Today The Official Merchant Services Blog offers a really quick update on the fallout from The Durbin Amendment. You’ll recall Host Merchant Services offered a thorough analysis of the legislation before it took effect.

Much of the current media coverage for this topic revolves around something we predicted in that analysis: “The banks, not wanting to take a $9 to $10 billion dollar loss in revenues for the year, will simply add fees to other payment options or get rid of premiums and extras that they had been offering.” We also stated: “Higher fees on checking accounts and the removal of debit card rewards programs were suggested as a response banks would have.”

Banks Lead the Charge With New Fees

This article from twincities.com reports pretty much what we’ve been reporting about the response banks are having with the Durbin Amendment. The article, dubbing this strategy as Bank Fees 2.0, states: “Three months after banks scrapped plans for debit card fees, it’s becoming clearer how they intend to recoup money lost in the Dodd-Frank financial reform law. Instead of one new fee, prepare to be sold more products, offered new service packages, lose debit rewards and face more fees in general.”

This creditcards.org article reports the same: “So [the banks] enter 2012 chastened … and still facing a revenue gap. How are they going to make it up? In fees, of course! Just not the fees you were expecting. The Bank of America mess taught them a lesson; trying to unilaterally slap all their customers with a new fee is going to end badly, especially in the current climate, where the man on the street is hopping mad about big bank behavior. So instead, they’re going to be sneaky about it.”

The article then offers a checklist of fees that could be forthcoming.

Minimum Balance requirements to increase for formerly free services such as checking accounts.

Penalty fees to go up.

One-time service fees — such as for opening a safety deposit box, or taking out a money order — to go up.

And then finally The Baltimore Sun offered this article which states that banks plan to add a wide variety of fees to help offset the losses from the Durbin Amendment. The article states “There are nearly 50 different fees consumers can wind up paying, depending on the services they use and how they use them, according to some consumer advocates’ latest estimates.” The article then quotes Alex Matjanec, co-founder of MyBankTracker.com, a consumer-finance information website describing the fees, “Most of these fees are not the in-your-face charges, such as the debit-card fee that caused the big uproar. Many are flying under the radar. But they could have a big long-term effect on your money if you aren’t paying attention.”

The sneaky fees were something we covered in The Official Merchant Services Blog entry on November 16, 2011: “Banks are now going ninja style with their plan of action. Sneaky fees hidden and peppered about their services. All combining to help make up the ground they were going to lose. But most of them deposited around their whole suite of services that it is much harder to latch on like a pit bull and berate them for doing this.”

Big Bank, Big Losses

The losses that banks need to make up are starting to come in and be reported. It was predicted they would be in the billions, and the latest analysis of fourth quarter earnings reports state that right now it’s about $6 billion in loss. The two largest banks handling these types of transactions — Bank of America and Wells Fargo — equal roughly $800 million of that loss. Here is an infographic breaking down the four biggest banks and their fourth quarter losses from the Durbin Amendment cap:

We’ve been covering Mobile Payments here at The Official Merchant Services Blog since the very beginning. In fact, the Article Archive at Host Merchant Services has extensive coverage of the topic as well. It’s just too sexy a topic — everybody loves the allure of gadgets — and too fascinating a financial prediction — folks in the know are predicting Mobile Payments to boom in the billions between now and 2015-ish — to not continually cover Mobile Payments.

But I keep picturing a scene from the 1992 women’s sports movie A League of Their Own in my head every single time I look at the state of Mobile Payments in the U.S. The scene that resonates with me is the one where Marla Hooch— fearsome and uniquely striking power hitter for the team — is about to step into the batter’s box. But she’s getting confused. She steps into the box. Then back out of the box. The reason for her confusion? She’s getting contradictory signals from her Manager and her teammate. One wants her to swing away and unleash the fearsome potential of her staggering offense. The other wants her to play it safe and move the runner over for a better chance to score an efficient run. So there she goes, Marla Hooch, the powerhouse of the league. One foot in the box. Then out of the box. It’s the exact problem Mobile Payments currently faces. The power and potential of what it can do for commerce keeps getting highlighted in story after story, research after research. And then the biggest obstacle it faces keeps getting thrust in front of its face: Security.

Step Out of the Box

Google Wallet, one of the biggest lynchpins in the mobile payment industry’s bid to effectively take hold in the U.S. market was recently plagued by a security problem. This article from ExtremeTech notes the issues that happened to Google and its mobile payment system in a piece that discusses the pitfalls of its beta testing. A pair of bugs forced Google to shut down its pre-paid cards and Google Wallet took a huge hit on the nose in the press. This reinforced the public’s view that mobile payments are a bit scary because people think that their personal information — account numbers, social security information, credit card numbers — will get swiped from them out of thin air. The thought process being that if all they have to do to pay for an item is wave their phone in the air at a cash register, some sneaky net ninja can pluck the data right out of the very same air.

The article sums up the problem: “In the last week, there have been not one, but two exploits that could give a malicious individual access to your Google Wallet mobile payment app on Android. While the first is a root-only hack that Google couldn’t really be expected to plan for, the second affects all Android users and is simple to do.”

It goes on to suggest these bugs popped up due to a core problem with how google beta tests things.

Since that story broke, Google has gone on the offensive, and is now stating that the bugs are fixed. As this cnet article says: “Google has patched a hole in Google Wallet that could’ve allowed someone to access a user’s funds simply by resetting the PIN and using a prepaid card. The company said yesterday it has issued a fix that now prevents a prepaid card from being re-provisioned to another person. It has also restored the ability to issue new prepaid cards following a move on Monday to disable the use of such cards.”

These bugs were a major setback for more than just Google. The Mobile Payments landscape is bubbling with interest but it’s also saturated with variety. There are multiple avenues businesses are considering for their entry point into what research firms like Gartner predict will be big money very very soon. One of those avenues is Near Field Communication (NFC). The underlying technology of NFC is described as: “Near field communication (NFC) is a set of standards for smartphones and similar devices to establish radio communication with each other by touching them together or bringing them into close proximity, usually no more than a few centimetres. Present and anticipated applications include contactless transactions, data exchange, and simplified setup of more complex communications such as Wi-Fi. Communication is also possible between an NFC device and an unpowered NFC chip, called a “tag”.”

