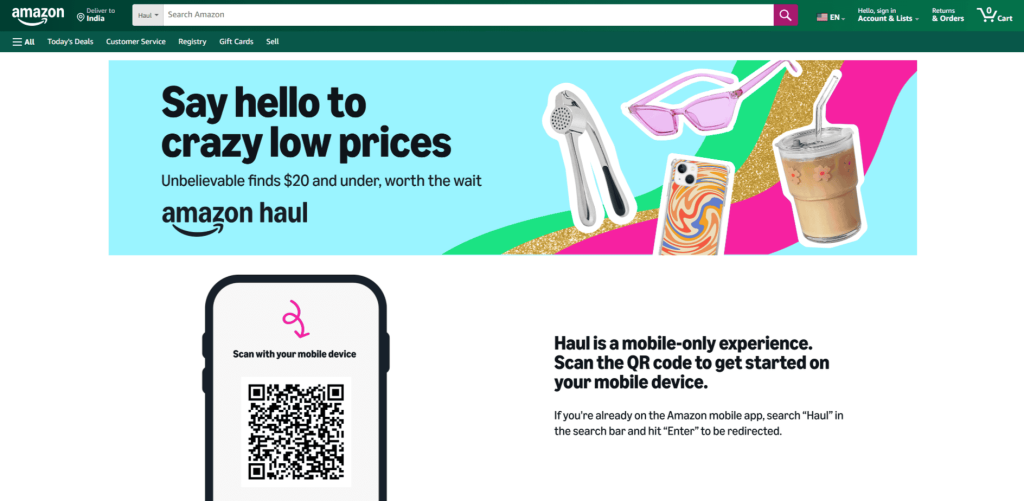

Amazon has launched a new feature in its mobile app named “Amazon Haul,” which provides a selection of items, including clothes, household goods, electronics, and more, each costing less than $20. This initiative targets cost-conscious consumers, positioning Amazon as a competitor to affordable retail outlets such as Temu and Shein.

This new platform offers a wide range of unbranded products in categories such as fashion, lifestyle, home essentials, and electronics. These items are sourced from international sellers vetted by Amazon and are covered by Amazon’s “A-to-z Guarantee.” The delivery timeframe for these products ranges from one to two weeks. Additionally, the feature prominently displays reduced prices on various items.

Key Takeaways

Launch of Amazon Haul: To compete with low-cost websites like Temu and Shein, Amazon launched a new storefront inside its app that sells unbranded goods for less than $20.

Cost and Shipping Details: Items are shipped from a warehouse in China, with delivery times ranging from one to two weeks. Orders over $25 qualify for free shipping, while smaller purchases incur a $3.99 fee.

Discounts and Return Policy: Customers can receive discounts for bulk purchases—5% off orders over $50 and 10% off those exceeding $75. Free returns are available for items over $3 within 15 days at various drop-off locations.

Strategic Focus and Challenges: Amazon’s move targets price-sensitive shoppers. However, longer delivery times and potential increases in import costs due to regulatory changes could impact its strategy in competing with established rivals.

Amazon Haul: Affordable Shopping to Compete with Temu and Shein

Amazon has launched “Amazon Haul,” a new online storefront with products priced at $20 or less. This move is designed to compete with budget retailers like Temu and Shein, known for their affordable products in clothes, household goods, electronics, lifestyle items, and more. Many products on Amazon Haul are priced under $10, with some available for as little as $1.

You can download the Amazon app for iOS and Android devices. Alternatively, you can visit www.amazon.com/haul on your mobile device’s browser. The storefront includes unbranded items like electronics, apparel, and home goods. For instance, it offers a phone case and a hairbrush, each for $2.99, and a sleeveless dress for $14.99.

To keep prices low, Amazon intends to distribute these products to U.S. customers from a warehouse in China. Expected delivery times range from one to two weeks. Orders exceeding $25 receive free shipping, while those below $25 are subject to a $3.99 shipping charge. This approach is Amazon’s strategic reaction to the growing popularity of Temu and Shein, which are known for their economical products. Nonetheless, both companies have been criticized for their environmental impact and are under regulatory examination for their business methods.

Shein primarily targets young women who are drawn to its affordably priced clothing. Temu, on the other hand, markets a wide range of items, including clothing, accessories, and kitchen gadgets, to price-conscious consumers.

Both Temu and Shein have been scrutinized for the environmental effects of their rapid fashion business models. They have also been questioned by lawmakers and regulatory bodies in the U.S. and abroad regarding several issues, including the characteristics of certain products available on their platforms.

Amazon has launched a new storefront accessible only through its mobile website and app and features a selection of unbranded products. Customers can purchase phone cases and hairbrushes for just $2.99 and sleeveless dresses for $14.99. Dubbed ‘Amazon Haul,’ this initiative highlights meager prices and budget-friendly activewear. The company guarantees customer satisfaction for all purchases within this collection through Amazon’s A-to-Z Guarantee. This assurance covers the condition of the products, ensuring protection against damages, defects, or discrepancies from descriptions.

Purchasing more through Amazon Haul can lead to greater savings. Orders totaling $50 or more receive a 5% discount, and those of $75 or more are reduced by 10%.

Additionally, Amazon offers free returns on all Haul purchases over $3 within fifteen days of delivery. Customers can return items at more than 8,000 drop-off locations across the U.S., including Amazon Fresh, UPS, Whole Foods Market, Staples, and Kohl’s.

Dharmesh Mehta, Vice President of Worldwide Selling Partner Services at Amazon, emphasized that customers appreciate discovering high-quality products at exceptionally low prices. He mentioned that Amazon collaborates with its selling partners to develop strategies to sustain these competitive prices. Mehta also pointed out that this initiative is in its initial phase, and Amazon intends to refine and enlarge it by integrating customer feedback in the coming weeks and months.

Additionally, Amazon may see an increase in the cost of importing goods from China. In September, the Biden administration introduced policies to curb the flow of inexpensive products from China. This strategy is designed to reduce U.S. dependence on Beijing, but it may result in higher prices for American consumers, many of whom shop with retailers like Temu and Shein. Moreover, President-elect Donald Trump has suggested a 60% tariff on Chinese goods, which could further impact costs.

Amazon is willing to test whether customers will accept longer delivery times in exchange for significantly lower prices. This strategy marks a departure for Amazon, which has previously established its leadership in the e-commerce sector by providing faster delivery times than its rivals. The company revolutionized online shopping by introducing free two-day shipping and has since reduced delivery times even further. Amazon currently provides same-day or next-day delivery in many areas, and in specific locations, customers can receive their orders within hours.

In September 2024, Amazon’s U.S. website traffic was relatively stable, showing a modest increase to 236.1 million unique visitors. By contrast, Shein has experienced consistent growth, reaching 52.5 million visitors. Meanwhile, Temu has seen a decline in traffic since a high of over 93 million visitors in June 2023, leveling off at approximately 71.5 million.

Conclusion

Amazon Haul is a calculated effort to attract budget-conscious shoppers while addressing competition from platforms like Temu and Shein. By offering low-cost, unbranded products across multiple categories, Amazon appeals to consumers, prioritizing affordability, even at the expense of longer delivery times.

With features like free returns, purchase discounts, and its trusted A-to-z Guarantee, Amazon enhances its value proposition for shoppers exploring this new storefront. However, rising import costs and regulatory challenges may influence its long-term sustainability. As Amazon fine-tunes this initiative, its success will depend on balancing low prices, customer expectations, and evolving market conditions.

The rewards app Fetch and Albertsons Media Collective, the retail media branch of Albertsons Companies, Inc., have launched their first retail media network collaboration. Through this relationship, Albertsons Media Collective can expand its range of services, providing consumer packaged goods manufacturers with additional avenues to increase sales that are unique to this store.

Brands can now include Fetch in their marketing strategies alongside their existing commitments with Albertsons Media Collective. This integration will allow them to target customers more effectively and efficiently through Fetch as part of their comprehensive marketing efforts.

Key Takeaways

First RMN Partnership for Fetch: Fetch has partnered with Albertsons Media Collective to launch their inaugural retail media network partnership. This collaboration provides consumer packaged goods (CPG) brands with fresh opportunities to increase sales via customized marketing campaigns.

Integration with Marketing Strategies: Brands can now integrate Fetch Points into their marketing efforts with Albertsons Media Collective, enhancing customer engagement during key stages of the shopping journey.

Data-Driven Insights and Technology: Fetch leverages AI and consumer purchase data to optimize advertising spend and provide insights, processing $180 billion in transactions annually by 2024.

