It seems that the U.S. Food and Drug Administration (FDA) is finally beginning to crack down on the growing vape and e-cig industry, after it announced last year that all e-cigarettes and other vaping products will now be regulated in the same way as cigarettes are under the 2007 Family Smoking Prevention & Tobacco Control Act. The law now applies to all electronic nicotine delivery systems (ENDS) and other vapor-producing products, meaning that all retailers and manufacturers of these products must now meet certain regulations in order to sell their products.

By extending its authority over e-cigs and vape products, the FDA is forcing both retail and online merchants to incur many additional expenses related to bringing their business in line with the new regulations. As these regulations cover the manufacturing, labeling, marketing and advertising of any e-cig related products, the expenses tend to pile up quite quickly.

Unfortunately, the new FDA regulations have also led to MasterCard changing its policy concerning online merchants. Previously, all companies who sold tobacco and tobacco-related products were required to prove their legal compliance and pay a $500 yearly registration fee in order to accept credit cards. However, the revised policy means that all vape merchants who wish to accept MasterCard payments are required to pay this yearly fee. Worse still, it seems certain that Visa and American Express will soon follow suit.

What the New Regulations Mean for Your Vape Business

One of the biggest problems associated with the FDA regulations is that they will make it much harder for merchants to continue to accept Visa and MasterCard payments. While $1,000 in total yearly registration fees will definitely have a negative impact on your company’s bottom line, there are many hoops you’ll first need to jump through before you can even get to the registration process.

In order for a merchant to register with one of the credit card companies, they’ll need to make sure that all transactions are properly age-verified. This means restricting sales to anyone under the age of 18, and, for online merchants, ensuring that all products require a signature from a legal adult upon delivery. As well, merchants also need to obtain a letter from an attorney legally verifying that the business is in compliance with all state and federal regulations.

The problem is that even paying the registration fee doesn’t actually entitle you to accept credit card payments, as you’ll then need to find a credit card processor that’s willing to underwrite your business. Despite the work you’ve put in to become complaint, the credit card processor is the one who has the burden to prove it.

Unfortunately, many credit card processors are currently unwilling to take the risk that goes along with it, meaning many online retailers may be left without a way to accept online credit card payments or will be forced to pay much higher fees in order to do so. For this reason, the FDA regulations seem certain to have a major impact on the industry, both in the short and long term.

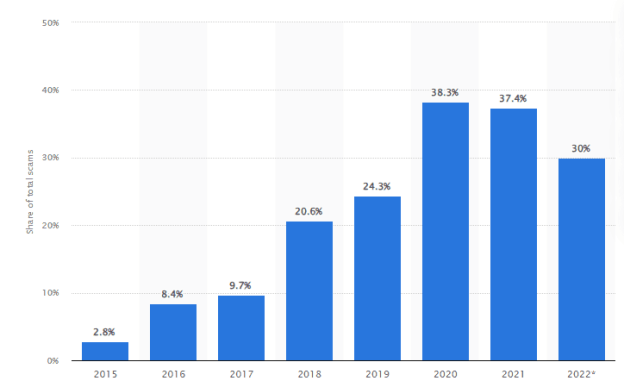

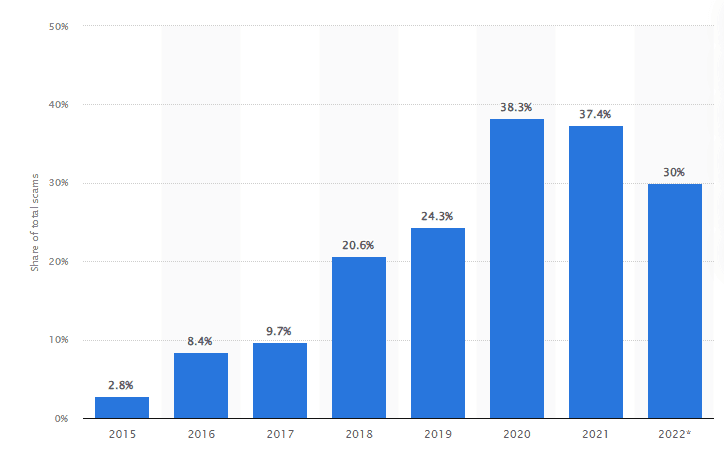

As online sales continue to trend up, there is an increased exposure to digital sales fraud specifically for card-not-present related fraud.

According to Forter, a fraud protection company, fraudulent activity accounts for about $11 of every $100 in digital sales nowadays. Fraudsters are remaining flexible in fighting the industry’s effort to stop these criminal acts. In response to changes in the marketplace, some of these criminals have found ways around the new mitigation techniques.

A large part of this trend is due to the introduction of EMV, which is the chip that most credit cards now have. On one hand, the chip has been successful in mitigating point-of-sale fraud in traditional brick-and-mortar stores. However, this has resulted in an upward trend for card-not-present issues for e-commerce merchants, resulting in an overall upward trend for digital sales fraud.