This is the technology that Google tagged to be their entry into Mobile Payments. And so these bugs are a major hit for Google and NFC as a whole, taking one of the most hyped aspects of Mobile Payments down a peg in the industry.

Step Into the Box

In the midst of NFC taking it on the chin, Visa and MasterCard unleashed its EMV initiative — as The Official Merchant Services Blog reported on February 7. This is, in my mind, the Mobile Payments Marla Hooch being told to step into the batter’s box and knock it out of the park. Visa is invested heavily into Mobile Payments, and is prepared to drag the industry kicking and screaming into the future of profits that are being predicted for Mobile Payments. The EMV initiative hinges on chip technology being attached to cards, and for Mobile Payment evolution also being attached to smart phones. What Visa’s investment in this avenue brings is added security. This is huge. The security advantage addresses the biggest fear people have for mobile payments. Visa, much like Tom Hanks, wants Marla Hooch to get in there and swing away.

Going Sci-Fi

This article from Asia One adds another wrinkle into payment processing, and possibly the future of mobile payments: Biometrics. The article cites The Monetary Association of Singapore (MAS) as researching ways to make Debit card transactions more secure. And one of the avenues of research has been biometrics. This could really lead to a breakthrough in the march towards a cashless society, including the use of smartphones for mobile payments. Having biometric security measures on your phone would work in tandem with the chip technology that Visa is pushing, making both the unit you use to store the information — your phone — attuned to your own physiology; and the transmission of your transactions — the swipe of said phone in the air — attuned to a secure chip. Identity thieves and card fraud masters would be stymied on multiple ends and have to work very hard to stay ahead of that security curve in their mission to steal your information and then your money.

The Bottom Line

So What’s Marla Hooch going to do? It looks like Google is sticking with its plan and dedication to NFC. They sort of have to due to how invested they are into the technology already. And it’s no secret that Visa is very much tied into the future of mobile payments, chip card technology, and payment processing security. Both entities are full steam ahead. And with that much tech and finance industry strength behind the initiatives, Mobile Payments will get its chance to swing for the fences. We look for the Google Bugs to blow over and not really hinder Mobile Payments growth much at all in 2012.

Today The Official Merchant Services Blog is turning its attention back to E-Commerce. Yesterday we delved into the topic of partial payment authorization, hopefully clearing up some of the more confusing aspects of the process. Now we’re going to take things back to the basics, and delve into the advantages of online processing, specifically focusing on the advantages that E-Commerce brings to your business.

Setting up a merchant account that allows you to process payments online opens up a whole new customer base for your business. By accepting credit and debit cards through an online shopping store you offer convenience to your current customers and opportunity for new customers — increasing sales and profits the entire time.

Partnerships That Count

We bring this up right now because Host Merchant Services just recently promoted its partnership program, which hinges on the customized E-Commerce solution package and the powerful online payment gateways the company offers online merchants. In particular, the company’s partnership with HostMySite.com — featured in a press release as well as an e-mail campaign from HostMySite — has underscored Host Merchant Services‘ dedication to making E-Commerce easy to use and profitable for its customers.

Host Merchant Services partners with online businesses to provide complete credit card processing and financial transaction services solutions for that merchant’s end-customers. HMS is the perfect partner to help integrate a fully customizable e-commerce solution that is tailored to the specific and variable needs of a web company’s customers. The partnership program splits into three tiers of focus: Web Hosting Companies, Web Designers and Website Owners. What this does is it lets the program be flexible according to the specific needs of the partner, but highlights the strength of the processing services offered to the end-user customer with the online shopping cart.

It all comes back to that: Online shopping. So, for example, the services being offered to a web hosting company provides extras that help their customers, who have their own websites with their own shopping carts, process transactions at a lower rate and with less hassles. Or, for example, with the website owner partnership the services go directly to that end-user and are tailored to their processing needs.

Set Up a Merchant Account

The first step an online merchant needs to take to launch a successful E-Commerce business is to open a Merchant Account with a credit card process, like Host Merchant Services. You can fill out this form and get the application process going quickly and smoothly. After you set up a merchant account, the next step is to get a payment gateway going.

Convenience is Key

One of the strengths of E-Commerce is that merchants can make sales from anywhere in the world. Online transactions don’t require you to have a physical terminal. You can use what is called a virtual terminal through your internet connection, giving you access to a payment gateway — and that’s it. You manage your sales through that and get your transactions done easily.

The goal is to find the gateway that works best for your business. Host Merchant Services offers a variety of payment gateway services which you can read about here. The Gateway essentially completes your website’s ability to allow visitors to shop on it. It takes the process from the point at which the customer clicks “buy now” or “check out” and allows customers to transmit their payment information safely and securely. The gateways also screen questionable transactions, and help reduce online fraud in the process.

What is a Payment Gateway?

A payment gateway is an e-commerce application that authorizes payments for e-businesses, online retailers, bricks and clicks, or traditional brick and mortar businesses. It is the virtual equivalent of a physical point of sale terminal located in most retail outlets. Payment gateways encrypt sensitive information, such as credit card numbers, to ensure that information passes securely between the customer and the merchant.

For more information on how Payment Gateways work, you can review this article and graphics series here which takes you on a step-by-step journey through the entire system.

Today The Official Merchant Services Blog is going to step off its SOPA soap box and return to a much more focused and specific topic — Partial Payment Authorization.

In November, 2011 Partial Payment Authorization was mandated by MasterCard and Discover. This mandate requires merchants to support partial payments on their terminals. Host Merchant Services reported on this mandate and you can read about it here in our Article Archive.

