Credit Card Commerce Tips to Keep Debt Under Control

Credit cards get a bad reputation, but they can actually be quite a handy financial tool if used correctly. There is no reason to go into unmanageable debt using credit cards. The following credit card commerce tips can actually help you use them to build wealth rather than destroy it.

Choose the Right Card

Choosing the right card can be overwhelming, but it is worth it in the end. Be picky about terms and incentives to ensure the best possible product available. Cash back, points, fraud insurance, and low interest rates are all things that should be insisted upon. Those with great credit can get these things easily, while those without such great credit should start with the lowest limit possible, follow the rest of these tips, and work up to eligibility for great incentives.

Use them in the Right Places

One of the best credit card commerce tips available is to carefully choose when and where to use the card. Many merchants accept credit cards but as a general rule, buy only what can be paid off the next month. If you get cash back, it is not a bad idea to buy everyday items such as groceries, and even pay bills on the card. Just be certain to spend no more than you would have spent any way, and pay of the purchases immediately. Do not use them for luxuries that would not be purchased otherwise.

One exception to this rule is appliances. It is fine to purchase appliances on a credit card even if it cannot be paid off the next month. Often stores offer no interest for a period of time, so take advantage but be certain to pay it off in that time frame to avoid interest. Another perk for the purchase of big ticket items on credit cards is purchase protection. Check with the credit card company to determine what may be available.

Pay it Off

Though this is one of a couple of credit card commerce tips already mentioned, it bears its own discussion. Be ruthless when it comes to paying off purchases immediately. If an emergency purchase must be put on a card, then set a plan for paying it off. Divide the total into manageable monthly payments and make that payment each month until it can be paid off. Do not simply pay the minimum payment each month. If having the car repaired cost $1,000, and a manageable payment is $200 per month, then pay $200 each month until it is paid off regardless of what the minimum payment is.

Take Advantage of the Perks

If the perks are not automatically cashed in, such as air miles or points, be sure to use them. Use the air miles, free hotel rooms, and cash in those points for gift cards. If there are discounts, then take advantage of them by choosing the retailers where the discounts are available. Not doing so leaves money on the table.

Credit cards do not have to be bad. In fact, they can be very useful money management tools if these tips are followed.

As part of an ongoing series covering the basics of payment processing, The Official Merchant Services Blog is going to discuss Batch Processing today. You may have seen the term come up before –– possibly in reference to your statement or when your merchant account representative first met you.

What is Batch Processing?

Providing quick and efficient service is key to a successful enterprise. This is also applicable to the process of accepting credit card payments as processing your transactions quickly will also ensure prompt and timely receipt of payments for your products. And that’s where Batch Processing comes in.

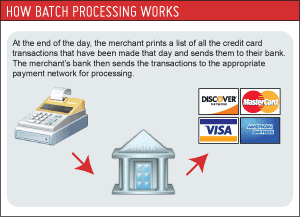

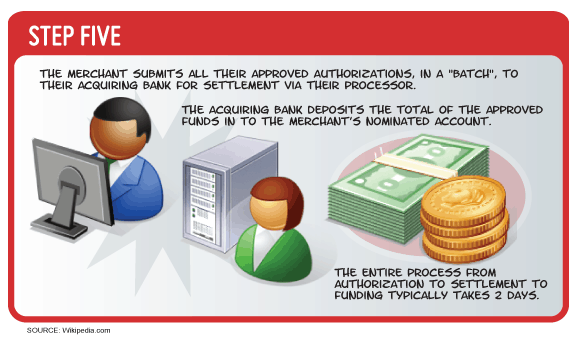

Batch processing is the mass processing of dozens of credit card transactions. It tends to be much more convenient to batch process hundred of orders at a certain time during the day, instead of each and every time they are received. A lot of merchants process their batch at the end of business. E-commerce businesses have batch processing built into their payment gateways. In fact, Step Five of our “How Payment Gateways Work” graphic details the daily “batch.” In fact, using a payment gateway will help simplify your batch credit card processing as it will help you coordinate the many functions that are necessary to process your payments. This form of card processing also has the benefit of being secure and this will certainly be a value added to your customer service.

How does Batch Processing Work?

Here’s an infographic that explains the batch process as it happens:

Batch credit card processing works well with small businesses where several credit card transactions are processed simultaneously, in the batch. With this, there is a definite lower risk of credit card fraud and you will be able to offer your customer and your business the assurance of transaction security.

The one con to Batch Processing

On occasions where there is a problem with the credit card payment, the seller may not know till the next day. Batches get processed with a lag. Host Merchant Services has 2 day processing. So there can be some issues with payments due to that lag. But the company has a qualified representative available 24 hours a day, 7 days a week, to help you with any issues you encounter in processing your transactions.

