This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. We want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: we deliver personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access.

Today we will take another look at international processing, and the fees associated with accepting an international card. Yesterday we defined the MasterCard Cross Border Fee, and today we will explain the Visa International Service Assessment.

Visa implemented an international service assessment (ISA) fee of 40 basis points (0.40%) in April of 2008. This fee applies to all transactions involving a U.S. based business and a credit or debit card issued outside of the U.S. The ISA is also separate from interchange rates and from Visa’s standard assessment fee, which is currently 11 basis points (0.11%).

For example, the ISA fee of 0.40% will be added to a transaction where a customer uses a Visa-branded card issued out of the United States to buy something here in Delaware.

The ISA is one of two fees Visa currently charges for international card usage, the other is the International Acquirer Fee, a separate 45 basis point fee (0.45%), which applies under the exact same circumstances as the ISA. Visa began charging the IAF in October 2009.

The total fees Visa charges for a transaction involving an international card processed in the U.S. is the sum of the ISA fee (0.40%), the Visa standard assessment (0.11%), and the International Acquirer Fee (0.45%), which comes to almost a full percent above interchange, 96 basis points (0.96%).

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. We want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: we deliver personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access.

Today we will define the MasterCard Cross Border Fee. MasterCard charges an additional fee to merchants for all transactions acquired in the United States that involve a credit or debit card issued outside of the United States. For example, if a cardholder uses a Canadian-issued MasterCard to make a purchase from a business here in Delaware, that merchant will be assessed a cross border fee for accepting an international card.

Introduced in 2006 by MasterCard, the fee was originally 10 basis points. Since then, it has been raised to 30 basis points in 2007, and then to the current level of 40 basis points in 2008. The cross border fee is initially charged to acquirers, who then pass the fee on to merchants.

If the transaction is settled in U.S. dollars, the cross border fee is 40 basis points (0.40%) above the interchange rate for that card. If settled in a foreign currency however, the fee is increased to 80 basis points (0.80%). This fee, along with MasterCard’s acquirer program support fee, are the only two volume-based fees that MasterCard charges on transactions involving credit cards issued in another region than where they are acquired.

It’s been a little while since the Official Merchant Services Blog touched on the increasingly sensitive topic of the Credit Card Interchange Settlement. We first talked about the possibility of ‘The Big Cash Comeback’ when the settlement was first announced, and later we discussed the opposition to the settlement.

Seven years after the first lawsuits were actually filed against the bank card networks and some leading banks, a tentative settlement was reached on July 13 of this year. The agreement has had many mixed reviews, and some big name retailers have come out against it, including most recently the National Retailers Foundation, the nations largest retail trade association. The NRF’s members operate 3.6 million stores nationwide, however the organization itself is not involved in the lawsuit, which includes individual and class merchants as well as trade-group plaintiffs.

Under the proposal, the main defendants, Visa and MasterCard will pay $6.6 billion in damages and temporarily reduce interchange rates to save merchants another $1.2 billion. Merchants also will get greater freedom to surcharge card transactions and could form bargaining groups to negotiate interchange with the networks. In return, the networks will be freed from future legal challenges from merchants regarding interchange rates and merchant rules, even from merchants that didn’t participate in the current lawsuit.

I think the key points here are the temporary reduction of interchange rates as well as the fact that all merchants give up their rights to sue Visa and MasterCard upon accepting the settlement. Merchants will most certainly be satisfied by the reduction of interchange rates, but the drop will only be temporary. After a few months Visa and MasterCard will raise them again, and continue to collect outlandish fees for credit card transactions. Also, not every merchant is involved in this suit. I don’t think it’s a good deal for merchants to give up any of their rights, particularly the rights to any future litigation.

The National Association of Truck Stop Operators (NATSO) released a statement on Monday, announcing their dismissal of the settlement, “We joined this lawsuit in search of real reform to a broken system, one that is shielded from normal competitive forces. This proposed settlement does not achieve this goal. It lacks meaningful fixes to a system that allowed Visa and MasterCard to set artificially high swipe fees and provided retailers and consumers with no choice except to pay.”

This statement echo’s the cries of dissenters, who say the settlement protects the status quo more than anything, and will not change the way the networks set interchange.