Pay Attention To The Purchase

We’re bringing this back up because there has been some confusion lately among merchants about this particular issue and this mandate. What keeps happening is that merchants are not noticing when the partial payment pops up on their terminal. This is a problem because of the way these payments function. If you do not notice that it is a partial payment and do not obtain the rest of the payment from the customer, they can walk out of your store with their purchase and you lose money.

So you need to really pay attention to the purchase. It will show up on your terminal screen. It will also show up on the receipt. Here is an example of what a receipt will look like:

In cases where only a partial authorization is returned, the merchant will need to collect another form of payment for the difference. In the instance where the cardholder does not have another form or payment to pay the difference or wants to use a different form of payment for the full amount, a real time partial authorization reversal must be performed in order to free up the funds that were previously held up by the authorization.

Host Merchant Services offers step-by-step guides on how to perform these real time partial authorization reversals.

The other area of confusion that seems to be cropping up with Partial Authorization is which businesses are affected by this mandate. Not all businesses are currently required to use Partial Authorization. However, there is a long list of businesses that are, and this list includes the most popular merchant codes. Here is the list:

To Recap

So just to review, Partial Payment Authorization is mandated by MasterCard and Discover. The listed businesses above are absolutely required to utilize it. It is easy to lose track of when these occur if you do not pay attention to the receipt or to your terminal when running the transaction through. The most common mistake is someone processing the transaction is in a rush and the receipt looks very similar to a normal, approved, full transaction when run through. Terminals do not have a sound or warning that this type of partial payment happened. So time and attention to detail are required for these payments moving forward. When a partial authorization happens you need to have your customer offer an alternate payment for the remainder of the transaction or you need to reverse the transaction right then and there.

For More Information

Host Merchant Services is available to walk any interested merchants through this process. You can contact us and we will be glad to explain how partial authorization works. Or you can take advantage of the materials we offer on this very website. To get more information regarding Partial Payment Authorization, you can:

This is part 2 of The Official Merchant Services Blog‘s rebuttal of this New York Times Op-Ed piece titled “What Wikipedia Won’t Tell You” written by Cary H. Sherman, chief executive of the Recording Industry Association of America, which represents music labels.

The Real Slim Shady

Mr. Sherman in his article goes on to accuse Wikipedia of spreading misinformation. He tries to find a smoking gun by suggesting the tech giants have an agenda of their own. He accuses them of bias in terms of the story they present, saying they are bending the truth and not being neutral. He even attacks media outlets that supported SOPA for not “taking advantage of their broadcast credibility to press their case.”

This is amazing. In a piece crafted specifically to present the RIAA’s very biased agenda that is featured in one of those media outlets thus stretching the New York Times’ already damaged credibility — lest we forget Zachary Kouwe, Maureen Dowd or Jayson Blair — Sherman accuses his opposition of doing the exact same thing he is doing. Keep in mind, his own executives were gloating about how well the music industry is doing in 2011. But here he is saying the industry is still being harmed by piracy and that Wikipedia is not telling you the whole story. Sherman simply seems to not be as familiar with how the internet works as his employee Duckworth is. To borrow the ever-popular phrase, he’s doing it wrong. He says, “Misinformation may be a dirty trick, but it works.” Not on the internet. People find you lying to them, or manipulating them, and they either make a mockery of you or turn you off. Sorry Mr. Sherman but in this instance, Citation Needed!

First World Problems

Mr. Sherman makes another fatal mistake with his article when he types: “The conventional wisdom is that the defeat of these bills shows the power of the digital commons. Sure, anybody could click on a link or tweet in outrage — but how many knew what they were supporting or opposing? Would they have cast their clicks if they knew they were supporting foreign criminals selling counterfeit pharmaceuticals to Americans? Was it SOPA they were opposed to, or censorship?”

Sherman is playing off of a stereotype about the twitter-age, or Net 2.0 –that everything is simplified and broken down into tiny bits of information. That the online citizen isn’t getting the full story is in fact that’s his main idea. But Sherman has forgotten net 1.0, and the strength of what Google, Wikipedia and all of that data really is. Somewhere between twitter campaigns with STOP SOPA avatars and Sherman’s own e-mail inbox is this huge collective database of information, which includes the exact language of the legislation as written. Every single piece Host Merchant Services has written on SOPA has included this link:

Many other articles that covered this topic throughout the past year have given links to all of the relevant data and text. It’s the internet Mr. Sherman. The information is just a click away. Many people not only had access to the bill, they also read it. And so their protest was based on the bill itself. Not on the oversimplification you suggest.

Young, Wild but Not Free

Mr. Sherman then takes a wild swing at all of the people who protested SOPA, suggesting some of them are criminals: “But others may simply believe that online music, books and movies should be free. And how many of those e-mails were from the same people who attacked the Web sites of the Department of Justice, the Motion Picture Association of America, my organization and others as retribution for the seizure of Megaupload, an international digital piracy operation? Indeed, it’s hackers like the group Anonymous that engage in real censorship when they stifle the speech of those with whom they disagree.”

So just because people don’t agree with your agenda, they’re hackers who support Megaupload and want free music? That’s the kind of rookie debate tactic that gets you ridiculed throughout the internet. It’s also misinformation and a huge distraction from the topic. The Megaupload arrest is separate from the SOPA debate. This is obvious. The arrest was made under the current law. The FBI was able to crack down on piracy using what is currently in place. That the federal government was able to successfully attack piracy under the laws currently in place would seem to weaken Sherman’s position. In fact data collected on the topic has shown that once the government moved past the Napster issue that Mr. Sherman was so quick to cry about in the opening portion of his article, piracy started to take a huge hit. In fact, that PDF from the IFPI has some compelling statistics about how much piracy dipped after Limewire was shut down. Apparently the current laws have a lot of teeth if law enforcement goes after the pirates and doesn’t waste time going after citizens or forcing search engines and payment network providers to police the internet.

U Jelly?