Enhanced Loyalty and Shopper Experience: The partnership enhances Albertsons’ loyalty programs by allowing customers to earn rewards effortlessly, benefiting both in-store and online shoppers.

Fetch and Albertsons Media Collective Partner to Enhance Retail Media and Consumer Engagement

The rewards app Fetch, based in Madison, has teamed up with Albertsons Media Collective, the media division of Albertsons Companies Inc., among the largest grocery and drugstore chains in the U.S. According to a press release, this collaboration aims to help consumer packaged goods (CPG) brands increase their sales in Albertsons stores while also expanding the services Albertsons offers.

The Fetch app integrates with Albertsons Media Collective, providing CPGs an additional method to connect with shoppers before and during decision-making. Brands now have the option to integrate Fetch Points with their current engagements with Albertsons Media Collective. This integration enables brands to reach customers through the rewards app, complementing their comprehensive marketing strategies.

By the end of 2024, Fetch’s ecosystem will process $180 billion in transactions annually. It utilizes artificial intelligence and machine learning to distribute advertising spending based on verified consumer purchase data. Fetch gains deep insights into consumer purchasing habits, powered by over 5 billion receipts submitted by users, earning them $1 billion in Fetch Points. These points motivate consumers to try new products, increase purchases, and sustain brand relationships.

Robin Wheeler, Chief Revenue Officer at Fetch, stated that as retail media networks seek to increase revenue and better support their shoppers, they are broadening successful programs already recognized and trusted by leading partners. Fetch aims to enhance existing RMN frameworks, simplifying the process of engaging consumers for life through the benefits of Fetch Points.

Chris Placencia, Senior Client Success Director at Albertsons Media Collective, shared that teaming up with Fetch improves their loyalty program. It allows customers to earn extra rewards on purchases without changing a consumer’s usual shopping experience. This collaboration builds on their existing platform, giving shoppers more opportunities to benefit from every in-store or online transaction.

Mondelēz International has initiated using Fetch’s RMN integration with Albertsons Media Collective to promote its prominent brands, such as Triscuit, Ritz Crackers, and Wheat Thins. This partnership allows Mondelēz International to direct consumers to Albertsons stores by offering targeted, purchase-related incentives through the app. These promotions attract new customers, boost sales, and strengthen retailer-specific brand loyalty.

Anne Martin, the director of shopper marketing at Mondelēz International, based in Chicago, emphasized that modern consumers demand personalized and relevant interactions from brands they like, and innovation is essential to fulfilling these expectations. The partnership with Albertsons and Fetch provides a new way to engage consumers across their shopping experience while building loyalty with a long-term vision, effectively strengthening their ties with customers and supporting business expansion.

Albertsons Media Collective, the retail media branch of Albertsons Cos., reaches consumers in over 2,200 locations across 34 states and the District of Columbia. Based in Boise, Idaho, Albertsons runs 2,269 retail stores, 1,725 pharmacies across 34 states, 403 associated fuel centers, 22 distribution centers, and 19 manufacturing facilities. The company operates under over 20 banners and is ranked No. 9 on The PG 100, Progressive Grocer’s 2024 list of North America’s top food and consumables retailers. Progressive Grocer has also recognized Albertsons as one of its Retailers of the Century.

About Albertsons

Founded in 1939 by Joe Albertson in Boise, Idaho, Albertsons Companies, Inc. has expanded to become one of the major food and drug retailers in the United States. With more than 2,200 stores across 34 states and the District of Columbia, the company operates under several recognized banners such as Albertsons, Safeway, Jewel-Osco, Vons, Acme, Shaw’s, Randalls, Tom Thumb, Pavilions, United Supermarkets, Haggen, Star Market, Kings Food Markets, Carrs, and Balducci’s Food Lovers Market.

In addition to its retail operations, Albertsons supports its stores with 22 distribution centers and 19 manufacturing plants, ensuring efficient supply chain management and product availability. The company’s omnichannel approach and commitment to innovation aim to make shopping more convenient for customers, contributing to its sustainable growth.

About Fetch

Fetch, established in 2013 and headquartered in Madison, Wisconsin, is a mobile shopping platform that enables users to earn rewards by scanning their receipts. The app recognizes receipts from various retailers, including grocery stores, drugstores, and restaurants, allowing users to accumulate points redeemable for gift cards and other rewards.

For brand partners, Fetch offers insights into consumer shopping habits, providing a comprehensive view of purchasing behaviors. This data enables brands to engage with customers more effectively and tailor their marketing strategies. As of 2021, Fetch reported an annual revenue of $102 million and had secured $325.3 million in total funding.

Conclusion

The partnership between Fetch and Albertsons Media Collective highlights a growing trend in leveraging retail media networks to enhance consumer engagement and brand loyalty. Combining Fetch’s data-driven approach with Albertsons’ established retail presence, this collaboration offers consumer packaged goods brands a powerful way to connect with shoppers more effectively.

The integration supports innovative marketing strategies and enriches the shopping experience by providing added rewards and incentives for customers. As both companies evolve, this partnership sets a foundation for mutually beneficial growth and customer-centric innovation in the retail and rewards sectors.

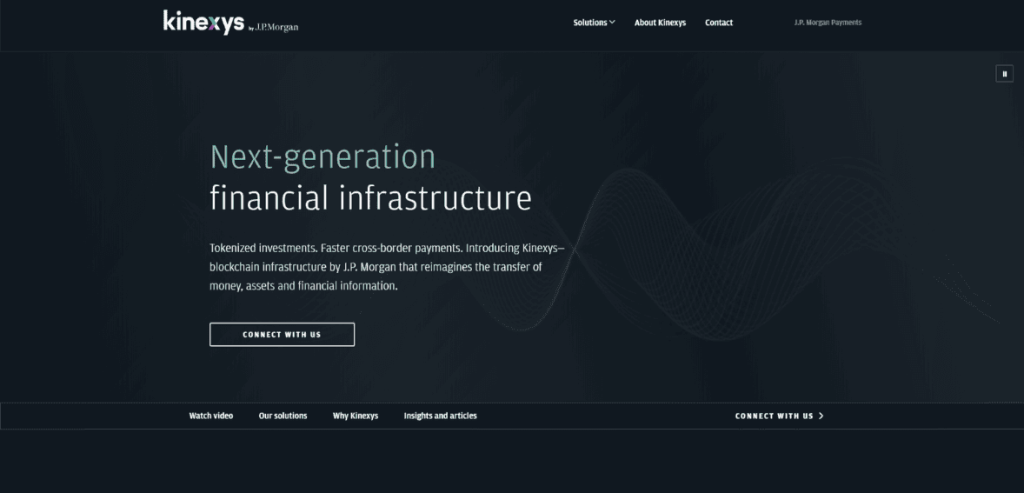

JPMorgan has renamed its blockchain operation Onyx to Kinexys and aims to expand its capabilities to encourage wider use of blockchain technology and tokenization in mainstream financial services.

The platform’s new name is Kinexys, and its payment settlement system, formerly JPM Coin, has been renamed Kinexys Digital Payments. Alongside these changes, JPMorgan has also revealed plans to introduce on-chain foreign exchange conversions to the platform next year, starting with USD to Euro transactions and intending to include additional currencies later.

Speaking at the Singapore Fintech Festival, Kinexys CEO Umar Farooq explained that the updates support automated, real-time clearing and settlement in multiple currencies.

Key Takeaways

Kinexys Rebranding: JPMorgan has renamed its blockchain platform from Onyx to “Kinexys,” with its JPM Coin system now called “Kinexys Digital Payments.” The change highlights the firm’s focus on integrating blockchain technology into mainstream financial operations.

On-Chain Foreign Exchange (FX): Kinexys plans to introduce on-chain FX functionality by 2025, starting with USD-to-Euro conversions. Future expansions will include other currencies to improve cross-border payment processes and minimize counterparty risks.

Transaction Growth and Capabilities: Since its inception, the platform has facilitated over $1.5 trillion in transactions and currently processes about $2 billion daily. It supports real-time multi-currency clearing to streamline global financial operations.

Focus on New Features: Kinexys’s Labs division is developing proof-of-concept projects targeting privacy and identity solutions. These efforts seek to broaden blockchain’s role in financial services and set new benchmarks for its applications.