The hardest impacted segments of the market are the merchants who deliver digital products such as music, movies, and other on-demand content. This makes sense when you consider the nature of their business in which the consumer expects their product at the time of purchase. Digital goods merchants do not have the luxury of time to mitigate fraud on those transactions. This results in a significant amount of chargebacks. A whitepaper published by Javelin indicates that the amount of chargebacks that come from online transactions is almost triple that of in-person transactions.

Not only do merchants have to deal with the losses directly related to the transactions impacted by these types of criminal activity, but there is also the indirect cost of managing and mitigating fraudulent transactions. Based on Javelin’s whitepaper, fraudulent activity costs e-commerce merchants 7.9% of their revenue. The effort required to reduce and manage these effects accounts for a whopping 74% of fraud-related costs.

One thing is for certain if e-commerce merchants want to remain profitable, combating fraud-related activities will continue to be at the forefront of their operations. Fortunately, there are companies that specialize in this very thing, giving merchants an alternative to solving this in-house. This gives merchants the ability to focus on what they do best, sales.

What is Digital Sales Fraud?

Digital sales fraud encompasses fraudulent practices that occur in online transactions. It involves exploiting technology and digital platforms to deceive individuals or businesses resulting in financial loss compromised information or both. These scams manifest in ways, such, as websites, phishing emails, counterfeit goods, and identity theft.

One common form of fraud is called “phishing.” It happens when scammers send emails pretending to be companies to trick people into revealing sensitive information, like passwords or credit card numbers. Another type of fraud involves creating marketplaces where sellers advertise products at unbelievably low prices but never deliver them after receiving payment.

Scammers also employ tactics like creating replica websites that closely resemble well-known e-commerce sites but have variations in the URL. They may even use social engineering techniques to manipulate individuals into sharing information.

The consequences of falling prey to sales fraud can be severe. Not only can you lose your hard-earned money but your data may also end up in the wrong hands leading to identity theft or financial ruin.

To safeguard yourself against sales fraud it’s crucial to remain vigilant and skeptical when engaging in transactions. Exercise caution when sharing information and always verify the authenticity of a website before making a purchase. Watch out for warning signs such as bad grammar, website email addresses, and offers that seem too good to be true.

Types of Digital Sales Fraud

Digital sales fraud is a growing concern in today’s online world. As technology advances, so do the tactics used by scammers to deceive unsuspecting consumers. It is important to be aware of the different types of digital sales fraud so that you can protect yourself and your hard-earned money. Always remember, educating yourself is the best prevention from such frauds.

One of the most common types of digital sales fraud that you might also know is phishing scams. These are common globally. A fraudulent email or a website that resembles well-known brands are some of the most common ways fraudsters use to rob you. An individual is tricked either to spend money on the site or share his or her personal information. Personal information may include passwords, credit card details, or other types of personal information.

Another very common way of online sales fraud is by using counterfeit products. Ecommerce has grown exponentially over the years. Fraudsters use counterfeit products to lure people. These products are exact replicas of the original product and for a layman, it is difficult to differentiate. Usually, this type of fraud is done by launching a new eCommerce website where these products are sold. Once the fraudster generates the expected income the website is removed and it becomes difficult for the buyer to contact the seller.

Online auction fraud is also prevalent in the digital sales world. Scammers may create fake listings, bid on their items, or fail to deliver goods after receiving payment. To avoid falling victim to this type of fraud, research sellers thoroughly and read reviews from other buyers before participating in an online auction.

Identity theft scams are unfortunately common where criminals aim to steal information to commit fraud like opening credit card accounts or making transactions. To safeguard your information it’s crucial to use strong passwords and enable two-factor authentication whenever available. Regularly keep an eye on your financial statements for any signs of suspicious activity.

How to Spot and Avoid Digital Sales Fraud

The rise of digital technology has undoubtedly made our lives more convenient, but it has also given rise to a new kind of threat – digital sales fraud. As consumers increasingly turn to online platforms for their shopping needs, scammers have found new ways to exploit unsuspecting buyers. However, by staying vigilant and following a few simple tips, you can spot and avoid falling victim to digital sales fraud.

One telltale sign of potential fraud is when a deal seems too good to be true. If you come across an offer that promises unbelievable discounts or prices significantly lower than the market value, proceed with caution. Scammers often use these tactics to lure in victims and make quick profits.

Another red flag is poor website design or unprofessional appearance. Legitimate businesses usually invest in well-designed websites that are easy to navigate and provide clear information about their products or services. On the other hand, fraudulent websites may appear hastily put together with spelling errors or inconsistent branding.

It’s essential always to do your research before making a purchase from an unfamiliar seller or website. Look for customer reviews and ratings on independent review platforms or social media channels. If there is limited information available about the seller or numerous negative reviews, consider it a warning sign.

Additionally, pay attention to secure payment options provided by sellers. Reputable e-commerce platforms typically offer secure payment gateways such as PayPal that protect your financial information during transactions. Be cautious if a seller insists on alternative payment methods like wire transfers or cryptocurrency since these options are harder to trace if something goes wrong.