The last straw with Mr. Sherman’s terrible presentation of his organization’s biased agenda comes from his short and shallow rejection of the Online Protection and Enforcement of Digital Trade Act (OPEN). This bill was drafted as an alternative to SOPA and PIPA. This bill was, excuse the irony, carefully devised by tech industry experts in the government — with an eye toward attacking online piracy but closing the wide open holes that the previous bills contained. The Official Merchant Services Blog helped break this story back in early December, with this blog, where we stated: “A bipartisan group of lawmakers have come out in support of a new law that has been proposed as an alternative to SOPA. Under this proposed legislation, the U.S. International Trade Commission (ITC) would be given the power to investigate claims of copyright infringement on foreign websites. The proposal would also allow the ITC to issue cease-and-desist orders to foreign websites that willfully engage in copyright infringement. The lawmakers demonstrate some clever ingenuity here with this proposal by tapping the ITC for the job of piracy oversight. The ITC already investigates patent infringement complaints and can bar infringing products from being imported into the U.S.”

In short, OPEN is an alternative that was everything Sherman asked for in online piracy legislation that we never received with SOPA or PIPA. It was well researched. It deals with the issues. It has input from tech industry savvy and knowledgeable politicians that know what they’re doing. But Sherman’s misinformation sums up OPEN like this: “The diversionary bill that they drafted, the OPEN Act, would do little to stop the illegal behavior and would not establish a workable framework, standards or remedies. It has become clear that, at this point, neither SOPA, PIPA nor OPEN is a viable answer.”

Forget You

Again Sherman glossed over some important aspects of his own organization’s rhetoric. This article found at The Verge cites the RIAA’s opposition to OPEN and its support of SOPA. The article quotes RIAA Senior Executive VP Mitch Glazier as saying that the ITC “clearly does not operate on the short time frame necessary to be effective.” Glazer cites the delays in the RIM vs. Kodak case — filed in January 2010 but now expected to be ruled on in September 2012 — as a prime example. Glazier sees these delays as hugely damaging, saying that each day a piracy-facilitating website stays online can cost millions of dollars to “American companies, employees and economy,” and be “an ongoing threat to the security and safety of our citizens.”

So again, it’s a case of what Sherman isn’t telling you, while simultaneously suggesting it’s Wikipedia or Google that are obfuscating the issue. The biggest problem with SOPA and what helped get it killed in Congress was that it left things extremely wide open to interpretation. The biggest boon to OPEN is that it requires investigation. Yes, that absolutely does take time. Time needs to be taken. The RIAA doesn’t seem to care about the affects that can happen when a law goes into place allowing swift shut down of websites based on willy nilly complaints or the hidden agendas of competitors. In fact, this is what is wrong with the RIAA’s stance on piracy. They want what caused the protest in the first place. They want to be able to quickly shut down sites with little to no oversight on how the plug gets pulled. So when an alternative is proposed that works more at the a proper speed with investigation, careful consideration of the circumstances and oversight, the RIAA has to denounce that suggestion.

The RIAA keeps pushing for legislation that mirrors SOPA. In fact, this will be the third consecutive year that Senator Ron Wyden [D-OR] will defend our country against the immense loopholes and abusive traits that the RIAA crusades for — Wyden took a stand and singlehandedly curbed the Combat Online Infringement and Counterfeits Act of 2010 (S. 3804) in 2010, and then was at the forefront of halting PIPA this year in the senate. What Sherman is telling us isn’t anything revealing about Wikipedia. No. What Sherman is telling us is that no matter how many times the government tells him that these laws are poorly written and open for abuse, Sherman will keep pushing for this to go through.

Courage Wolf

Host Merchant Services and all other payment network providers have a vested interest in this legislation because they keep getting named in it. These laws keep coming up that require payment processors to be involved in the policing of online content. The issue is just as important to merchant services as the Durbin Amendment. And so The Official Merchant Services Blog is once again here to keep people informed about these developments. The RIAA is singing the same old song about Napster and Piracy trying to push some sympathetic buttons with the people, but at the same time attacking the overwhelming opposition to their agenda, calling them misinformed — and criminal. Suggesting that internet users don’t go beyond twitter messages in the depth of their awareness of issues that pertain directly to the future of their internet usage. And the entire time the RIAA is engaging in this shell-game of misinformation, they’re also gloating about how profitable they’ve been able to make digital music transactions. They claim they know the internet. But Mr. Sherman acts like he still thinks it’s a series of tubes. He might know it’s not a truck, but he’s still doing it wrong.

We’ll leave you with the same message we had days ago when Sherman’s employees were tweeting “DECLARE THAT!”

The bottom line is if Lady Gaga and Pitbull online sales are robust and legit, it’s probably time to back off the Online Piracy rhetoric.

The RIAA just won’t quit. They’re taken up the crusade to push for anti-piracy legislation once again, as seen in this New York Times Op-Ed piece titled “What Wikipedia Won’t Tell You” written by Cary H. Sherman,chief executive of the Recording Industry Association of America, which represents music labels. The content of the piece is incendiary, and that’s being kind. The RIAA is adamant about their stance on piracy and are pressing the issue in every outlet they can. To quote Digital Underground from their Sons of the P album — which currently is not available for legal purchase online due to holes in the DU library in various legit digital music resources — “Like Ice Cube says, Once Again it’s On.”

Everyday They’re Shufflin’

The Stop Online Piracy Act and the Protect Intellectual Property Act were both killed in Congress — shelved because they were too wide open to abuse. The protest against these bills reached a collective crescendo when internet giants Wikipedia and Google and WordPress teamed up with a host of others for an internet blackout. When the largest source of internet information — and grade school kids’ favorite spot for help with their homework — goes dark and the search engine juggernaut that fuels the internet shines its spotlight on your bill, things have finally gotten serious. The U.S. citizens took notice of this blackout, and joined the internet in protest. And Congress heard the people and backed off this poorly written legislation.

But that hasn’t stopped the entertainment lobby. They went back to the drawing board and then returned mere weeks later with a new idea on how to combat online piracy. Unfortunately that new idea was the exact same idea as before. This was seen in the wishlist the International Federation of the Phonographic Industry (IFPI) released. The highlights of this list are essentially that the music industry wants pretty much the exact same things that were in SOPA, the same things that prompted the protest in the first place. A list of seven demands, which include the exact same far reaching calls for search engines and payment processors to police websites individually and be responsible to law enforcement for content they are indirectly connected to.