In conclusion, the settlement still faces harsh criticism, and Visa and MasterCard have not had much to say to those who oppose it. Only time will tell if the plaintiffs decide to accept the deal, or push back for a settlement more in their favor. Host Merchant Services will keep you informed of all the latest news involving this legal battle between the merchants and the card-issuing giants.

Today the Official Merchant Services Blog will examine the PCI Security Standards Council’s most recent guidelines, and their slow crawl towards comprehensive security requirements for mobile devices.

On Thursday, the PCI Security Standards Council released a set of best practices geared toward software developers of mobile devices. These guidelines come four months after they released some guidance about mobile payments for small businesses.

The PCI Council, based in Wakefield Massachusetts administers the Payment Card Industry data-security standard and affiliated standards for secure payments software and also PIN-based transaction devices. The guidelines were released during the Council’s annual North American meeting in Orlando, Florida on Thursday, after hinting at a possible PCI clarification in early September. Present at the gathering were security assessors, merchants, processors and vendors, all preparing for the update of the main PCI standard next year.

The Council announced that it is starting to approve hardware for mobile payments such as card readers that plug into smart phones or tablet computers. The Council has not delved into the approval of software for mobile payments and have they made it clear when that will happen. They have however, announced that more guidance for merchants will come next year and that they will continue to take input from the payments industry on the serious task of protecting card holder data when payments originate from mobile devices.

Correcting software vulnerabilities is the most important aim of the Council’s new guidelines, as app developers crank out new programs for processing payments on smart phones and tablets everyday. The guidance covers everything from the payment transaction, access protection, and remote disablement of a missing device.

The last point is arguably the most important aspect of a new mobile PCI security system. Since mobile payments are true to their name, mobile, the chance of someone running away with your credit card terminal is an increasingly possible risk. The same applies for any tablets acting as POS systems in a store. An unlucky shopkeeper may open up in the morning only to find part of his or her POS system missing, and all cardholder data inside compromised. This is what the PCI Security Standards Council seeks to avoid.

Today The Official Merchant Services Blog gets extra visual with a step by step breakdown of how Credit Card Processing works.

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. We want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today we build off of our previous knowledge base entry on just credit cards. We noticed that we’ve been adding to this database for months now and kind of skipped over some of the most basic elements of the industry. So now that we’ve defined credit cards, we want to take you on a journey through credit card processing, detailing exactly how it happens.

CREDIT CARD PROCESSING

Host Merchant Services is able to guarantee its customers savings and the lowest rates possible. By understanding how credit card processing works, where the money gets made off of the transactions themselves and where those hidden fees actually are, you can gain some valuable insight into how Host Merchant Services is able to make its guarantee. Here’s a step-by-step breakdown that sheds light on where the fees from each transaction come from:

How Does Credit Card Processing Work?

The way credit card processing companies make money for themselves can sometimes be a confusing labyrinth where fees are hidden, percentages are tied to things not listed on statements and the deal you think you are getting isn’t the best deal you can actually get. Host Merchant Services is dedicated to giving its merchants the lowest price guaranteed, and the company strives to maintain transparency with no hidden fees. So take a walk with us and see behind the curtain as you learn exactly where the money is being made when you swipe a customer’s credit card.

Step One: A customer visits a store.

Step Two: Customer purchases $10 worth of merchandise.

Step Three: The customer swipes his credit card through a payment processing terminal such as a Hypercom T4205 from Equinox Payments to pay for the merchandise.

Step Four: The card reader recognizes who the customer is and contacts the bank that issued the credit card.

Step Five: The customer’s bank sends $10 to the merchant’s bank.

Step Six: Then the merchant’s bank deposits $9.80 to the merchant’s bank account.

Step Seven: That remaining 20 cents, a 2% fee, is taken from the $10 and given to the customer’s bank.

Step Eight: The customer’s bank then splits the 20 cents with the credit card company.*

* Depending on the specific company, country and merchant, the percentage can range from 1% to 6%. The amount the bank gets and the amount Visa gets is a negotiated deal. Also, Visa and MasterCard charge the banks an annual fee to be a part of their network in the first place.

Where The Money Gets Made

Credit Card Companies make money in a variety of ways. Here are the four most common:

One: The most common way credit card companies make money is through fees, such as the annual fee, overlimit fee and past due fees.