Furthermore, be wary of spammy emails or messages offering incredible deals from unknown sources—especially those requesting personal information such as passwords or credit card details through links embedded within them (phishing). Legitimate companies rarely ask for sensitive data via email and will usually direct you back to their official website for any account-related actions.

Conclusion

Digital sales fraud is a growing concern for businesses and consumers alike. With the increasing reliance on online transactions, it’s important to be aware of the various types of fraud that can occur and take steps to protect yourself.

By understanding what digital sales fraud is and being able to spot the warning signs, you can avoid becoming a victim. Remember to always research sellers before making a purchase, use secure payment methods, and be cautious of deals that seem too good to be true.

Additionally, staying informed about emerging trends in digital sales fraud can help you stay one step ahead of scammers. By following these tips and remaining vigilant, you can protect yourself from falling victim to digital sales fraud.

So next time you’re browsing online or making an e-commerce transaction, keep these tips in mind. Stay safe and enjoy your online shopping experience without worrying about falling prey to digital sales fraud!

The swipe fee antitrust lawsuit that The Official Merchant Services Blog has been covering for a few years now has an update: Wal-Mart, accusing Visa of excessively high card swipe fees, is suing Visa for $5 billion. The action by Wal-Mart is being taken because Wal Mart opted out of the settlement of the class action lawsuit between merchants and Visa and MasterCard.

This follows our previous report of the Minnesota Twins also opting out of the settlement. Wal-Mart filed the suit Tuesday, March 25, in the U.S. District Court for the Western District of Arkansas, where Wal-Mart is headquartered.

Wal-Mart’s Side of the Suit

Wal-Mart, the world’s largest retailer, is seeking damages from price fixing and other antitrust violations that it claims took place between January 1, 2004 and November 27, 2012.

In its lawsuit, Wal-Mart contends that Visa, in concert with banks, sought to prevent retailers from protecting themselves against those swipe fees, eventually hurting sales. Wal-Mart stated in court documents: “The anticompetitive conduct of Visa and the banks forced Wal-Mart to raise retail prices paid by its customers and/or reduce retail services provided to its customers as a means of offsetting some of the artificially inflated interchange fees. As a result, Wal-Mart’s retail sales were below what they would have been otherwise.”

Wal-Mart contends that that the way Visa set up the swipe fees violated antitrust regulations and generated more than $350 billion for card issuers over the time period in question, in part at the expense of the retailer and customers.

Case History

The antitrust case against Visa, MasterCard and several issuing banks stemmed from the dispute relating to the percentage of credit card transaction fees that retailers must remit to the credit card processing network. The fees generally range from 1.5 to 3 percent and are shared with the bank that issued the card. Also known as “swipe fees,” these charges serve to underwrite the supporting infrastructure that allows businesses to accept and process credit cards.

Large retailers and supporting associations have repeatedly complained about the costs associated with accepting credit cards and the fees for merchant services. These grievances resulted in a number of lawsuits filed in 2005, which were eventually consolidated into a single case known as the Payment Interchange Fee and Merchant Discount Antitrust Litigation.

There were 139 parties involved as plaintiffs, and the case was active for over eight years. In July 2012, a settlement was reached that provided $6 billion in damages to affected retailers and another $1.2 billion for a temporary reduction in interchange fees. As a further concession, Visa and MasterCard eliminated certain rules for merchant services that prohibited surcharging, which is a practice that allows retailers to recoup credit card costs by passing them on to the consumer.

After a settlement was reached in the case, major retailers such as Target, Nike, Home Depot, Lowes, Starbucks and Best Buy ultimately opted out of the settlement. Major trade organizations, including the National Restaurant Association (NRA), have voiced significant opposition to the agreement. In fact, the NRA strongly encouraged its constituent members to reject the settlement and highlighted the potential negative impact it could have on the emerging mobile payments market.

The Saga

To review the full extent of this ongoing saga, you can read our previous coverage of this settlement:

On Tuesday, February 25, 2014, Nevada and Delaware lawmakers signed a landmark agreement to join the states together in online poker ventures, potentially increasing payouts for residents who gamble online. The Multi-State Internet Gaming Agreement signed by Gov. Brian Sandoval of Nevada and Gov. Jack Markell of Delaware established a legal framework for the first authorized interstate Internet gambling.

The legislation opened up a landmark new initiative for the two states. Delaware officials supported this venture in the hope that revenues from online poker in Delaware, blackjack, and slots would help boost revenue in the state’s three brick-and-mortar casinos. Competition in those real-world casinos has risen significantly because of the appearance of new facilities in surrounding states. This increased competition has affected overall state revenues from gambling and prompted Delaware lawmakers to seek out other revenue streams like online gambling.

Nevada has three online poker websites: Ultimate Poker, which is owned by a subsidiary of Station Casinos; WSOP.com, which is aligned with the World Series of Poker; and Real Gaming, which is owned by South Point. Delaware’s websites are controlled by the state’s three racetrack casinos and run on 888’s platform.