We’ll get back to this, but for now the point is the music industry felt the need to push for the same stuff that killed SOPA and PIPA. And that came right back to the forefront with Mr. Sherman’s opinion article in the New York Times. Essentially the RIAA wants a do-over and Mr. Sherman is here to tell us why that needs to happen.

Come At Me Bro

So today The Official Merchant Services Blog is going to try to put this issue in its place much like Blake Griffin did to Kendrick Perkins recently. Yes, we are going to Posterize the RIAA. Because the op-ed article indicates the RIAA has soft interior defense and can’t play man to man very well at all. First up we’ll start with the relative hypocrisy of Sherman’s ill-timed article found in this contextual relationship: Suggesting Wikipedia isn’t telling people everything, and then making this comment, “They knew that music sales in the United States are less than half of what they were in 1999, when the file-sharing site Napster emerged, and that direct employment in the industry had fallen by more than half since then, to less than 10,000.”

This is hypocritical because Mr. Sherman is leaving out some very pertinent information — which his employees were just recently bragging about on twitter. As we reported on January 31, the RIAA was excited about the IFPI wishlist because it had a series of statistics that showed the music industry is doing well with digital sales. The music industry claims Wikipedia is being deceptive and then suggests that they are still reeling from Napster, which was effectively scuttled back in 2002. They’re making a play for sympathy from an issue that happened almost a full decade ago, and yet they just got finished gloating about how successful they were this year!

Jonathan Lamy, senior VP of Communications for the RIAA, tweeted that paid subscription services rose 65 percent to 13.4 million in 2011. This tweet was in response to figures released by the IFPI which Lamy was excited to read. Lamy also tweeted that paid digital music services are active in 58 countries, generating $5.2 billion in revenues.

And then Cara Duckworth. The VP of Communications for the RIAA also cited the IFPI figures and then said: “W/more than half of all music sales coming from digital services, we know how Internet works. “Music=Innovation. Declare THAT. #CES #SOPA.”

What the RIAA isn’t telling you is far worse than what Wikipedia isn’t telling you. But Mr. Sherman isn’t about to concede facts when the agenda needs to continue to be pushed. The music industry is finally getting the hang of the digital market. Their own people brag that they know how the internet works. Declare that! But Sherman’s still waving the Napster suit in your face trying to claim that Wikipedia is obfuscating the issue.

It gets worse.

Born This Way

Sherman writes, “While no legislation is perfect, the Protect Intellectual Property Act (or PIPA) was carefully devised, with nearly unanimous bipartisan support in the Senate, and its House counterpart, the Stop Online Piracy Act (or SOPA), was based on existing statutes and Supreme Court precedents.”

The only thing in that statement that is rooted in the reality of what happened with SOPA and PIPA is that there was a lot of bipartisan work. Unfortunately, the work was bipartisan unity on finding problems with the so-called carefully devised legislation. Tech industry experts on both sides of party lines found the problems and holes in the legislation. As we reported on December 27, 2011, SOPA sparked unity in the federal government. And as we’ve written in our in-depth analysis, the bill was not very carefully devised at all. In that analysis we lean heavily on discussion from Congresswoman Zoe Lofgren [D-CA], an expert in the tech industry. We’ll highlight just a bit of Lofgren’s criticism of this bill, with questions raised: “Section 103 also allows a “portion of” a website to be deemed “dedicated to the theft of U.S. property,” regardless of the culpability of the website as a whole. Like many important terms throughout H.R. 3261, the precise meaning of these words is ambiguous, and will require years of expensive litigation to clarify. However, the plain meaning of the words seems to indicate that any large website could face a risk of termination by payment and advertising providers based solely upon infringing material contained in a single web page. ”

This is not carefully devised legislation. And as we eventually reported, the bill’s own sponsor admitted he did not fully understand the technical aspect of the bill and he backed off of it. Bill sponsor Lamar Smith is quoted in various media sources as saying: “I have heard from the critics and I take seriously their concerns regarding proposed legislation to address the problem of online piracy. It is clear that we need to revisit the approach on how best to address the problem of foreign thieves that steal and sell American inventions and products.”

Today The Official Merchant Services Blog is going to give you a roundup of the latest news that is affecting merchants and payment processing. Our goal is to keep you informed and up to date on all the important news developments in the industry. Armed with that information you can make the decisions and the moves to keep your business ahead of the curve. The news roundup today focuses mainly on The Durbin Amendment and its continued impact on consumers, merchants and processors. The Durbin Amendment will continue to have a major impact on processing throughout 2012, and we’ll continue to keep you abreast of the topic.

Durbin Reactions

The first story we bring you is from the Los Angeles Times and it’s about the fallout from the Durbin Amendment. The article, found here, states that by the end of last year 610,000 U.S. bank customers switched to a switched to a smaller institution to protest plans by major banks to impose monthly charges for using debit cards. The article says the data was reported by Javelin Strategy & Research in a report and that the 610,000 figure represented 11% of the overall 5.6 million people who switched banks in that time period. The article also noted that: “In addition to the 11% who joined the Bank Transfer Day movement in October, November and December, an additional 26% told Javelin that they switched not as part of the protest movement per se but because the banks charged too many fees.”

Host Merchant Services Predictions Confirmed

The next news item we’re reporting is from The Denver Post. In this article the Post reports pretty much exactly what Host Merchant Services predicted would happen in its Durbin Amendment Analysis article.

The Denver Post writes: “Instead of one new fee, prepare to be sold more products, offered new services, lose rewards and face more fees in general.”

In the HMS Article from 2011, we wrote: “Merchants will end up having to shoulder the burden of the extreme cuts in revenue that this cap brings. Those who predict that merchants will end up worse off by the amendment suggest that the banks, not wanting to take a $9 to $10 billion dollar loss in revenues for the year, will simply add fees to other payment options or get rid of premiums and extras that they had been offering merchants prior to the cap being put in place.”