JPMorgan Rebrands Blockchain Platform as Kinexys, Expanding Into Forex Services

JPMorgan has rebranded its blockchain-based platform to Kinexys as it gears up to introduce foreign exchange services to accommodate its increasing clientele. Originally launched in 2019 as JPM Coin and later renamed Onyx, the financial services firm revealed that the platform will soon facilitate forex transactions for its growing list of international clients.

The need for this expansion stems from a significant increase in usage. The platform has experienced a 1,000% year-over-year growth in payment transactions, prompting JPMorgan to enhance its infrastructure and introduce new services. Since its inception, the blockchain platform has processed over $1.5 trillion in notional value, with daily volumes now surpassing $2 billion. However, this amount is relatively small compared to the $10 trillion in traditional payments the bank handles daily.

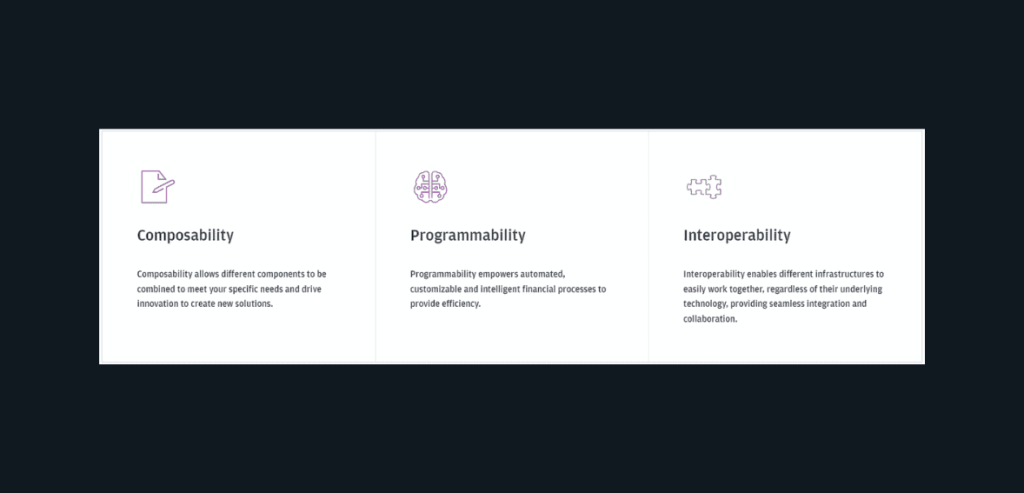

The company explained that the new name, Kinexys, is inspired by the term “kinetic,” reflecting the global dynamic movement of money, assets, and financial data. Additionally, the revamped platform will include advanced features like on-chain privacy, identity verification, and tools focused on composability within its network.

In a statement, Umar Farooq, co-head of JPMorgan Payments, mentioned their objective to surpass the constraints of existing technology and fulfill the potential of a multichain environment. He emphasized their commitment to creating a more integrated ecosystem that overcomes the barriers of current systems, enhances interoperability, and diminishes the restrictions of present-day financial infrastructure.

Tokenization of real-world assets like conventional financial instruments has rapidly expanded within the blockchain sector, with major banks playing significant roles. JPMorgan has pioneered in this area through its platform, originally named Onyx, and its blockchain-based payment technology, JPM Coin, now called Kinexys Digital Payments.

The bank plans to implement on-chain foreign exchange features on its platform by the first quarter of 2025. This initiative enables automated, around-the-clock, near-instant clearing and settlement in multiple currencies. Initially, the service will handle transactions in USD and Euro, but it will expand to other currencies in the future.

The bank also noted significant increases in client engagement, product offerings, and transaction volumes, positioning it to further push the integration of blockchain technology and tokenization into mainstream financial services.

JPMorgan is not alone among major banks that are adopting blockchain technology. Last year, over twenty financial institutions, such as BNP Paribas and Goldman Sachs, introduced the Canton Network, a blockchain platform dedicated to tokenizing real-world assets. Additionally, earlier this month, the Singapore-based bank DBS launched its own Token Services platform, which provides a collection of blockchain-powered tools.

About JPMorgan

JPMorgan Chase & Co., headquartered in New York City, is the largest bank in the United States by assets and a leader in global financial services. The firm has a rich history dating back to 1799 and has grown through significant mergers, including the 2000 combination of J.P. Morgan & Co. and Chase Manhattan Bank. It operates in over 100 markets worldwide, providing comprehensive services such as investment banking, retail banking, asset management, and treasury services.

The company’s key divisions include Community and Consumer Banking, Asset and Wealth Management, Corporate and Investment Banking, and Commercial Banking. These segments cater to businesses, individuals, institutions, and governments, offering tailored solutions like mortgages, credit cards, advisory services, and investment products. As of 2023, JPMorgan Chase manages assets exceeding $3.9 trillion, with over 309,000 employees globally.

The firm’s innovative approach and global reach make it a critical player in financial markets. It serves millions of clients and drives advancements in banking technology and services. Its dedication to sustainability and community initiatives further underscores its leadership in the industry.

Conclusion

JPMorgan has renamed its blockchain platform Kinexys as part of a strategy to lead the use of blockchain and tokenization in mainstream finance. This new name highlights the platform’s goal to support fast, real-time transactions in a multichain environment. Starting in 2025, Kinexys will offer on-chain foreign exchange services, beginning with conversions between USD and Euro. This change shows JPMorgan’s commitment to making cross-border payments more efficient and reducing risks.

Since launching, Kinexys has processed over $1.5 trillion in transactions and handles more than $2 billion daily. This shows how scalable and impactful blockchain technology can be in finance. Kinexys’s Labs division is also working on advanced tools like on-chain privacy and identity solutions to keep pushing for innovation.

The broader industry is also moving towards blockchain for tokenizing real-world assets, with competitors like DBS and the Canton Network joining in. By using its global reach and strong technology, JPMorgan is not just improving its blockchain services but also helping to change financial systems around the world. This rebranding positions Kinexys as a key part of JPMorgan’s vision for the future of financial services.

Last week, TGI Fridays filed for bankruptcy protection in Northern Texas, focusing on restructuring the business. The company, headquartered in Dallas, submitted a Chapter 11 petition to a federal court in Texas. This move is intended to manage existing debts and develop strategies to sustain the brand following the recent closure of multiple locations. The filings indicate the company’s assets and liabilities are between $100 million and $500 million.

Established in New York City in 1965, TGI Fridays has encountered several operational challenges recently. These include rising costs and shifts in consumer behavior, largely due to the impacts of the COVID-19 pandemic, which significantly changed the dining industry.

Key Takeaways

Bankruptcy for Restructuring: TGI Fridays filed for Chapter 11 bankruptcy in Texas to reorganize its debts and restructure operations. This decision follows years of financial challenges, accelerated by COVID-19 impacts on dining habits and operational costs.

Revenue Decline and Strategic Adjustments: Once a leading chain with $2 billion in revenue, TGI Fridays revenue has fallen to $728 million, partly due to location closures and lower sales per unit. Efforts to revive sales included new menu items, value pricing, and expanded happy hour options, but these strategies struggled against stronger competitors.

Asset Takeover and Merger Disruption: In 2024, bondholders took over key assets, stopping a planned $220 million merger with UK franchisee Hostmore. This event reduced TGI Fridays’ royalty income and hindered a planned shift toward a franchise-heavy model.

Franchise Support and Temporary Funding: TGI Fridays Franchisor, LLC will provide short-term funding to support franchisees while TGI Fridays Inc. restructures. This move aims to preserve the company’s franchise operations and stabilize its corporate structure for long-term recovery.

TGI Fridays Files for Bankruptcy in Texas, Citing COVID-19 and Capital Structure Issues

TGI Fridays has declared bankruptcy in Northern Texas as part of a plan to reorganize the business. TGI Fridays’ Executive Chairman Rohit Manocha stated that the main reasons for its financial difficulties were the impacts of COVID-19 and issues with its capital structure. The company aims to improve its corporate structure to help its restaurants perform better, continued Rohit in a press release.

Since its first branch debuted in Manhattan, New York, in 1965, TGI Fridays, which is owned by TriArtisan Capital Advisors, has enjoyed great success. The brand grew quickly, reaching its highest point in 2008 with 601 US outlets and $2 billion in sales.

However, by 2023, revenue had dropped to $728 million or 15%, showing a sharp decline in the company’s performance due to closing some locations and lower sales per unit, as stated in a court document. The company tried several strategies to improve sales, including introducing virtual brands through C3, launching the Grilled and Sauced menu in 2023, and considering new real estate strategies focused on less capital-intensive hotel expansion.