The potential boost to Delaware’s economy from this move is unclear. Delaware officials predicted that online gambling would generate up to $5 million in state tax revenue in its first year. Those officials have since scaled back that forecast after some technical difficulties and slow take-up online.

Eilers Research gaming analyst Adam Krejcik told investors that Delaware’s current numbers “have been nothing short of a disaster.”

According to the Delaware Lottery, the state brought in $145,200 in revenue from online gaming in January, following $140,000 in December and $111,000 in November.

Nevada hasn’t broken out online poker revenues in the state’s monthly figures, but Union Gaming Group estimated the revenues were between $200,000 and $750,000 each month.

Online Poker in Delaware: Already Opposition

On top of the consternation over the economic impact of this partnership is mounting opposition to the law. On March 26, 2014 members of both parties in Congress supported a ban on online gambling. This bipartisan ban comes just mere months after Delaware’s online gambling system went live and a few short weeks after Delaware and Nevada signed The Multi-State Internet Gaming Agreement.

Both Republican and Democrat lawmakers introduced legislation in the House and Senate aimed at banning online gambling, setting the stage for a two-pronged battle in Congress. The measures are aimed at reversing a 2011 decision by Attorney General Eric Holder that a 1961 law used in recent years to curb Internet gaming only barred sports betting. The bills would broaden the prohibition to where it stood before Holder’s ruling.

The Other Shoe Drops

So after Delaware, New Jersey, and Nevada leaped into the space created by the Holder ruling, creating online gambling systems, both Delaware and Nevada teamed up to allow their customers to play against each other in a virtual environment. But before this entire endeavor really gets going, Congress is looking to ban it outright. One key component to why the customer interest is lackluster has to do with something extremely basic (and relevant to The Official Merchant Services Blog): Credit Card Acceptance!

According to uspoker.com, the lack of credit card acceptance is one of the biggest complaints about regulated online poker in Delaware, Nevada, and New Jersey. The Mastercard acceptance rate at regulated sites is higher than Visa, however, neither is high enough to be considered adequate for players and operators.

While this is all still new and getting off the ground, the trend in behavior shows at least one of the obstacles online gambling in Delaware faces. Regulated sites have higher fees, and that is there to help offset the risk of fraud. Essentially what happens with these kinds of sites is that they suffer from a much higher rate of chargebacks.

A chargeback typically refers to the act of returning funds to a consumer. The action is forcibly initiated by the issuing bank of the card used by a consumer to settle a debt. Essentially what happens is a consumer disputes a transaction, and the credit card company’s bank responds by taking the money back from the merchant and returning it to the consumer. Customers dispute charges to their credit card usually when goods or services are not delivered within the specified time frame, goods received are damaged, or the purchase was not authorized by the credit card holder — the latter being the most common reason for a chargeback. The chargeback mechanism exists primarily for consumer protection.

Now in online gambling, the risk of a chargeback happening is much higher. Customers who lose money will oftentimes initiate the chargeback instead of taking the loss.

Card issuers have the right to block any transaction that the company does not consider legitimate. Online gaming transactions, even if explicitly legal, sometimes fall into this category. Chargebacks are expensive for banks. These costs are passed onto merchants and processors in the form of penalties and higher processing fees. Banks loathe chargebacks and online gaming has been associated with too many of them over the years. This is one reason credit card companies are not quick to approve these transactions.

But regulation steps in and alleviates these fraud issues. All of the concern related to abusive chargebacks is resolved in regulated markets because players cannot easily charge back a credit card transaction. The transaction is coded as a legitimate, regulated purchase. Many are considered cash advances. The poker site can prove where the player was located at the time of the transaction and that the chips were received. Proper player verification also provides evidence that a charge was proper.

In Conclusion

The allure of online gambling is still high and Delaware is one of the states diving headfirst into the industry. But there are already obstacles facing the First State. A ban from Congress and all of the problems with chargebacks and fraud create a daunting road ahead for Delaware’s online gambling future. Teaming up with Nevada in a partnership to expand the competition was a good first step. But more states need to be involved if the fledgling endeavor is to really get going. That also helps with the fraud issues as it will take more states regulating online gaming to help make banks more comfortable with the industry. This will also help the profitability of processing these transactions.

Today marks the start of CoinSummit San Francisco, a two-day event ”connecting virtual currency entrepreneurs, angel and VC investors, hedge fund professionals and others who are looking to learn and network in the virtual currency industry.” CoinSummit will take place on March 25-26 2014 at the Yerba Buena Center for the Arts in San Francisco. Many in the bitcoin community have been waiting for this event for a while.

The event with feature notable entities in the virtual currency community that include Marc Andreessen of Andreessen Horowitz, Brian Armstrong of Coinbase, Nic Cary of Blockchain.info, and Tony Gallippi of BitPay.