So essentially the Denver Post reports that the banking industry is reacting as expected to the Durbin Amendment. We even did an entire blog making the statement that the banking industry was going to go in stealth mode like a ninja.

The Denver Post article also gives a recounting of the tale of the Durbin Amendment as it took center stage in the media spotlight. This entire tale was chronicled as it happened by The Official Merchant Services Blog both in its Countdown to Durbin Series, as well as its ongoing Durbin Coverage after the October 1, 2011 date that saw the bill’s provisions begin. The Denver Post recap is succinct and states: “Several other banks already had either imposed debit card fees or were testing them, and analysts had predicted the trend would spread to the entire industry. But BofA’s plan, which leaked out at the end of September, produced an enormous surge of criticism. Protesters from the Occupy movement, consumer advocates and even President Obama questioned the move, and an online movement called Bank Transfer Day emerged to encourage people to switch to small banks and credit unions. Bank of America ultimately called off its plans without imposing the $5 charge, and the rest of the industry followed suit in allowing fee-free use of debit cards.“

Durbin Going Bye Bye?

The final piece of Durbin-related news comes to us from payment processing review site cardpaymentoptions.com. In this article, they give an extensive roundup of their predictions for 2012 — and one piece is sub-titled “Durbin May Get the Boot.” The article states the Durbin Amendment was originally designed to help merchants deal with high swipe debit card transaction fees, but now that it’s been in effect merchants are feeling the legislation has harmed them. The article specifically cites merchants getting hit with much higher for small ticket transactions — a noted loophole in the law that many media sources criticized while the amendment was still being discussed by Congress.

The article then makes this bold prediction: “Several retail organizations have brought suit against the Federal Reserve in order to repeal/modify the amendment and even the main author, Dick Durbin, has admitted the new law is flawed. With such disastrous results, merchants should expect to see the Durbin Amendment either repealed or greatly modified this year.”

The Official Merchant Services Blog has reported on a few of these suits as they’ve come up. And the backlash against Durbin has been significant. But with the election about to be in full swing it seems, to us at least, that the Durbin Amendment may continue to kick around for 2012. In fact, we’ve also reported that there is growing interest in a similar cap on credit card processing fees, swinging things even further in a direction that will burden consumers and incur ire with the banking industry. It just seems like it will be a lot more difficult to get rid of Durbin after it’s started and that the path of least resistance for Congress on this issue will be to continue to add to the law with more tweaks and changes, making it even murkier and over-legislated. That’s more the federal government’s style.

What do you think? Will 2012 see the end of the Durbin Amendment and the great experiment that was finance reform for payment processing fees? Or will the federal government just try to keep working with the law they have in place trying to smooth it out?

Today The Official Merchant Services Blog discusses a fascinating new development by Visa in the realm of credit card processing, security, and hopefully Mobile Payment Technology.

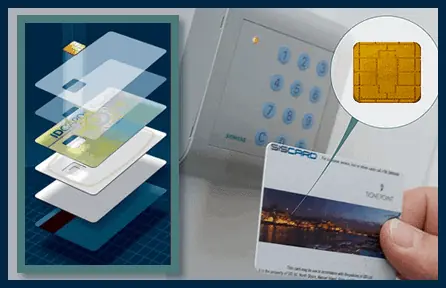

Smart cards have been slow in gaining traction, especially in the United States. But now Visa is making moves to drag the U.S. into the chip card realm, kicking and screaming if it has to. A recent article on Credit.com reveals as of December 31, 2011, Visa — the largest processor of both debit and credit card payments — had issued more than 1 million credit cards that use “chip” technology to sore consumer payment information. The article notes that this data is being announced rather quickly in relation to Visa’s August 2011 announcement that it planned to start issuing more EMV — Europay, Mastercard, Visa — smart cards to push the industry toward better security and an easier transition to mobile payments.

What is Smart Card Technology?

A smart card, or chip card, is any pocket-sized card with embedded integrated circuits. These cards contain volatile memory and microprocessor components, are made of plastic,and provide strong security authentication capabilities. Because of these characteristics, the technology is being utilized for credit cards by major card companies like Europay, MasterCard and Visa — garnering the nickname EMV. Visa has begun a major push of this technology because of the benefits the technology provides.

What are Those Benefits?

These kinds of smart cards can provide identification, authentication, data storage and application processing. A single contact/contactless smart card can be programmed with multiple banking credentials, medical entitlement, driver’s license/public transport entitlement, loyalty programs and club memberships to name just a few. Multi-factor and proximity authentication can and has been embedded into smart cards to increase the security of all services on the card. In one fell swoop, this technology can bridge the gap between card-swipe style processing and the mobile payment processing that the industry is striving to move toward. The technology lets virtual wallets and contactless payment happen, increasing convenience for consumers. And then it also boosts security, which is the largest concern consumers have with mobile payments.

The Credit.com article quotes Stephanie Ericksen, head of authentication product integration at Visa Inc. as saying “Migrating the U.S. market to chip will help build an infrastructure for accepting NFC mobile payments, enhance international acceptance and reduce fraud.”

TransFirst Sets Guidelines

TransFirst, Host Merchant Services’ acquirer and one of the premier providers of transaction processing services and payment processing technologies in the U.S., has issued a mandate in response to the EMV push. TransFirst says that Visa will require U.S. acquirer processors and sub-processor service providers to be able to support merchant acceptance of chip transactions no later than April 1, 2013. Visa also intends to institute a U.S. liability shift for domestic and cross-border counterfeit card-present point-of-sale transactions effective October 1, 2015, and for fuel-selling merchants by October 1, 2017.

Many of these dates are long-term projections and would seem to be a little far out there in comparison to the fast-paced results Visa is achieving already with their shift to chip cards.