According to Richter, the company also introduced a new value menu with 10 meals starting at $9.99, boosted its ‘happy hour’ program, offered direct mail promotions, and presented attractive loyalty incentives. Consumer perception of the brand’s pricing improved by 15 percentage points from the first to the second quarter. However, as customers became more sensitive to prices, competitors like Chili’s, who have more resources and are publicly traded, were more effective in promoting their value meals to consumers.

Other post-pandemic shifts in consumer behavior—such as reduced alcohol consumption, increased remote work, and a preference for fast-casual dining options like Shake Shack and Chipotle—have adversely affected the chain’s profitability.

Kyle Richter, the Chief Restructuring Officer at TGI Fridays, mentioned that the company faced challenges in funding national marketing campaigns, which affected its competitive stance against larger chains. He highlighted that Fridays struggled to maintain its market share due to these financial limitations.

In September 2024, the company failed to meet the terms of its bond agreement, leading bondholders to take control of several assets, including restaurant royalties. This move, a manager termination event, interrupted a planned $220 million merger with the UK franchisee Hostmore. The merger was intended to shift TGI Fridays towards a fully franchised business model; however, the takeover of assets halted these efforts.

The loss of assets forced TGI Fridays to forfeit a substantial part of its income, as it could no longer collect revenue from restaurant royalties.

TGI Fridays’ financial troubles were also affected by the end of its relationship with Citibank, which had managed the company’s financing since 2017. Citibank’s absence resulted in a lack of management in key areas such as licensing, franchise operations, personnel decisions, and funding securitization. A permanent successor has yet to be found, and a consulting firm has temporarily stepped in to handle these duties.

Its financial strategy, especially its dependence on “whole business securitization,” played a role in its difficulties. This method involved the issuance of corporate bonds backed by expected cash flows from franchise royalties. Poor financial practices, including payment delays to vendors and a drop in restaurant performance, further destabilized the company’s financial health.

There are currently 163 TGI Fridays restaurants in the US, down from 269 the previous year. The company shut down 36 locations in January and several others over the past week. Most closures were company-owned units; the company operated 140 US restaurants at the start of the year but only 39 remained during the bankruptcy filing—a small part of the 461 TGI Fridays locations worldwide.

Another entity, TGI Fridays Franchisor, holds the brand’s intellectual property and licenses it to 56 independent operators in 41 countries, where the franchised locations continue to run.

TGI Fridays Franchisor, LLC will provide temporary funding to TGI Fridays Inc. to ensure ongoing support to its franchisees as it develops a permanent solution. Manocha described the latest measures as tough but essential to safeguard the interests of the company’s stakeholders, which include franchisees in the US and internationally and its employees worldwide. He emphasized that the restructuring would enable the company’s restaurants to operate with an optimized corporate infrastructure, allowing them to reach their full potential.

This year, over ten restaurant chains, such as Tijuana Flats, Buca di Beppo, and Red Lobster, have filed for bankruptcy. Red Lobster closed more than 106 locations but has now exited bankruptcy and named Damola Adamolekun as the new CEO.

About TGI Fridays

TGI Fridays, founded in 1965 by Alan Stillman and Daniel R. Scoggin in New York City, is a well-known American casual dining restaurant chain famous for its American cuisine and lively atmosphere. “TGI Fridays” stands for “Thank God It’s Friday,” highlighting the brand’s focus on creating an energetic dining experience. As of June 2024, the chain operates over 400 locations in 44 countries, including 163 in the United States. The menu includes a variety of dishes such as sizzling entrees, appetizers, salads, seafood, sandwiches, desserts, and both alcoholic and non-alcoholic beverages.

Ownership of the company has changed over the years; in May 2014, TGI Fridays was acquired by Sentinel Capital Partners and TriArtisan Capital Partners. By October 2019, TriArtisan became the sole stakeholder after purchasing Sentinel’s remaining shares.

Conclusion

TGI Fridays recent bankruptcy filing reflects the broader challenges facing the casual dining industry as consumer preferences and economic conditions shift. COVID-19 and financial and operational issues significantly impacted the brand’s stability, leading to restructuring.

Despite efforts to revitalize sales through menu adjustments and value-based promotions, competition and rising operational costs have intensified financial pressures. The reorganization plan, supported by short-term funding from TGI Fridays Franchisor, LLC, aims to preserve the franchise network and refocus the brand’s business strategy. With effective restructuring, TGI Fridays hopes to stabilize its financial foundation and adapt to the evolving dining landscape, ensuring the franchise’s and its stakeholders’ long-term resilience.

Bitcoin price surge is now past the $90,000 mark, continuing its strong performance amid expectations that Donald Trump’s presidency could benefit cryptocurrencies. The leading digital currency has seen significant activity since the election, reaching new highs this month.

The price on 13th Nov shows the rate crossing the $92,500 mark, showing a 38%+ increase month to date. During his campaign, Trump supported digital assets, pledging to position the United States as a global cryptocurrency leader and build a substantial national bitcoin reserve.

Key Takeaways

Bitcoin’s Record Highs: Bitcoin recently hit over $92,500, influenced by expectations of a more crypto-friendly U.S. regulatory environment under the incoming administration, boosting investor confidence.

Policy Shifts on the Horizon: The new administration aims to reshape crypto regulation, including potential changes in SEC leadership and establishing a national Bitcoin reserve, signaling a major shift in federal engagement with digital currencies.

Market-Wide Growth: Beyond Bitcoin, other cryptocurrencies like Dogecoin and Ethereum have seen significant gains, and crypto-related stocks, such as Coinbase and Robinhood, are also rising as market optimism extends across the digital asset space.

Analyst Division on Bitcoin’s Future: Experts remain divided on Bitcoin’s potential path forward. While some believe pro-crypto policies could propel Bitcoin to $100,000 by year-end, others emphasize caution due to the market’s high volatility and the possibility of unexpected regulatory hurdles.

Bitcoin Price Surge: Hits New Highs as Post-Election Optimism Fuels Cryptocurrency Market Growth

Bitcoin soared to a record high of over $92,500 before dropping to $88,823 on November 14th, marking a more than 10% increase since the elections. The cryptocurrency has seen significant growth since Trump’s victory in the recent U.S. presidential election, surpassing its previous peaks several times. This rise is attributed to investor confidence in a more favorable regulatory environment for digital assets under the incoming administration. The total value of the global cryptocurrency market has also exceeded $3 trillion for the first time in three years.

Edul Patel, CEO of Mudrex, noted that breaking this significant resistance point has increased investor interest and trading volume across platforms.

According to a report, Trump stated in his campaign that he intends to make the United States the global center for Bitcoin and cryptocurrencies.

He intends to replace SEC Chair Gary Gensler, known for a stringent approach to crypto regulation, with a more crypto-friendly appointee like Mark Uyeda and Paul Atkins. Additionally, Trump has proposed the establishment of a national Bitcoin reserve, signaling a potential shift in federal engagement with digital currencies.

Mark Uyeda, currently serving as an SEC Commissioner, has been critical of the agency’s stringent approach to crypto regulation. In October 2024, he described the SEC’s policies as “a disaster for the whole industry,” advocating for clearer guidelines and a more collaborative approach with the crypto sector. Paul Atkins, a former SEC Commissioner under President George W. Bush, is also under consideration. Atkins has previously opposed heavy fines on companies violating securities laws and has shaped a more lenient regulatory approach.

The rally in Bitcoin’s price has positively affected related financial instruments. BlackRock’s spot Bitcoin ETF reported a record trading volume of $4.5 billion, indicating growing mainstream investor interest and confidence in the asset. The positive sentiment has extended beyond Bitcoin—other cryptocurrencies, such as Dogecoin, at $0.39 as of 14th Nov, witnessed over 240% gains in a one month, and Ethereum, at $3,083.55 as of 14th Nov, saw over 22% gains in a one month. Crypto-related stocks, including Coinbase Global and Robinhood Markets, have also experienced significant increases, reflecting broader market optimism about the future of digital assets under the new administration.

Analysts are divided on Bitcoin’s trajectory. Some predict that the cryptocurrency could reach $100,000 by the end of the year, citing the anticipated pro-crypto policies of the incoming administration as a catalyst. Others advise caution, noting the inherent volatility of the crypto market and the potential for unforeseen regulatory challenges.

During Trump’s earlier administration, reductions in corporate taxes injected more liquidity into the market, spurring investments in cryptocurrencies. In September, Trump revealed plans to launch a digital currency platform called World Liberty Financial with his sons and other entrepreneurs. However, the report noted that earlier this month’s launch was less successful, with only a few tokens sold.