The Official Merchant Services Blog has been tapped into the ongoing saga of Bitcoin since this article in November — delving into the fascinating gimmick of Bitcoin mining. Traversing the ups and downs of this unstable and chaotic currency led to the crazy month of February and then the fall of Mt. Gox. Since that fateful day, the virtual currency industry has been scrambling. And now we have this much anticipated summit of industry experts discussing the details and potential future of BitCoin and its competitors.

Don’t Miss a Moment of the Action

For those interested, a live stream of the event begins at 9 AM Eastern time today, and can be viewed here.

Points of Interest

So some of the things we’ll be hoping the Summit delves into are: The Mt. Gox crisis, its aftermath and the future of the currency exchange. Of course industry insiders are all going to be sharing their thoughts, rants and frustrations about MtGox. Many will be raging about the losses incurred by the public and so many bitcoiners, and how badly Mark Karpeles has handled this debacle. But more importantly the issue of malleability will be explained and also how the currency and its exchanges can survive well into the future.

Which leads right into the fact that the crisis didn’t imply a complete price crash for BTC, even after hundreds of millions of dollars in permanent losses. How will exchanges guaranty transparency? Audits? Open balance sheets? These are critical issues if Bitcoin is to be adopted by mass markets. So let’s hope the summit dives right into the answers for those questions.

And then there’s the heavyweight presence to consider. The “big 4″ (Coinbase, Blockchain.info, Bitstamp, and BitPay) will all be present at this summit through its founders. Let’s see if the industry leaders explain their current strategies and growth trends.

The competitors also have some spotlight. Ripple, DogeCoin, Litecoin, and Ethereum will be pitching the advantage of alternative options, but also talking about the future of Bitcoin through smart contracts and smart property, two functionalities many think will catapult BTC prices to new levels.

That’s a quick roundup of what to expect at CoinSummit San Francisco.

Sometimes the future just sort of sneaks up on you. Even if you’ve given yourself reminders, sticky notes, calendar alarms, and the proverbial string tied around your finger, the future still has a way of creeping up on you unawares.

Which is why Host Merchant Services is happy to offer its customers a payment processing terminal that comes with a reminder built in. Verifone with its VX 520 Terminal is here to prevent any memory lapses about the future from happening to your business and its PCI compliance needs. The VX 520 is PCI PTS 3.0 compliant right out of the box and is a forward thinking terminal designed specifically to be prepared for the PCI compliance mandates that are changing the rules of the industry.

Verifone terminals use end-to-end encryption with SSL v3.0 and 3DES to maintain the highest levels of security. This encryption, coupled with Master/Session and DUKPT key management, provide maximum protection from fraud and misuse of the terminal. The VX 520 terminal is also certified with PCI PED 2.0 approval.

All About Security

Security and secure transactions have been a hot button issue in the payments processing industry for the past few years. Everything from the Global Data Breach to Bitcoin to the Target Breach has people wondering about how secure their payment information really is. This is the root of the creation of PCI and its standards. In the ten years since the PCI DSS emerged as a consensus industry standard for the major credit card vendors, PCI DSS succeeded wildly in some areas – such as the use of endpoint security, encryption and network monitoring technology.

The Clock is Ticking

However, the success of PCI DSS in some areas highlighted others in which the standard had little to say or created perverse incentives—rewarding “compliance” over real security. Subsequent updates have attempted to right those wrongs. And the VX 520 is on the cutting edge of those PCI updates.

In January 2012 the PCI DSS released version 2.0 of their standards. And the VX 520 was built to be compliant to those standards and more.

In November 2013, the PCI DSS released version 3.0 of their standards. And again the VX 520 was compliant.

The 520, offered by Host Merchant Services, is a nimble processor that is ahead of the curve on security standardization. This is helpful because by December 2014, changes are coming from the credit card companies where older terminals will no longer be valid. Host Merchant Services offers a free terminal to new customers that sign up and are available 24x7x365 to help upgrade existing customers to terminals that will be PCI compliant.

Getting Secure and Staying Secure

Host Merchant Services knows that your business needs secure transactions to function. And we’re here to make the process of PCI Compliance easy, understandable and consistent for you each year. We offer the lowest PCI Compliance fee in the industry, at just $4.95 per month. PCI Compliance is essentially the process of adhering to the standards set forth by the Payment Card Industry Data Security Standards Council (PCI DSS). Essentially the standards are a set of requirements designed to ensure that all companies that process, store or transmit credit card information maintain a secure environment.

Secure transactions are important for merchants and a key element of the customer service Host Merchant Services provides. As part of our commitment to our Merchants and their transaction security, HMS offers a PCI ComplianceInitiative to anyone interested in processing with us. We are happy to offer this initiative as well as our free resources to help our merchants see what needs to be done to become compliant … and stay PCI compliant.

February was the month that the all-seeing eye of the media turned its lidless gaze upon Bitcoin and the craggy peaks of Mt. Gox, the Japanese Bitcoin exchange site. Almost half a billion dollars went missing from Mt. Gox, the exchange was rocked, Bitcoin was scorched, and the site went bankrupt.