The Carrot on the Stick

TransFirst explains that Liability Shift is often used as the incentive to encourage acquirers or issuers to move to chip transactions. For magnetic stripe swipe transactions, POS counterfeit fraud is mostly absorbed by the card issuers. But in the EMV shift Visa is pushing, the party that is not chip-capable will be liable for frauds that would have been prevented if the transaction were processed with a chip-on-chip connection.

It would seem that Visa is happy with the fast embracing of their chip transition but are still giving the acquirers and the merchant service providers and the merchants years to implement this fully before holding them liable.

In preparation for Visa’s Accelerated Chip Migration plan, TransFirst will migrate new terminal deployments on the following POS Terminals to chip capable versions of the same devices. Once implemented, non-chip capable versions of these terminals will no longer be available for purchase through TransFirst:

These new cards work in a similar fashion to the cards they are replacing. Users present them when making a purchase and from there the transaction follows the steps detailed in the Host Merchant Services Infographic found here. But the cards are different from swipe cards in some very important ways. Consumers do not swipe these cards. Instead they wave them over a sensor. This is the exact same style of payment that mobile phone based “virtual wallets” look to employ. You wave your smart card across a sensor, or you wave your smart phone across a sensor. Payment made. Visa also plans to allow chip cards to work with PIN codes, bringing debit under the umbrella.

The Mobile Payment Connection

Visa is heavily invested in the future of Mobile Payments. Which is not surprising as you can see from Host Merchant Services‘ coverage of the topic in its article archive. Past blogs have noted that the biggest obstacle Mobile Payments face with U.S. consumers is concern about the safety of the transactions. Visa’s hoping that the added security that the chip technology provides will overcome that obstacle and finally tap them into the billions of dollars of revenue that Mobile Payments are predicted to have in the coming years. As Ericksen says in the Credit.com article, “Since announcing our roadmap last year, we have seen strong interest among U.S. issuers large and small to invest in chip technology, as today’s milestone shows.”

Today The Official Merchant Services Blog is going to address an e-commerce issue that perhaps gets overlooked by a lot of merchants — effective design of your online shopping experience. Previously we offered a 2-part series on free, open source online shopping carts that are available. But just having the basic elements there for functionality is only part of the process. Your site should integrate e-commerce into its experience seamlessly so that visitors effortlessly make the transition from stopping by to actually purchasing.

Design plays a huge role in making this happen.

What is E-Commerce?

E-Commerce refers to the buying and selling of products or services over electronic systems such as the Internet and other computer networks. The term may also refer to the entire online process of developing, marketing, selling, delivering, servicing and paying for products and services. You can review a detailed explanation of E-Commerce in the Host Merchant Services Article Archive at this link here.

Why is E-Commerce Important?

E-Commerce is important because of how commonplace it has become in the daily lives of consumers. Shopping online has blossomed and grown in the past decade, and sales figures show that it is a standard. Merchants need to offer online shopping alternatives and can make quite a lot of profit by offering good online shopping solutions.

E-Commerce Tips

To assist merchants in making their e-commerce venture robust, well designed and profitable, we’re going to offer up a series of tips focused on improving e-commerce through strong design elements. Here’s our list of tips:

Navigation

Navigation is probably one of the most basic, and yet most often mangled aspect of strong e-commerce design. All online shopping sites have to allow their customers to navigate through the products to find the stuff the customer wants to buy. But so many sites out there have difficult or clunky navigation. Make sure your site offers a smooth, easy to navigate experience and you’ll get your customers clicking “purchase” much more frequently.

A Detailed Product Catalog

Tied right into navigation, is the single most important element merchants need to consider — the product catalog. This is what you are selling and it needs to be seamlessly incorporated into your website. Your product catalog needs to have detailed information about the products you are selling.

Database Search Capability

This is an extension of the previous element. If you have a large product catalog, then you need to offer your customers the ability to search through that catalog. Essentially you need to give your customers a database searching tool that will help them drilldown through your catalog to quickly find what products they are interested in.

Product Images

Your catalog needs to contain clean, easily readable images of the products. You should consider offering images from multiple angles — this is of course product dependent — so that your customers can feel safe that they are getting the most information possible about what they buy. One of the long-standing concerns about buying online is that customers feel like they’re being conned because they can’t view the product right there in front of them. Offering multiple angles can assuage some of those fears. Also you must balance the issue of image file size versus resolution and quality of image. You want to keep images small enough that they don’t distract from your catalog, but detailed enough that they give the customer a good look at what they’re buying. One solution that a lot of sites use these days is a Content Delivery Network (CDN).

Contact Information

Your E-Commerce solution needs to contain an easy to use, and easy to find, contact information area. Many sites make finding contact information a bit of a treasure hunt — sometimes requiring using the site map just like a treasure map. Keeping contact information visible and easy to use helps you with long-term customer service goals. And your contact information can also assist you in making sales. If a customer has special needs or requests involving a product they want to buy, they may need to contact your business directly. Making them hunt around for the ability to contact your business could cost you a sale.

Checkout Process

Integrating your online shopping cart into your site is extremely important. It was the primary reason we ran through our two-part series on open source shopping carts. Those 10 carts were advertised because of their cost efficiency (free) and because of their online support. Having a strong support community from an open source shopping cart gives you a safety net for things like your checkout process. Your checkout process needs to be smooth. It needs to be just a series of clicks and a small form (usually credit card information). Your customers want to click to purchase, click to confirm and get the shopping done. That’s the biggest draw of an online shopping cart — the internet makes it easy and convenient. So your checkout process needs to play on that, and get your customers through the checkout fields as easily as possible.

Payment Options

Building off of the checkout process, a good online shopping cart needs to present the various payment options to its customers in a clear, concise and easy to read manner. You want to offer your customers a variety of payment options. This includes all forms of credit and debit transactions, including gift card — even EBT where applicable. You want to make sure coupon codes and gift certificates are also shown clearly and have easy to use forms for completion. Merchant Services Providers, like Host Merchant Services, make it easy for merchants to offer any and all forms of payment for their online shopping cart. So it’s really just a matter of contacting your merchant services provider to make sure your e-commerce is customized to offer the maximum amount of payment options.