Two: Another way credit card companies make money is through interest on revolving loans if the card balance is not paid in full each month.

Three: As explained above, the card issuer (the bank that issued the card and/or the issuer network, be it Visa, MasterCard, Discover) makes a percentage of each item you purchase from a merchant who accepts your credit card. The rates range from 1% to 6% for each purchase.

Four: The card issuer can also make money through ancillary avenues, such as selling your name to a mailing list or selling advertisements along with your monthly billing statement.

SOURCE: Information for this article was gathered from www.creditscore.net, the movie Superman III, Wikipedia and Authorize.net.

Welcome to The Official Merchant Services Blog’sKnowledge Base effort. We want to bring clarity to the payment processing industry’s terms and buzzwords. We want to remove any and all confusion merchants might have about the industry. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today we decided to get as basic as possible. Our term is credit card. No, really, credit card. We noticed that we’ve been adding to this database for months now and kind of skipped over the most basic element of the industry.

Credit card processing hinges on the use of credit cards. So, without further hullabaloo:

Credit Card

A credit card is a payment card issued to users as a system of payment. It allows the cardholder to pay for goods and services based on the holder’s promise to pay for them. The issuer of the card creates a revolving account and grants a line of credit to the consumer (or the user) from which the user can borrow money for payment to a merchant or as a cash advance to the user.

Credit cards are issued by a credit card issuer, such as a bank or credit union, after an account has been approved by the credit provider, after which cardholders can use it to make purchases at merchants accepting that card. Merchants often advertise which cards they accept by displaying acceptance marks – generally on stickers depicting the various logos for credit card companies like Visa, MasterCard and Discover. Sometimes the merchant may skip the display and just communicate directly with the consumer,saying things like “We take Discover” or “We don’t take credit cards”.

When a purchase is made, the credit card user agrees to pay the card issuer. The cardholder indicates consent to pay by signing a receipt with a record of the card details and indicating the amount to be paid or by entering apersonal identification number (PIN). Also, many merchants now accept verbal authorizations via telephone and electronic authorization using the Internet, known as a card not present transaction (CNP).

Electronic verification systems allow merchants to verify in a few seconds that the card is valid and the credit card customer has sufficient credit to cover the purchase, allowing the verification to happen at time of purchase. The verification is performed using a credit card payment terminal or point-of-sale (POS) system with a communications link to the merchant’s acquiring bank. Data from the card is obtained from a magnetic stripe or chip on the card; the latter system is implemented as an EMV card. For card not present transactions where the card is not shown (e.g., e-commerce, mail order, and telephone sales), merchants additionally verify that the customer is in physical possession of the card and is the authorized user by asking for information such as the security code printed on the back of the card.

Each month, the credit card user is sent a statement indicating the purchases undertaken with the card, any outstanding fees, and the total amount owed. After receiving the statement, the cardholder may dispute any charges that he or she thinks are incorrect. The cardholder must pay a defined minimum portion of the amount owed by a due date, or may choose to pay a higher amount up to the entire amount owed which may be greater than the amount billed. The credit issuer charges interest on the unpaid balance if the billed amount is not paid in full (typically at a much higher rate than most other forms of debt). In addition, if the credit card user fails to make at least the minimum payment by the due date, the issuer may impose penalties on the user.

Merchants

For merchants, a credit card transaction is often more secure than other forms of payment, because the issuing bank commits to pay the merchant the moment the transaction is authorized, regardless of whether the consumer defaults on the credit card payment. In most cases, cards are even more secure than cash, because they discourage theft by the merchant’s employees and reduce the amount of cash on the premises. Finally, credit cards reduce the back office expense of processing checks/cash and transporting them to the bank.

For each purchase, the bank charges the merchant a commission (discount fee) for this service and there may be a certain delay before the agreed payment is received by the merchant. The commission is often a percentage of the transaction amount, plus a fixed fee (interchange rate). In addition, a merchant may be penalized or have their ability to receive payment using that credit card restricted if there are too many cancellations or reversals of charges as a result of disputes. Some small merchants require credit purchases to have a minimum amount to compensate for the transaction costs.

Costs to merchants

Merchants are charged several fees for accepting credit cards. The merchant is usually charged a commission of around 1 to 3 percent of the value of each transaction paid for by credit card. The merchant may also pay a variable charge, called an interchange rate, for each transaction.