The Official Merchant Services Blog has been tapped into the ongoing saga of Bitcoin since this article in November — delving into the fascinating gimmick of Bitcoin mining.

Wait, What is Bitcoin?

Bitcoin is a virtual currency introduced in 2008 by a programmer or group of programmers under the name Satoshi Nakamoto. It has no central issuing authority and uses a public ledger to verify encrypted transactions. The flashy shiny aspect of it is it’s a currency that can be bought, sold and mined electronically. The famous internet comic strip Penny Arcade defines Bitcoin for its readers here.

In 2013 the currency captured the imagination of the virtual and business worlds by soaring in value, rising from $10 to $1,200 per coin. It surpassed the value of gold at its peak. And then i crashed down to $500.

The currency was also embroiled in the huge Silk Road scandal as federal authorities seized millions of dollars worth of Bitcoins when it shut down the notorious black market web site the Silk Road.

The real trick of Bitcoin and why it’s so fascinating to payment processors is that it’s a cryptographic protocol, or crypto-currency. The protocol creates unique pieces of digital property that can be transferred from one person to another. It’s essentially the legitimization of microtransactions linked to actual monetary value. Each Bitcoin is defined by a public address and private key, both long strings of numbers and letters giving it a unique identity in virtual reality. In addition to its digital fingerprint, Bitcoins also have a place in a public ledger. This blockchain gives the Bitcoin a physical identity. So Bitcoins bridge the virtual and the physical.

Mt. Gox: Hackers Gonna Hack

But no matter how elegant and ingenious the actualization of Bitcoin is, the currency apparently can be hacked.

On February 25, Mt. Gox, the leading Bitcoin exchange located in Tokyo Japan shut down. It had discovered that hundreds of thousands of Bitcoins had gone missing, and more than $400 million had been stolen.

On February 28, Mt. Gox filed for bankruptcy and said it was under orders not to pay its debts. The exchange publicly apologized to users for “causing so much inconvenience.”

February was actually filled with problems for Mt. Gox and Bitcoin, as we reported previously.

Everything from Russia banning Bitcoins to China half embracing it just piled onto the Bitcoin craze. And then the hack and the bankruptcy happened. Since then, pieces of code showing parts of Mt. Gox’s Bitcoin source have cropped up around the web according to VentureBeat. Mt. Gox set up a phone support line but that got blitzed. Two other sites vied to fill the void of Mt. Gox, with BitStamp edging out BTC China for the title of largest Bitcoin exchange — for now. And then things got funny weird.

Virtual Theft

The authorities are now tasked with investigating the crime. And well, there’s this book, Halting State by Charles Stross, written in 2007. The premise of the book seemed so novel back then: A police officer is called to the offices of a big corporation because a robbery was reported. The robbery as it turns out took place in a virtual world, as the company runs a video game system with virtual currency. And then the novel goes on to explore technology, and how it is quickly evolving to affect the physical world from the virtual world. It was set just a few short years in the future.

And here we are, a few short years into the future, and authorities are investigating the theft of real value currency stolen from a virtual environment.

The amount of coins hacked and stolen from Mt. Gox amounts to about 6 percent of the entire Bitcoin market in circulation. And law enforcement is now tasked with trying to find the identity of the perpetrators — which may seem like an obvious and standard step in the investigative process. But it’s Bitcoin, which is famous for its anonymity and unregulated status. So authorities are filing subpoenas to Mt. Gox to gather information about how the virtual currency is transferred and converted into dollars. While stuck investigating even the basics of how the model works, authorities haven’t even gotten to the stickier situation of how Bitcoins are designed to be untraceable and finding the phantom thieves who stole the strings of encrypted numbers may not happen.

Leaving a half billion dollar hole in an industry that’s already proving to be volatile and susceptible to hacking.

Twitter, the modern equivalent of Mad Libs and the yellow journalism of the late 19th century, has revealed to us a gem of irony that makes the whole Target getting hacked story seem that much more poignant.

No one is safe in this bold new era of credit card hackers and identity thieves. Not even the president of a major payment processing company.

PayPal President David Marcus has been the victim of credit card fraud, he said on Monday. The leader of the online payments company revealed via Twitter that his credit card information had been stolen on a trip to the United Kingdom and he’d racked up a “ton” of fraudulent transactions on his account.

Smart Chip Didn’t Help

Marcus speculated that thieves probably skimmed the info from the magnetic stripe on his card, even though his card had an EMV chip, a technology that makes cards in Europe more secure than the ones commonly used in the U.S.

EMV® chip technology– or EMV — is a worldwide standard for credit and debit card payments based around the use of chip card technology. The acronym stands for Europay, MasterCard, and Visa, who collaborated to create the technology. The goal of this project was to create a card that worked based off of a microprocessor chip that is read by the payment terminal. Because the U.S. has yet to widely deploy embedded chip technology, the nation has increasingly become the focus of hackers seeking to steal such information. The stolen data can easily be turned into phony credit cards that are sold on black markets around the world.

Is it Just a Marketing Ploy?

