorization.

Facebook defended its program and its protocols in response to Limited’s claims. The company has said it is investigating the claims that Limited has made, and noted that it has defenses in place for such kind of fraud. A fake click, Facebook said, would come from a fake account, which would be disabled immediately upon discovery.

Facebook defended its program and its protocols in response to Limited’s claims. The company has said it is investigating the claims that Limited has made, and noted that it has defenses in place for such kind of fraud. A fake click, Facebook said, would come from a fake account, which would be disabled immediately upon discovery. In May we learned that the breach might have actually

In May we learned that the breach might have actually

That first bullet point is good for the credit card processing industry as it allows merchants to feel more in control of their business and lets

That first bullet point is good for the credit card processing industry as it allows merchants to feel more in control of their business and lets  This decision is the second major event concerning limitations placed on swipe fees in credit card processing. Last year

This decision is the second major event concerning limitations placed on swipe fees in credit card processing. Last year

Host Merchant Services specializes in providing world-class customer service and support to its credit card processing customers. The company takes a different approach to merchant services, focusing on delivering the industry’s lowest processing rates while providing industry-leading service and support. Host Merchant Services, headquartered in Newark, Delaware, specializes in

Host Merchant Services specializes in providing world-class customer service and support to its credit card processing customers. The company takes a different approach to merchant services, focusing on delivering the industry’s lowest processing rates while providing industry-leading service and support. Host Merchant Services, headquartered in Newark, Delaware, specializes in

{kind=link}