The Official Merchant Services Blog is here to share information with merchants to get them better prepared to understand how the payment processing industry works. This premise stems from Host Merchant Services and its philosophy to bring trust to the industry.

Payment processing can be confusing. And nowhere is that more evident than in a merchant’s processing statement. One of the ways some processors make their money is by hiding fees within the arcane labyrinth of a monthly statement, making the fees and the numbers difficult to understand.

Host Merchant Services believes that when one of its merchants receives their statement every month, that merchant should understand the items on the statement and that the fees should match what was promised in the sales process.

So in an attempt to help everyone understand that process better, The Official Merchant Services Blog is going to shine a spotlight on statements and see what there is to see.

What Is a Merchant Statement?

Every month, you receive a Merchant Statement from the company that processes your transactions. These transactions include Debit and Credit Card Transactions. This statement summarizes your net sales for all the cards that you process. It also provides your monthly transaction volume as well as provides you with an itemized list of your daily transactions. You can also see the majority of your debit and credit card processing fees. This is where we’re going to shine the spotlight, as this is where fees get hidden. Your fees on your statement include:

your transaction fee

your monthly discount rate for your Credit Cards

your monthly terminal fee (if you do not own your credit/debit card machine).

your Interchange charges

any chargebacks

third-party transactions

credit adjustments

The tricky part about these fees is that each company assembles their statement in a different way. Each payment processing provider has a unique statement layout structure, so most of the characteristics of the statement are the same but are put there in a different order. It forces merchants –– especially those who have used more than one processor in their time in business –– to do all of the eagle-eyed investigating themselves.

We’ll stick to the basics and then when that’s done, we’ll take a moment to explain why Host Merchant Services might be a little less confusing than other Payment Network Providers.

Card Deposit Summary

It’s pretty common for the Card Deposit Summary to be prominently displayed in a merchant statement. A lot of times it’s the first item a merchant will see on their statement. The phrasing may be a tad different –– perhaps it’s called a fund summary –– but for the most part it’s the opening line on each merchant services provider’s statement. The summary tends to include a laundry list of statement data, such as:

Amount of transactions incurred in that month

The dollar amount of those transactions

What credit cards were used

Any discount or coupon usage charges

Often this information is presented as individual daily line items, but some payment processors may combine all the data into one section.

Credit Card Fee Summaries

After the deposit summary information, most statements provide some sort of variation of how much the credit card issuer charged per transaction. This is usually called the Summary of Card Fees. As we explained in a previous blog series, a lot of payment processors offer a tiered pricing plan. And this is the section of the statement where you will see fees being charged for “qualified transactions.” That term specifically relates to your qualified tier in the pricing plan you signed up for. This section should include any fees, discounts and rates applied to transactions made through your merchant count. Most payment processors provide a complete list of card fee categories in this section, since qualified and non-qualified pricing tiers differ. Also included should be a listing for gross sales amounts per credit card and any fees and discounts applied to specific card transactions.

Transaction Fees

This section is an extension of the Summary of Card Fees section. This section lists each fee related to card transactions in dollar amounts. This can be a daunting section to sift through as the terminology used in this section is extensive. There is no shortage of card fee categories, and you’ll see chargebacks and batch header fees and ACH return fees mentioned here. This is why Host Merchant Services says payment processing can be confusing. The statements sometimes overwhelm merchants with tiny fees and cryptic buzzwords. Within that morass, the black hat companies will hide fees that some merchants aren’t aware they are paying or –– even worse –– aren’t aware they don’t even need to pay.

No Hidden Fees Guarantee

Now that some light has been shed upon the statement, and we can see where the fees get hidden and where the confusion takes place, it’s time to take a look at a much simpler way of doing this: Host Merchant Services offers a processing plan with no hidden fees. The company offers its merchants an Interchange Plus pricing plan. So right off the bat, there are no tiered pricing plan issues, so its merchants are not hit with “non-qualified” tier penalties and fees. Host Merchant Services also eschews a long-term contract. So there is no application or set up fee. No annual fee. No Non AVS Adjustment fee. Host Merchant Services does not penalize you with termination fees. Host Merchant Services also does not lock its merchants into contracts for equipment. The company provides free equipment, including free terminal paper. The prices that the company quotes during the application process are grandfathered, and will not increase at all during the lifetime of the business relationship.

It’s a simple and straightforward plan, really. Host Merchant Services shows you exactly what you will be charged on your monthly statement. The company has swept away many of the added charges that other companies hide on statement fees. And then the company sticks to the plan they quoted its merchant. The company will be happy to review your statement and help you find areas where you can save money each month.

So monthly statements may be extremely confusing –– to the point where one thinks it is being done on purpose. But using some of the guidelines put forth here, or using Host Merchant Services itself, you can find your way through the puzzle that is payment processing.

{kind=link}