Marcus adroitly used the incident as an opportunity to plug his own company, suggesting that the fraud wouldn’t have happened if the merchant had accepted PayPal. His company is currently trying to expand its presence as a payment option in physical stores, putting it in direct competition with platforms like Square and Google Wallet.

It also comes right when data breaches are major news in the payment processing industry. On December 19 2013, Target confirmed a sophisticated data breachoccured. In their press release they stated: “Approximately 40 million credit and debit card accounts may have been impacted between Nov. 27 and Dec. 15, 2013. Target alerted authorities and financial institutions immediately after it was made aware of the unauthorized access, and is putting all appropriate resources behind these efforts. Among other actions, Target is partnering with a leading third-party forensics firm to conduct a thorough investigation of the incident.”

So Marcus’ misfortune happens right at the time identity theft, credit card fraud and hackers are on everyone’s mind. With EMV chip cards being touted as one of the best solutions to the hacking problem, Marcus’ mishap even taps into that buzz.

It’s mid-February 2014. The Mid-Atlantic, homebase to Host Merchant Services, has been mired in a series of snowstorms that makes the jaunty tune of “Take Me Out To The Ballgame” seem months and months away. Yet today, February 12, is the day pitchers and catchers report for Philadelphia Phillies Spring Training 2014. Six days ago the first players of the season reported for the Arizona Diamonbacks. And 4 days from now, they will report for the Minnesota Twins.

Which means we’re closing in on a new season of baseball. More strike outs, more ground outs, more pop outs and even more home runs. A whole new season of visiting the ballpark and craving a hot dog. Or an ice cream sundae in a batting helmet cup. Or a brand new plastic batting helmet hat and foam finger combo to display your rabid fandom. All purchases you can make with plastic and one herculean, Casey-At-The-Bat swipe of said plastic right there at the ballpark.

But one of those major league baseball teams will be visiting the mound and facing a decision on how to proceed with the biggest ongoing lawsuit in the payment processing industry. The Minnesota Twins, according to the Star Tribune, enter the credit card swipe fee dispute after opting out of a class-action deal. The baseball team hopes to do better on its own than in a class-action settlement over credit card transaction fees.

What’s on Second?

The Twins are the latest business to sue MasterCard and Visa — the two dominant credit card networks — accusing them of breaking antitrust laws by fixing bloated fees that retailers have to pay to accept their customers’ credit cards. The antitrust case against Visa, MasterCard and several issuing banks stemmed from a dispute relating to the percentage of credit card transaction fees that retailers must remit to the credit card processing network. The fees generally range from 1.5-3 percent and are shared with the bank that issued the card.

The lawsuit settled in 2012 for a record $7.25 billion, with a federal judge ultimately approving $5.7 billion after thousands of dissatisfied retailers opted out of the damages portion of the deal. There were 139 parties involved as plaintiffs, and the case was active for over eight years. In July 2012, a settlement was reached that provided $6 billion in damages to affected retailers and another $1.2 billion for a temporary reduction in interchange fees. As a further concession, Visa and MasterCard eliminated certain rules for merchant services that prohibited surcharging, which is a practice that allows retailers to recoup credit card costs by passing them on to the consumer.

Arguing with the Ump

Almost immediately, opposition to the swipe fee settlement began to emerge. The primary objections centered on the belief that the agreement does not provide any meaningful reforms to the current model. Many merchants believe that market forces will not allow for credit card surcharges since consumers will object to the added fees. Other retailers oppose the stipulation in the agreement that prohibits future swipe fee lawsuits.

As a result, major retailers such as Target, Nike, Home Depot, Lowes, Starbucks and Best Buy ultimately opted out of the settlement. Major trade organizations, including the National Restaurant Association (NRA), have voiced significant opposition to the agreement. In fact, the NRA strongly encouraged its constituent members to reject the settlement and highlighted the potential negative impact it could have on the emerging mobile payments market.

Batting Clean Up

The Twins are part of a local group of Minneapolis opt-outs that includes Granite City Food & Brewery and JB Hudson Jewelers; they all filed their own lawsuit Feb. 7 in U.S. District Court in Brooklyn. The complaint doesn’t say how much the companies think they are owed.

Speaking to the Star Tribune, Twins spokesman Kevin Smith characterized the lawsuit as something of a technicality “to protect our interests.”

“Once we opted out, the legal system pushed the burden on us to move forward with obtaining a fair result,” Smith told the paper. “We’ll see what happens.”

Vincent Esades, the Minneapolis antitrust lawyer representing the group, told the Star Tribune the Twins are basically making the same case against Visa Inc. and MasterCard Inc. as the original antitrust class lawsuit. He estimated that “hundreds” of such cases have been filed in the wake of the settlement, but said he feels confident the group will get more in damages on their own than they would as part of the settlement.

Around the Horn

To review the full extent of this ongoing saga, you can read our previous coverage of this settlement:

Back in November, The Official Merchant Services Blog dove into the Bitcoin currency craze with an in-depth look at Bitcoin mining.