Merchants must also satisfy data security compliance standards which are highly technical and complicated. In many cases, there is a delay of several days before funds are deposited into a merchant’s bank account. Because credit card fee structures are very complicated, smaller merchants are at a disadvantage to analyze and predict fees.

Finally, merchants assume the risk of chargebacks by consumers.

I’m back to once again speak about Mobile Payments and their presence in Delaware. In case you missed my last blog, it’s here. It’s really finally here. Barclaycard Mobile Wallet is an active program that participating merchants at the waterfront in Wilmington, DE, and along Main Street in Newark, are using. Right now you can use your phone to buy stuff!

So that’s exactly what I did. I set out to visit some shops and buy some stuff. To give this test run some authenticity, I decided to try and buy things I actually needed. Let’s see how the process works and how useful it is for real-time shopping!

But first, I needed to update my settings. After downloading the application, and adding a credit card to my account, I had noticed I wasn’t seeing any offers. Kara from Barclaycard saw my blog and reached out to help me.

So I needed to add another step in our process for getting the technology up and running. It may seem like a bit much at first, but trust me, it’s fast and easy to initialize.

Kara noted that I needed to add locations to my account to get the offers to show up. ZIP codes are the easiest way to do that. Wilmington’s ZIP is 19801, and Newark’s is 19711.

The Revised Set of Steps

So now, our updated steps to bring the power of mobile purchases right to your hot hands look like this:

Step 1: Visit this site and register for an account. This is key. You can’t just download the app and go. You need to register online first. Since you’re here online reading this blog, you can take a moment to click that link and get that out of the way.

Step 2: You go through the process of setting up an account. Choose a username, password, give your information.

Step 3: You add the card you want the wallet to charge.

Step 4: You can then download the app from the app store or google play store.

Step 5: Activate the app on your phone, and go through the log in process. You’ll be asked for your passcode, and to log in with your username and password, and even one of the additional security questions.

Step 6: Go to settings — the gear icon — and go to offer locations. Add locations. Use the ZIP code that works best for you (I used both). Then you go to …

Step 7: BOOM! Start buying stuff!

The Buying Stuff Part

Thanks to Kara’s timely advice, I had offers streaming through my phone immediately. Armed with mobile purchasing power and enthusiastic curiosity, I leapt from my centralized blogging and news update headquarters — taking this story live and direct to the macadam of Main Street Newark.

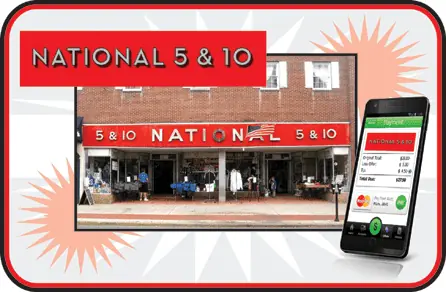

My first target was National 5 and 10, located on 66 E. Main Street. Boasting the world’s largest selection and lowest prices for University of Delaware merchandise, I decided to zero in on … art supplies. I needed a sketch book and a new pencil and eraser set to continue to design and draw projects like this more than I needed a new Blue Hens ball cap.

So I went to work racking up an impressive spree of supplies:

Mechanical Pencil with lead refills, 0.5 mm fine point lead size. For the nitty gritty line work.

Hi-Polymer Pentel white plastic art eraser. Because they take the pencil marks away but leave the ink behind.

5.5 x 8.5″ sketchbook, to help me rough out all my creative ideas.

And to get my purchase up over $10, four 5 x 9″ bubble mailer envelopes, so I can send slick prints of my best portfolio pieces to people interested.

Total: $11.24

I took this stash of artistic loot to the one counter that was open. When it was my turn I happily stepped up and asked if I could purchase these with the Barclaycard app, and flashed my phone at the cashier. This caused quite a stir, as it seems I was the very first customer to utilize this technology. Excitement buzzed in the air. We moved this transaction over to the other side of the area where the Barclaycard Mobile Wallet Terminal was kept. Another cashier took over the transaction, but a crowd began to form. The owner came over to see this landmark purchase of a pencil, eraser, sketchbook and some envelopes take place. Customers took notice. And then it happened.