Related Products

This is an E-Commerce enhancement that helps improve your shopping experience. You an see this in a variety of forms. It can be something as simple as a list of products that fall under the same “category” your customer was searching, or as over the top as what Amazon does with its Customers Also Bought These Items lists that you get when shopping there. No matter what your approach, though, you should consider offering some type of related products feature in your online shopping cart. This helps establish return business in a very meaningful way as it gives customers targeted advertising to products they may also be interested in purchasing.

Shipping Rates Calculator

This should be standard on any and all e-commerce sites. Letting the customer control and maximize their shipping options directly will lead to more sales. Shipping costs have always been one of the biggest obstacles E-Commerce has faced, so making it transparent and giving customers the ability to reduce their costs manually helps keep them hooked on the potential sale of your product.

Store Policies

And last, but not least, try to make any and all relevant store policies displayed prominently on the site during the perusal and during the purchase portion of the experience. This includes things like return policies and refund policies. Be as up front about what it is you can and unfortunately can not do for your customers and your E-Commerce site will avoid some serious customer service headaches.

That’s just the basics of what The Official Merchant Services Blog suggests merchants do to make their E-Commerce and online shopping experience powerful and persuasive for their customers.

Today The Official Merchant Services Blog is here to talk about merchant accounts — specifically ways for business owners to maximize their usage of their merchant accounts.

The Basics

First we’ll address the most basic element of the topic: What is a merchant account?

A merchant account is a type of bank account that allows businesses to accept payments by debit or credit cards. A merchant account is established under an agreement between an merchant services provider, like Host Merchant Services, and a merchant acquiring bank for the settlement of credit card and/or debit card transactions.

Having a merchant account can really boost your business. It gives you more flexibility and lets you obtain revenue from a variety of sources consumers have for purchasing goods and services.

Payment Network Providers and Merchant Services Companies provide a wide variety of services. Host Merchant Services, for example, provides processing for retail merchants directly on their premisses. But HMS also provides e-commerce solutions in the form of online payment gateways — including Host Merchant Services’ very own HMSExpress — as well as mobile payment technology. Merchants have so many different options available to them that they can customize their merchant account to fit their flexible and ever-changing business needs.

Here’s a review of some of the most typical mistakes that business owners make with their merchant accounts, and a look at how Host Merchant Services Guarantee helps you avoid them.

Did Not Ask Questions

A lot of merchants are either lost in the details and fine print of payment processing or they are intimidated by the process and do not ask questions of their processor. Do not be intimidated. Always ask questions about your contract, your fees, your statement — everything. The jargon used in payment processing can sound like technobabble or biz-speak, so make sure you get all the clarification you need. High or hidden fees, bad service, long term contracts with hidden rules or steep penalties can have a negative impact on your business. So make sure you keep on top of the details.

Host Merchant Services provides a variety of online resources to keep merchants in the know.

They are always available to answer your questions and help guide you through the confusing maze that payment processing can be.

Lured in By Free Perks

Many processors offer perks, a common one being Free Equipment. This type of bonus is designed to get your attention, but many processors tack on hefty hidden fees to the deal, covering the cost of the freebie. The payment processing industry can be cutthroat at times and companies use aggressive tactics to board merchants. It’s very important for merchants to be aware of what they are signing up for and the true cost of the merchant services before they get locked into a bad deal.

Host Merchant Services offers a free equipment perk as part of its guarantee. The big difference with HMS and other processors is that HMS does not lock its customers into contracts. HMS also offers a transparent statement, with no hidden fees. The perk is exactly what it claims to be: Free Equipment. What you see is what you get.

Not Shopping Around

A lot of merchants find payment processing dense, sometimes confusing, and certainly a boring topic. So many of them will not comparison shop. This is a very big mistake. Take your time with offers and research the company pitching the offer to you. Read the fine print of each contract and see the differences in the numbers yourself.

Host Merchant Services offers a free statement analysis to every merchant they visit. HMS sales representatives will go over your statement, find the hidden fees and then go over step-by-step how the pricing structure HMS offers is different, and transparent. The HMS Guarantee even offers a free gift card if the company can’t save you money after the statement analysis.

The Cancellation Fee

Many merchants ignore or forget about the cancellation fee they face when changing payment processors. Cancellation fees are designed to keep a merchant locked into a contract. Some of these cancellation fees are exorbitant and restrict a merchant’s options. Some processors also tack on equipment fees for having to take back the used credit card processing terminal.

Host Merchant Services offers no cancellation fees. No fees for returning used equipment. And as part of the statement analysis and the sales pitch, the company takes any cancellation fees a merchant faces for switching into account and still finds a way to lower a merchant’s rates and save a merchant money.

Not Getting it in Writing

A salesperson in the ultra-competitive merchant services industry can sometimes make a pitch that sounds too good to be true. Always ask that salesperson to point it out in the contract they offer. In short, get it in writing. One common tactic merchants will find themselves being barraged with is a payment processor will offer a better specific rate. This shows up in Tiered Pricing models. But the way the pricing is structured, the reality is the merchant doesn’t get that savings when their monthly bill shows up. Some really bad examples will go a step further and hide the added fees, so the merchant won’t even know that they are being billed at a rate they weren’t quoted, because of the technical nitty gritty of the plan they signed up for. Hidden fees get abused quite a bit in situations like this.

Host Merchant Services adheres to no hidden fees. The company explains its pricing, and that’s the pricing you get. The company shows you your statement, goes over everything that is in writing and sees to it that you get exactly what you signed up for. It helps that the company utilizes the Interchange Plus pricing plan, which is far more transparent than the Tiered Pricing structure many other processors use.

The Official Merchant Services Blog ran a series on Tiered Pricing versus Interchange Plus Pricing back in 2011. You can review those blogs here and here and here.

That’s pretty much it in a nutshell. Merchants need to be focused and ask a lot of questions of their payment processor. If a merchant is relentless in their pursuit of understanding they will find that they can get quality processing with a good plan and great rates.