Bitcoin, introduced in 2008 by a programmer or group of programmers under the name Satoshi Nakamoto, has no central issuing authority and uses a public ledger to verify encrypted transactions. It is a virtual currency that can be bought, sold and mined electronically.

The Hammer is Dropped

We focused on the technological gimmick that is Bitcoin mining – essentially powering multiple computers to create the virtual currency from virtually nothing. The rest of the media since then has been concentrating on the other aspects of Bitcoin, including its use as a money laundering tool. In that same month of November, Federal prosecutors in New York filed charges against Ross William Ulbricht for running the Silk Road website, where customers allegedly used Bitcoins to buy and sell drugs.

And on February 9, Florida stepped into the spotlight concerning virtual currency and money laundering. Bitcoin traders. Florida prosecutors have charged three men, saying that their use of a site called localbitcoins.com violates laws against unlicensed money transmitters, according to a report in the Krebs on Security blog.

Bitcoin Banned in Russia

More bad news for Bitcoin came from Sochi Olympics host country Russia. The country banned Bitcoin altogether. Russia’s Prosecutor General’s Office recently made its stance on Bitcoin abundantly clear. “Systems for anonymous payments and cyber currencies that have gained considerable circulation — including the most well-known, Bitcoin — are money substitutes and cannot be used by individuals or legal entities,” the office said in a recent press release reported by Reuters. Any use of Bitcoin will be considered “potentially suspicious,” as the Russian government has linked Bitcoin usage to illicit activities.

Russia is only the latest country to release a statement detailing its position on Bitcoin. In early December, China barred financial institutions from using Bitcoin, though it didn’t ban the currency outright. In late January, Canada released a statement that said Bitcoin is not legal tender in the country. Countries like these have expressed skepticism in Bitcoin not only because of its links to money laundering, but also for its overall volatility.

Market Troubles

Bitcoin has plunged more than 8 per cent after a Tokyo-based exchange halted withdrawals of the digital currency, citing technical malfunction. Mt. Gox, a popular exchange for dollar-based trades, said in a blog post it needed to “temporarily pause on all withdrawal requests to obtain a clear technical view of the currency processes.”

It promised an “update” – not a reopening – on Monday, February 10, Japan time. Bitcoin exchange Mt. Gox said customers can take out cash “as normal” and it’s working to resolve technical issues that prompted it to halt withdrawals of the digital currency.

“It’s not about cash at all, only about Bitcoin,” Michael Keferl, a communications officer for Tokyo-based Mt. Gox, said. “There is a problem in the way transactions are verified.”

Things then rebounded. The price of Bitcoin rose 0.3 percent to $683.66 at 9:07 a.m. London time, according to the CoinDesk Bitcoin Price Index, which averages prices from exchanges including Mt. Gox.

Bitcoin App Dropped by Apple

On February 5, Apple struck a blow against Bitcon. The Blockchain app, downloaded 120,000 times during its two years in Apple’s iTunes App Store, was the most popular way for people and companies to transfer bitcoins from one another. Apple removed it from the store on February 5. Blockchain immediately shot back with a statement, accusing Apple of getting overly aggressive with future competitors. Apple is rumored to be developing its own mobile payment system.

And Speaking of …

With the crazy ups and downs of Bitcoin, one thing is undeniable: Virtual currency is a profitable new marketplace. Which means Apple isn’t the only group trying to develop their own alternative. An untraceable currency called Zerocoin is being designed by Johns Hopkins University researchers to compete with other virtual moneys such as Bitcoin. The researchers say that if virtual currencies are going to exist, there should be one that provides the same kind of privacy that people have when exchanging traditional forms of money.

What Does This all Mean?

The virtual currency movement has the potential to be the next stage in the evolution of payments and transaction processing.

Advocates say such digital currencies, made possible by complex computer formulas, will eventually be widely embraced by users who want to exchange money instantly and directly, without a bank as middleman.

While it may seem like the wild west in terms of security and long term viability, the concept of virtual currency is actually well in line with what we’re already surrounded with as consumers. By and large we continually swipe plastic through card readers when we buy everything from a coffee at Wawa to a down payment on a new automobile. So a paperless and coinless world is already one in which we exist. It’s not hard to envision a next step where the currency itself is virtual.

But that does leave security issues which are relevant and real. Relying on even the best encryption still leaves risk and susceptibility to fraud.

However, it seems governments are still playing catch up to the technology itself. Focusing on money laundering and the instability the anonymous exchange of currency brings to the banks themselves, as well as the sale of illegal goods and services. All of which are certainly part of their purview. It’s just a weird transition period as the infrastructure of the old school banking system doesn’t seem all that prepared to deal with the fluidity of a virtual currency snaking through the world’s consumers.

In short, it’s an interesting time to bear witness to the evolution of money and the marketplace. Governments will catch up with virtual currency. And consumers will embrace convenience more and more until we face a world that may actually give up on paper and coins completely, in favor of your PIN numbers and some encryption codes that store the value of you.