Elon Musk has also had a notable impact on the recent U.S. elections and, indirectly, on the Bitcoin market, largely due to his substantial support for Donald Trump. Musk’s contributions have been financial and strategic, utilizing his media influence and platforms to support Trump’s campaign, which has intertwined with broader market reactions, including those affecting Bitcoin.

Musk donated millions to Trump and other Republican causes, significantly aiding the Trump campaign. His financial involvement exceeded many other contributors, with substantial sums directed toward campaign activities and political action committees.

On a lighter note, the President-elect launched the “Department of Government Efficiency” (D.O.G.E) shortly after his election victory. This title cleverly nods to Musk’s favorite cryptocurrency and the department’s intended function, a topic of considerable discussion. The main goal of this initiative is to reduce federal spending and make government operations more efficient, potentially saving billions of dollars.

Elon Musk has shown support for the plan, especially because he sees it as a way to reduce what he views as excessive government waste. This matches his previous efforts to improve efficiency at his companies, like Tesla and SpaceX. Musk’s interest in leading such a department reflects his vision of a more efficient government that uses technology and innovation to cut costs and boost productivity.

Though the proposed reforms are serious, Musk’s involvement with the “DOGE initiative” adds a playful twist, as it references the Dogecoin cryptocurrency and his frequent use of cultural memes.

Conclusion

Bitcoin’s recent surge reflects growing investor confidence in the potential for more favorable U.S. policies on digital assets under the incoming administration. The anticipated regulatory shift, including Trump’s proposed SEC leadership, changes and initiatives like the national Bitcoin reserve has fueled optimism in the cryptocurrency market, with prices and trading volumes reaching new heights.

However, the crypto market’s volatility persists, and regulatory uncertainties remain a concern. While some analysts foresee Bitcoin hitting $100,000 by year’s end, others urge caution, citing the market’s inherent unpredictability. The broader market sentiment, including Musk’s financial backing and his symbolic support through initiatives like the “DOGE Department,” highlights both strategic and cultural dynamics at play as the U.S. faces a potentially transformative era for digital finance.

Canadian FinTech company Nuvei has partnered with BigCommerce, an open software-as-a-service (SaaS) eCommerce platform, to provide customizable payment solutions globally that were traditionally limited to large enterprises. Nuvei and BigCommerce partnership covers North America, Europe, and the APAC region, allowing BigCommerce clients to integrate Nuvei’s omnichannel payment solutions through its Nuvei for Platforms service. This integration aims to unify online and physical store payment systems under one processing partner.

For BigCommerce clients, Nuvei delivers extensive transaction processing services, including payment acceptance, pre-authorization, refunds, advanced 3DS2 security technology, multi-currency support, stored card processing, and integrated checkout solutions. Brands and retailers using BigCommerce will gain benefits such as quick, bank-independent settlements, various alternative payment options, centralized payment management, and dedicated support for integrations.

Key Takeaways

Enhanced Payment Capabilities for All Business Sizes: The Nuvei BigCommerce partnership extends enterprise-grade payment solutions to businesses of all sizes, providing smaller merchants access to tools typically reserved for larger companies.

Global Payment Flexibility: With support for over 700 payment methods and 40 cryptocurrencies, Nuvei’s integration allows BigCommerce merchants to meet the diverse payment preferences of customers in North America, Europe, and Asia-Pacific.

Improved Cash Flow and Operational Efficiency: The integration features same-day and next-day settlement options and a bank-agnostic processing system, allowing merchants to reduce bank-related processing delays and improve cash flow.

Comprehensive Support for eCommerce Growth: By combining advanced security, multi-currency support, and embedded checkout solutions, Nuvei and BigCommerce offer a unified payment infrastructure that enhances the customer experience and simplifies transaction management for eCommerce businesses.

Nuvei and BigCommerce Partnership Advances eCommerce Payment Capabilities Globally

The recent partnership between Nuvei, a Canadian fintech company, and BigCommerce, an open SaaS eCommerce platform, represents a notable development in eCommerce payment solutions. This collaboration, announced on October 22, 2024, is designed to broaden the scope of available payment solutions for eCommerce businesses operating on BigCommerce, a platform that serves both B2C and B2B clients globally.

Nuvei’s “Nuvei for Platforms” solution will be integrated into BigCommerce, providing businesses with a unified, omnichannel payment solution. This approach enables merchants on BigCommerce to streamline transaction processes, accept multiple forms of payment, manage refunds, and leverage additional features such as advanced 3DS2 technology for security, support for multiple currencies, and embedded checkout options.

The payment integration also aims to bridge the gap between online and physical store transactions by offering a centralized payment management system. This solution simplifies operations and ensures quicker access to revenue with options for same-day or next-day settlements. This key feature benefits businesses by improving cash flow.

Other FinTech collaborations have also led to developing and integrating comprehensive omnichannel payment solutions. For instance, the Revolut Business Payment Gateway was integrated with the BigCommerce platform in August. This enhancement has streamlined payment processing for online businesses and improved customers’ checkout processes.

One of the standout features of this Nuvei BigCommerce partnership is the support for diverse payment methods. Nuvei’s platform offers over 700 alternative payment methods and supports 40 cryptocurrencies, allowing businesses to meet the evolving demands of a global customer base.

This flexibility is particularly relevant as consumer preferences shift toward more varied payment options across markets like North America, Europe, and Asia-Pacific. Nuvei’s bank-agnostic processing system also enables BigCommerce merchants to bypass potential bank-related processing delays, further enhancing operational efficiency.

Another advantage of the Nuvei-BigCommerce integration is its adaptability for businesses of all sizes, from small to enterprise-level companies. Typically, such comprehensive payment solutions are accessible mainly to larger companies, but this Nuvei BigCommerce partnership aims to bring enterprise-grade payment capabilities to smaller merchants.

By doing so, Nuvei and BigCommerce are positioning themselves as catalysts for business growth, making advanced payment processing tools more widely accessible. This move aligns with Nuvei’s strategy to expand its influence in the eCommerce SaaS sector, which is seeing rapid growth as digital commerce continues to evolve globally.

Philip Fayer, Nuvei’s CEO, expressed excitement about the partnership with BigCommerce. The goal is to introduce Nuvei for Platforms’ advanced payment solutions to customers worldwide, starting with customers in Europe, North America, and Australia.

This collaboration decisively enhances the connection between businesses and their customers through superior payment solutions. It delivers tailored options specifically designed for eCommerce businesses poised for expansion. By leveraging Nuvei’s expertise in unified payment solutions alongside BigCommerce’s powerful platform, they empower customers with the essential resources to excel in online and offline markets.

Shannon Ingrey, VPt and General Manager, APAC, at BigCommerce, mentioned that their collaboration with Nuvei underscores their dedication to offering customers access to top-tier technology and service providers. Nuvei aligns with its goal to assist brands and retailers in increasing sales and accelerating growth to achieve greater success. They are eager to work together to provide mutual support to their customers.

The Nuvei BigCommerce partnership marks a significant step forward in the eCommerce payments landscape, particularly by equipping BigCommerce merchants with an extensive, customizable payment infrastructure flexible enough to cater to local and global audiences. As eCommerce expands, partnerships are instrumental in making advanced financial tools available to a wider range of businesses, empowering them to confidently navigate a competitive digital marketplace.

In August 2024, Nuvei and Fintech360 introduced a new cashier solution. This collaboration aimed to help forex businesses and their clients enhance productivity using Fintech360’s services.

The launch responded to the financial landscape, where effective payment processing is crucial for success, particularly in the Forex B2B sector. With the growth of digital commerce, organizations are under increased pressure to provide secure and efficient payment methods. Recognizing this need, fintech companies are concentrating on developing this area and providing solutions that help businesses grow and increase their international presence.

Recently, BigCommerce announced a change in its leadership, with Travis Hess stepping in as CEO following Brent Bellm’s departure. The company also reported an 8% increase in its year-over-year earnings for the second quarter of 2024, with revenues nearing $82 million and an adjusted EBITDA of $3 million. It anticipates third-quarter revenues to be between $82 million and $84 million, with full-year revenues expected to range from $330.2 million to $335.2 million.

In light of these announcements, Stifel adjusted its price target for BigCommerce shares to $8.00, maintaining a Buy rating. Other financial institutions such as Needham, Barclays, Oppenheimer, and KeyBanc have also maintained their positive ratings, recognizing the company’s potential for growth despite some challenges.