The cashier rang up the items. I had my phone out and the app open. I was prompted to scan the QR Code on the terminal. The app took over and in a flash my payment was recorded. I approved it with the click of a button. The cashier printed out my receipt and just like that it was over. Payment made. Stuff bought. Once the wow factor wears off, the process will turn out to be very easy. As fast as swiping a credit card, with none of the hassle of keeping a card on you in your wallet. Mobile wallet finally lives up to the hype. I take my phone everywhere, as do most people. I need it for emergencies — but also to keep up with work and friends while on the go. So tucking this payment power into it just consolidates everything, making shopping a seamless part of the package.

But Wait, There’s More

I made the effort to obtain a purchase of $10 or more to take advantage of the offer I saw on my screen. But it didn’t seem to take. Later in the day I found out the offer might not be live yet. So I moved on to my next stop: Switch Skateboarding, located on 54 E. Main Street. No worries here about finding an item over $10 in price, but there were no visible offers for Switch anyways, so I put that out of my mind and focused on finding something I actually needed — wrist guards.

I haven’t been on a skateboard since I was 15 years old. But I’ve needed items that Switch sells almost regularly for the past four years because I’m a roller derby referee. I picked up a pair of Destroyer wrist guards. I chose them primarily because I already have a pair of 187 wrist guards and an old pair of pro-tec, so wanted to see if these fit any more comfortably. They cost $17.

Once again I stepped up to the counter and announced my intention to purchase this item with the Barclaycard app. There was decidedly less of a fuss about it as the staff at Switch seemed to be both more chilled out in general and ready to handle the unusual request. However, just like at National 5 and 10, there was a swapping of cashiers in terms of who handled the transaction. Switch uses a different setup than 5 and 10. The skateboard shop is working a completely virtual system, running transactions through a computer. The payment seemed even more seamless than at 5 and 10. All that was involved was opening up their gateway in their browser, inputting the details of the transaction, scanning the item’s barcode and then it was up to me. Switch has a static, standing QR Code on a card atop its counter. I had my app open and ready. When prompted I clicked the button and my phone scanned the barcode. Once again it was lightning fast. And after clicking my approval of the sale, the transaction ended.

Success. I was now armed with a fully operational mobile payment telephone, a pair of brand new wrist guards and some art supplies that I needed. This took the idea of buying things with a wave of my phone from concept to cold, hard reality. I found myself wanting to do this everywhere.

The Only Downside

As far as I was concerned I came away from this excursion with only one negative — there just wasn’t enough visible presence to let consumers know this existed. At 5 and 10, I created a crowd, but I knew going into the store I could buy things this way. The terminal itself stands out as it is different from other terminals. But I wonder if it’s all that visible since it’s not exactly a place where consumers actually look. I’m reminded of the time I spend standing in line at places like Wawa or 7-11, where I’d really like to just swipe my phone and go. I don’t even look at the terminal until I have to. How do you let people know they can do this now? Do you start to ask them, “Credit, Debit or Mobile?”

Or do you just get the word out there with more and more buzz, like this blog or a demonstration in the store at key high traffic times? Do I just keep telling my friends, “Hey, check out what I can do?”

It’s probably a mixture of all of those ideas. The technology is now here. It works. And it’s very easy to use. The ball is rolling. It just needs to pick up speed and add more snowy mass as it rolls along.

Today the Official Merchant Services Blog, along with the rest of the world, will take a look at the new iPhone 5 being debuted in California today. Specifically, we will look at one of the new iOS 6 features called Passbook.

Passbook is a new app, exclusive to iOS 6, the feature lets users store and quickly retrieve electronic versions of tickets, boarding passes and merchant cards all in one place according to executives at the WWDC 2012 today.

The app aims to replace almost all paper tickets, coupons and plastic gift cards that might be taking up space in a user’s wallet. Apple already has partnerships with a number of airlines, retailers and venues including Virgin Air, Delta, and Starwood Hotels.

In a demo, senior Vice President of iPhone software Scott Forstall showed how to use the app with a San Francisco Giants baseball ticket. The feature will also work with Starbucks and Apple Store gift cards. Adding to its already intriguing features, the app is dynamic, so users will be notified of any flight delays or gate changes. Users can also be alerted when near a movie theater that they have tickets to or rewards points that can be redeemed.