In addition, BigCommerce has added three new executives to its team: Doug Hollinger, John Huntington, and Ryan Means. These new appointments aim to improve the company’s market strategy, extend global partnerships, and enhance service quality. These efforts are part of BigCommerce’s strategy to stay competitive in the ecommerce platform sector and support growth for its customers and partners.

About Nuvei

Nuvei Corporation offers payment technology solutions to merchants and partners across regions, including North America, the Middle East, Europe, Latin America, Africa, and the Asia Pacific. The company provides a platform that supports customers in making and receiving payments worldwide, irrespective of location, device, or payment preference. Their offerings include an integrated payments engine with extensive processing capabilities, a solution for smooth payment processes, and a comprehensive selection of business intelligence and risk management tools.

Nuvei Corporation promotes and sells its products and services through direct and indirect channels, strategic platform integrations, local sales teams, and partners. Previously known as Pivotal Development Corporation Inc., the company rebranded to Nuvei Corporation in November 2018. Established in 2003, Nuvei Corporation is based in Montreal, Canada.

BigCommerce is a cloud-based eCommerce platform designed for established and expanding businesses. It offers enterprise-level features, open architecture, and access to an extensive app ecosystem, optimizing marketplace performance. The platform helps businesses increase online sales while reducing costs, time, and complexity by 80% compared to traditional on-premise software.

BigCommerce supports B2C and B2B eCommerce for over 60,000 brands, including over 2,000 mid-market companies and 30 Fortune 1000 firms. Notable clients include Ben and Jerry’s, Assurant, Skullcandy, Paul Mitchell, Toyota, and Sony.

Conclusion

The Nuvei and BigCommerce partnership highlights a shift in the eCommerce payment landscape, bringing advanced payment capabilities that were once exclusive to larger enterprises to businesses of all sizes. By integrating Nuvei’s diverse, secure, and flexible payment solutions into BigCommerce’s platform, this collaboration provides merchants with enhanced options to meet global payment demands and streamline operations.

As digital commerce expands, partnerships like this one equip eCommerce businesses with the tools to remain competitive in a fast-paced market, supporting growth and customer satisfaction across multiple regions.

A few weeks back, the U.S. Consumer Financial Protection Bureau introduced new open banking rules designed to simplify the process for consumers to switch financial services providers and encourage competition. The Open banking rules mandate that traditional banks and fintech firms allow consumers to transfer their personal data between providers at no cost.

Banking industry groups, which the rule could negatively impact, quickly criticized it, raising concerns about consumer data security and questioning the agency’s authority. In contrast, fintech organizations welcomed the rule, saying it would enable secure consumer data transfers.

Key Takeaways

Greater Control and Flexibility for Consumers: The rule lets consumers transfer their banking history and other financial data between providers without fees, making it easier to switch to institutions offering better services or terms.

Boosted Competition and Access to Better Rates: The rule is expected to drive competition by allowing consumers to compare and move accounts more freely. Consumers can seek higher deposit rates, lower loan rates, and improved credit options, particularly benefiting those with limited credit history.

Enhanced Data Security and Privacy Standards: Financial service providers and third-party firms must follow strict data access and usage guidelines, limiting data collection to specific consumer requests. They must also have clear revocation and data deletion processes, empowering consumers to control how their information is used.

Mixed Reception and Legal Challenges: While fintech advocates see the rule as a positive step for consumer choice, the banking sector has raised concerns over data security and regulatory overreach, leading to a lawsuit claiming the rule imposes security risks and could increase compliance burdens.

CFPB’s New Rule Enhances Consumer Data Control and Aims to Boost Competition in Financial Services

The Consumer Financial Protection Bureau just finished a rule that gives people more control over their financial data. This wraps up a project they started back in 2010 with section 1033 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, which established the right for consumers to access their account data freely and to permit third parties to access this data on their behalf.

On October 23, 2024, the bureau issued its final Open banking rules. The rule’s implementation will be staggered, starting with larger providers who will be required to comply earlier than smaller ones. Financial institutions must adhere to the rule depending on their size. The largest will need to meet the requirements by April 1, 2026, whereas the smallest institutions have a deadline of April 1, 2030. Under this rule, financial service providers must provide consumers and their authorized third parties with access to financial data upon request. This data must be delivered electronically and safeguarded to ensure both security and reliability. Additionally, third parties accessing this data must adhere to privacy protections.

Through this regulation, the CFPB aims to enhance consumer choice and stimulate more competition within the financial sector.

The new rule spans 38 pages and includes over 500 pages of explanatory comments from the CFPB, addressing feedback received on the contentious regulation and the bureau’s responses. It has already led to a lawsuit filed by the Kentucky Bankers Association, the Bank Policy Institute, and a community bank in Lexington, Kentucky, alongside endorsements from consumer advocacy groups and indications of further regulations in the future. The lawsuit, filed in the Eastern District of Kentucky, asserts that the rule undermines established private data-sharing practices, increases cybersecurity risks, and imposes a complex compliance framework that could increase the likelihood of data breaches.

According to the CFPB, the rule could foster increased competition within the financial services sector, potentially reducing prices and interest rates. Consumers gain greater access to their own financial data, enabling them to share it with third-party providers more easily. This is intended to increase consumer choice, promote competition, and reduce reliance on entrenched financial institutions.

The new rule mandates that companies must, upon consumer request, share clients’ confidential information with banks and fintech companies offering alternative products, allowing consumers free access to their data. By broadening consumer access to their data, the CFPB aims to promote competition by lowering obstacles to switching financial providers. A secondary goal of the rule is to create a more competitive environment for fintech firms looking to enter the banking sector with innovative products and services. The rule also strengthens data protection standards at fintech companies to better secure customer information.

Under the finalized rule, banks and credit unions with assets under $850 million are exempt. The rule applies to all non-depository institutions and remains mostly unchanged from its proposed version. Implementation will be staggered based on institution size from 2026 to 2030.

However, critics argue that it might also increase the risk of fraud and scams, which are current issues for consumers and banks. The banking lobby has expressed concerns that the rule may compromise consumer data security and overstep the agency’s legal authority. Meanwhile, the American Fintech Council (AFC) criticized the rule as too limiting regarding consumer data provisions. Critics added that the rule compromises data security by requiring financial institutions to share sensitive information with third-party providers, many of whom lack the stringent oversight applied to traditional banks. Additionally, critics claim that banks are unreasonably restricted from refusing third-party access, limiting their ability to manage security risks effectively.

Rohit Chopra, Director of the U.S. Consumer Financial Protection Bureau, likened the rule’s impact to the regulations that allow mobile phone users to switch providers while retaining their numbers. He suggested this change would align U.S. payment systems with those of other advanced countries.

During a speech at a financial technology event hosted by the Federal Reserve Bank of Philadelphia, Chopra emphasized that the rule includes robust privacy safeguards and gives consumers significant control over their data. He stated that while a company can use consumer data to deliver requested products or services, it cannot use the data for unrelated purposes that the consumer has not agreed to.

How New Open Banking Rules Help Consumers Move Accounts, Access Better Rates, and Make Secure Payments?

The Personal Financial Data Rights final rule grants consumers more control over their financial data, aiming to boost choice and competition by enabling people to:

Switch providers for better service: Consumers can transfer their banking history to a new bank or fintech provider without facing fees or obstacles, making it easier to leave institutions with poor service.

Seek better rates on financial products: Consumers can compare rates and move their accounts to providers offering better terms, such as higher interest on deposits or lower loan rates. This rule also allows people with limited credit history, like young consumers, to access better credit options by using data on income and expenses from other institutions.

Make secure payments, including through “pay-by-bank” options: Consumers can securely share payment information, allowing for direct bank payments to merchants, peers, or across accounts, which may foster competition in the payments sector.

How Are Third Parties Limited in Data Use, and What Rights Do Consumers Have for Revocation and Deletion?

Third parties can only collect and use data directly for the product or service the consumer requests. Without explicit consumer consent, they are barred from retaining or repurposing data for unrelated activities, such as targeted advertising.

Additionally, consumers can revoke data access immediately, and data deletion becomes the default. Continued access requires reauthorization within one year, and the revocation process must be straightforward to prevent confusing or manipulative practices.

Conclusion

The CFPB’s final rule on open banking marks a significant shift in U.S. financial regulations. It offers consumers enhanced control over their financial data while aiming to increase competition in the sector. The rule empowers consumers to explore better financial products and switch providers without facing barriers by facilitating the secure transfer of personal data between banks and fintech companies.

While this regulation has sparked mixed reactions, support from fintech firms and consumer advocates, and concerns from traditional banking groups, it lays the groundwork for a more consumer-centered financial ecosystem. As larger financial institutions prepare for the 2026 implementation deadline, this rule could pave the way for future data rights and financial transparency developments in the U.S.

Direct-to-consumer brands are everywhere today, and they’re known for building strong, direct relationships with their customers. Focusing on unique shopping experiences, these brands stay memorable and often become customer favorites. Traditional brands and established retailers can learn a lot by studying how DTC brands stand out and connect with customers in a crowded market.

Recent statistics show that about 53% of consumers worldwide prefer purchasing online directly from brands because they perceive it as offering lower prices and better value than buying from third-party retailers. This preference is driving an increase in DTC sales.

To highlight this growing trend, we have compiled a list of the top 10 DTC brands in the US that are particularly noteworthy right now.

What Are Direct-to-Consumer Brands?

Direct-to-consumer (DTC) brands sell products straight to customers, bypassing third-party retailers or wholesalers. They manage all aspects of sales, including promotion, advertising, and customer support, which intermediaries typically handle. This setup gives DTC brands direct customer access, allowing them to control brand messaging, customer experience, and data collection.

DTC brands can gather customer feedback directly, informing product design, marketing strategies, and customer service. With this access to customer insights, brands can offer more personalized marketing, respond quickly to customer preferences, and strengthen brand identity. While DTC demands a greater commitment to marketing and support, it enables brands to retain full control over their market presence and customer interactions.

History and Strategy of Direct-to-Consumer Brands

DTC marketing originated long before the internet, dating back to early direct selling methods. In 1785, farmers began delivering milk directly to customers’ homes, cutting out middlemen. Later, in 1886, Avon used a network of female sales representatives to sell beauty products directly, establishing a successful model that endured over time.

The online shift to DTC took off in the early 2000s, with brands like Warby Parker, Bonobos, and Everlane leveraging e-commerce and social media to build online storefronts. These companies saw the Internet as a way to connect directly with customers on a large scale, bypassing traditional retail and creating brand experiences designed for online shoppers.

DTC brands resonate with modern consumers, particularly millennials, who value trust, authenticity, and personalized experiences. Common strategies include targeted emails, appealing packaging, and responsive customer service to build loyalty. Techniques like cart abandonment reminders increase conversions by re-engaging shoppers, while feedback loops give brands insights into customer preferences, helping them refine products and interactions.

The DTC model also enhances profit margins by eliminating retail markups, allowing brands to retain more revenue. This approach enables sustainable growth and greater flexibility to respond to market demands, making it a preferred model for brands focused on controlling customer relationships and pricing.

Top 10 Direct-to-Consumer Brands in the US

DTC brands have gained attention for their direct connection with customers and innovative product design, marketing, and engagement approaches. With e-commerce expanding and more consumers choosing to buy directly from brands, DTC companies have seen impressive growth, attracting strong customer loyalty and significant investment.

Below, we will highlight the top 10 DTC brands across various niches in the US, with insights into their monthly organic traffic as of November 2024 (source: Ahrefs), recent funding rounds, and a brief of each company to understand how these brands are still competitive in a dynamic market.

Lovevery, based in Boise, Idaho, focuses on improving early childhood development with well-designed educational toys and resources. Their main product, The Play Kits, is a subscription service that provides learning materials aligned with children’s developmental stages. These kits are developed with advice from child development experts, therapists, and specialists and are based on the Montessori method to encourage independent learning and development.

By 2024, Lovevery had grown to more than 375,000 subscribers worldwide, a 17% increase from the previous year. In 2023, the company’s subscription revenue was $170 million, contributing to a total net revenue of $221 million—a 21% increase from the year before. Lovevery’s products are available in 60% of US zip codes and 32 international markets, including recent expansions into Australia, Singapore, and New Zealand.

In March 2024, Lovevery was named one of Fast Company’s Most Innovative Companies in education. The company is committed to sustainability, using durable, organic, and sustainably sourced materials for its products. Lovevery also provides extensive support to parents to help them meet their children’s developmental needs.

Lovevery has raised $126 million in a Series C financing round, which will allow it to continue developing and broadening its product range.

Waterdrop, based in Vienna, Austria, is a DTC brand that offers “micro drinks”—small, flavored cubes that dissolve in water to encourage better hydration. These sugar-free cubes, made from natural fruit and plant extracts, are enhanced with vitamins and come in recyclable packaging. Waterdrop also partners with Plastic Bank to remove one plastic bottle from the ocean for each 12-pack sold, underlining its commitment to environmental sustainability.

The company aims to reduce plastic use and CO₂ emissions while promoting healthier hydration habits. In 2022, Waterdrop secured $70 million in funding to aid its expansion. By 2024, the company will operate over 40 retail outlets in Europe, the United States, and Singapore, including mall kiosks that provide cost-effective opportunities to explore new markets and products.

Led by founder and CEO Martin Murray, Waterdrop has broadened its range to meet diverse consumer needs. Its products include Microlyte, for exercise recovery, and Microenergy, which offers a natural energy boost. Additionally, the company sells a variety of innovative, environmentally friendly bottles and accessories, further committing to sustainability and user convenience.

Waterdrop’s innovative hydration solutions and commitment to environmental causes make it a notable entity in the wellness market.

Based in Milford, Connecticut, Athletic Brewing Company has become a prominent figure in the non-alcoholic craft beer market. The company produces various non-alcoholic beers, including IPAs, golden ales, stouts, and light beers, designed for consumers who want flavorful options without alcohol.

Beyond its main beer products, Athletic Brewing has expanded into the seltzer market with its DayPack Sparkling Water line, which includes hop-infused flavors as refreshing, non-alcoholic alternatives. By July 2024, Athletic Brewing raised $347.54 million across 13 funding rounds. The most recent round, a $50 million equity investment led by General Atlantic, placed the company’s value at about $800 million.

Athletic Brewing has seen considerable growth. It ranks among the top 20 US breweries by volume, with sales exceeding 258,000 barrels in 2023. The company’s products are distributed in over 75,000 locations throughout the United States and have reached international markets, including Canada and the United Kingdom.

The company’s innovative practices have earned it recognition, including a spot on TIME’s “100 Most Influential Companies” list for 2024. Athletic Brewing is dedicated to sustainability and community involvement through its “Two for the Trails” initiative, which donates 2% of sales to preserve and rehabilitate local trails.

Led by co-founders Bill Shufelt and John Walker, Athletic Brewing continues to shape the non-alcoholic beverage industry by offering quality products that cater to consumers pursuing healthier lifestyles.

BRUNT Workwear, founded by Eric Girouard and David Chernow, is a Boston-based DTC brand specializing in robust work boots, apparel, and accessories for tradespeople. The company aims to deliver high-quality, comfortable, and innovative workwear designed to meet the needs of various labor-intensive fields.

BRUNT’s product line features work boots engineered for comfort, flexibility, and durability in tough conditions. Additionally, the company offers a range of apparel and accessories designed for various work settings, ensuring that professionals have the necessary gear for their jobs.

As of September 2024, BRUNT Workwear has accumulated $44 million in funding across three rounds. The latest funding, a Series C round in May 2023, contributed $15.5 million.

Initially, BRUNT operated solely as a DTC brand, but in February 2024, it expanded its distribution by partnering with 23 retail partners. This expansion made its products accessible in over 110 stores across the United States, responding to customer demands for in-store purchasing options and extending the brand’s reach.

Alongside its retail growth, BRUNT released updated versions of its flagship work boots, the Marin and Bolduc collections. Based on customer feedback, these enhancements include better slip resistance, improved cushioning, and waterproof features to accommodate trade workers’ needs better.

BRUNT is dedicated to supporting the significant yet often underrepresented group of over 23 million US workers in the construction, installation, maintenance, and repair sectors. By emphasizing quality, comfort, and innovation, BRUNT strives to provide workwear that effectively supports professionals in their challenging roles.