The app uses a special QR code that can be scanned by the participating retailer to redeem that ticket or coupon. Done with a particular card in Passbook? A virtual shredder “shreds” it on screen.

Is it a mobile wallet?

Well no, Apple hasn’t announced any kind of payment feature yet for the Passbook app, but don’t rule that out just yet. With the migration towards digitizing all of this info, as well as the time and location based triggers that give you what you need, when you need it this app is the one to watch in the festival of new software coming out of Cupertino, CA.

Passbook will roll out along side iOS 6 on September 19th, and the iPhone 5 will be begin shipping September 21st. As usual, we here at Host Merchant Services will keep you updated with all of the breaking news in the mobile payments world.

This is the latest installment in The Official Merchant Services Blog’sKnowledge Base effort. We want to make the payment processing industry’s terms and buzzwords clear. We want to remove any and all confusion merchants might have about how the industry works. Host Merchant Services promises: the company delivers personal service and clarity. So we’re going to take some time to explain how everything works. This ongoing series is where we define industry related terms and slowly build up a knowledge base and as we get more and more of these completed, we’ll collect them in our resource archive for quick and easy access. Today’s term is the Address Verification System, or AVS.

The system was designed by card issuers to aid in the detection of suspicious credit card transaction activity, and verify that the cardholder’s address info matches what the banks have on file. The service is provided as part of a credit card authorization for mail order/telephone order transactions (MOTO) or Internet e-commerce transactions. A code is received with an authorization result that determines the level of accuracy of the address match. This verification helps secure the most favorable interchange rates for the merchant.

Visa, MasterCard, Discover, and American Express support this service, and when paired with a CVV confirmation the result is a secure, verified transaction. To verify a customer’s address, a merchant will need the cardholder’s billing ZIP code and the house or apartment number of the billing address. The merchant does not need to enter in the street, city or state of the cardholder. While AVS is not intended for use as absolute protection against suspicious transaction activity, it is an important step in securing non-face-to-face transactions. Host Merchant Services recommends to all merchants that they secure these types of orders with both AVS and CVV.

The Official Merchant Services Blog again looks into the mobile wallet world today, by introducing the new product from Visa, Inc. called V.me. Last week we discussed in detail the BarclayCard mobile wallet system, which has come here to Delaware at participating locations in Newark and Wilmington.

Visa plans to roll out its own version of a mobile wallet solution by the end of this year. Although the Card Issuer is the largest in the world, the entrance seems late in a game filled with tough competitors. Visa has been testing a beta of the program with five large online retailers. Buy.com, Bidz.com, Cooking.com, Modnique and PacSun are the retailers currently offering the e-commerce side of the service on their web sites. Customers have the option when checking out to sign up for the program, set up the account and add a card, all without leaving that merchant’s site. Buy.com went live with V.me first in May; the others followed suit a few months after.

The program will eventually allow mobile device users to pay for goods from participating merchants at physical locations, most likely by the end of 2012. V.me uses a ‘hybrid’ security system of the device’s secure element, as well as cloud servers to store customers’ card credentials. This technique is reportedly more secure than the Isis system of storing card information directly on a device’s SIM card. In August, Google decided to upgrade to a cloud based system of storing card data, however they kept reliance on the phone-based element to house a prepaid virtual card that initiates transactions and identifies users.

Visa will also include a location-based offers service with V.me, that will likely use geo-tagging to identify customers most visited locations, and market offers accordingly. Competitor Google Wallet, while nearly a year old, has struggled due to the reliance on NFC-based technology that is not wide spread enough yet. Other companies such as Apple Inc., and MasterCard have also announced their entrance into the mobile payment game. Apple, with its Passbook wallet feature expected in the new iOS 6 will feature QR code reading technology. MasterCard announced a mobile wallet program in May, called PayPass wallet service that claims to be open to third parties for development and flexible to a wide variety of payment brands.

In summary, Visa’s V.me is one of the mobile wallets that I’ll be eagerly waiting for, however it seems a long way off from implementation now. For Delawareans, Barclays’ Barclay Card Mobile Wallet app seems to be the only one to hit the ground running here in the First State. A watchful eye will be kept on this close race of Banks, Card Issuers and Credit Card Processors to see who will be the one to win Mobile Wallet Dominance.