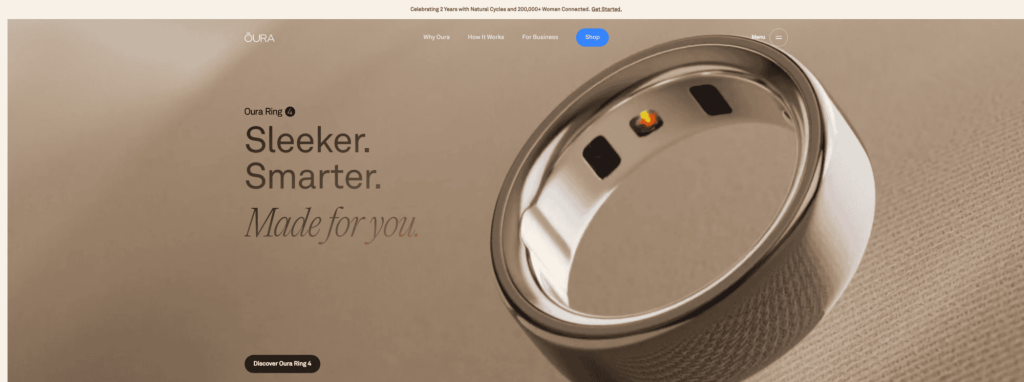

Oura, based in Oulu, Finland, has transformed personal health monitoring with its advanced smart rings. These rings track a wide range of health metrics, such as heart rate, blood oxygen levels, sleep patterns, and activity levels, all in a sleek and lightweight design.

In October 2024, Oura unveiled the Oura Ring 4, a notable development in wearable health technology. This new model features a full titanium body with recessed sensors to improve comfort and durability. It is available in sizes ranging from 4 to 15 and offers six finishes: Silver, Brushed Silver, Stealth, Black, Rose Gold, and Gold. The Oura Ring 4 uses “Smart Sensing” technology with 18 signal pathways, which enhances the accuracy of data collection, even if the ring moves on the finger. It boasts a battery life of up to eight days on a single charge, with a full recharge taking about 120 minutes. The ring is water-resistant up to 100 meters (328 feet), making it suitable for swimming and other water activities.

The ring integrates smoothly with smartphones, automatically syncing with health apps to provide real-time access to health data. The newly redesigned Oura App offers a more user-friendly interface, simplified tabs for daily insights, and tracking long-term health trends.

As of 2024, Oura has raised $148.3 million in funding, demonstrating strong investor support for its innovative health monitoring solutions. The company’s focus on user-centric design and cutting-edge technology has established it as a leader in the wearable health tech sector.

Glamnetic was founded in 2019 by Ann McFerran and Kevin Gould and is headquartered in Los Angeles, California. This beauty brand is known for its magnetic eyelashes and press-on nails.

Glamnetic focuses on making beauty routines easier by providing high-quality, easy-to-apply products that suit various personal styles and preferences.

The company promotes the idea that beauty should be easy, enjoyable, and accessible to everyone. It aims to deliver this through innovative and sustainable products and a strong commitment to meeting consumer demands.

Their mission is to enable individuals to feel confident and glamorous effortlessly, leveraging the impact of their products. Glamnetic also prioritizes accessibility and sustainability, aiming to impact the beauty industry positively. Remarkably, the company reached $50 million in revenue within its first year without external funding.

Based in New York, NY, Little Spoon was established by Angela Vranich, Michelle Muller, and Ben Lewis. The company has secured around $90 million in funding with five rounds.

The brand is dedicated to providing organic, clean, and wholesome food products designed for different stages of a child’s growth. They aim to make parenting easier by offering nutritionally rich and safe food choices, including infant purees, finger foods, toddler meals, and snacks. Little Spoon prioritizes quality and convenience, utilizing more than 100 organic ingredients and eschewing artificial additives. Their Clean Label Project certification affirms their commitment to safety, which ensures each meal and snack contributes to a healthy foundation for children.

As of September 2024, Little Spoon became the first US baby food brand to implement safety standards aligned with the European Union. Little Spoon set public limits and shared test results for heavy metals, pesticides, and plasticizers to increase transparency and trust in baby food safety.

In October 2024, the company broadened its product range to include organic oatmeal baby cereal for infants four months and older. This cereal is made from ancient grains like barley and millet and delivers 14 grams of whole grains and 13 essential vitamins and minerals per serving. It contains no added sugar, rice, or the top nine allergens.

Additionally, Little Spoon launched organic Puffs, a snack for babies over six months old designed to support self-feeding and fine motor skill development. These rice-free, easy-to-grasp puffs include Organic Kale Apple Curls and Organic Banana Pitaya Rings.

As of February 2023, Little Spoon had delivered over 27 million meals, serving hundreds of thousands of parents across the US.

Caraway, based in New York, NY, was founded by Jordan Nathan. The company has accumulated roughly $27.2 million in funding over two rounds, including one early-stage round. Caraway is known for its non-toxic, non-stick cookware, bakeware, and kitchen accessories. Their offerings include ceramic-coated cookware and stainless steel sets, focusing on safety, sustainability, and ease of use. The ceramic non-stick items are designed to minimize chemical exposure, providing a safer option than traditional cookware. The brand aims to merge stylish design with practical functionality to improve the cooking and baking experience while being environmentally responsible.

In November 2023, Caraway broadened its partnership with The Container Store, making its complete range of products available online at all US locations. This development established Caraway as the first cookware brand available at The Container Store, indicating the retailer’s strategic expansion into complementary categories. In September 2024, Caraway launched a new line of enameled cast iron cookware. This series is made for optimal heat retention, durability, and easy cleaning, offering consumers a high-performance, non-toxic cooking solution.

Prose, based in New York, NY, specializes in personalized hair care products. The company has raised $25.3 million over four rounds. Prose offers custom formulations for its main products, such as shampoos, conditioners, hair masks, and styling products. Customers undergo an online consultation that gathers details about their hair type, lifestyle, and preferences, allowing Prose to create products suited to each individual’s needs. Additionally, Prose offers a line of supplements designed to promote hair growth and scalp health.

The company prioritizes using natural ingredients, avoiding sulfates, parabens, and phthalates, and commits to sustainability with eco-friendly packaging and ethical sourcing practices.

Prose has seen a 192% increase in search growth over the last five years, showing a consistent increase in consumer interest. In 2024, Prose broadened its offerings to include personalized skincare products, extending its customization approach to meet individual skin care needs and demonstrating its commitment to providing tailored beauty solutions.

Embr Labs, founded by Sam Shames and Matthew Smith, has secured about $35 million in total funding. The company focuses on personal temperature management through its innovative Embr Wave product. This wearable device allows users to adjust their personal temperature, providing relief from hot flashes, aiding in sleep improvement, reducing stress, and increasing comfort. The Embr Wave utilizes cutting-edge thermoelectric technology, allowing immediate and tailored temperature adjustments.

In February 2024, Embr Labs released findings from a sleep study in partnership with the West Virginia University Rockefeller Neuroscience Institute. The research showed that users of the Embr Wave saw marked enhancements in sleep quality, such as decreased sleepiness, improved sleep quality, reduced heart rates at night, and higher sleep efficiency. The study also noted better cognitive function in the morning among participants. Dr. Pam Peeke, a senior clinical investigator at Embr Labs and co-author of the study, commented on the significant impact of the device, highlighting its ability to improve both the quality and physiological aspects of sleep, thereby enhancing life quality.

Embr Labs has earned accolades, including a SleepTech Award from the National Sleep Foundation and a place on the Foremost 50 list, which recognizes innovative consumer brands.

What Makes DTC Brands Unique?

DTC brands set themselves apart through several distinct attributes:

Brand Storytelling

DTC brands excel in articulating a compelling brand story beyond their products. They often emphasize their origins, the founder’s journey, or a pivotal value that propels the brand. This narrative helps build a distinct identity and connects with customers who share the brand’s values.

For instance, DTC brands in the wellness or sustainability sectors often discuss their motivations for creating products, which they say are in response to a market void of reliable, quality options.

Control Over Customer Experience

DTC brands manage all aspects of the customer experience, from the website interface to packaging and after-sales support. Owning direct communication channels enables them to provide personalized services and quickly adapt based on customer feedback. This comprehensive control helps ensure a consistent and customized experience for customers.

Direct Feedback Loop

DTC companies collect and analyze customer data independently of third-party retailers. This direct insight allows them to understand customer preferences, evaluate product performance, and identify improvement areas.

They can then refine products, launch new ones, and adjust their marketing strategies based on genuine customer input, making them more agile than traditional brands.

Unique Marketing and Branding Strategies

DTC brands frequently employ original, targeted marketing methods. Many utilize digital platforms, including social media and influencers, to connect directly with customers, designing campaigns that embody the brand’s character and appeal to specific demographics.

This strategy allows DTC brands to test unconventional marketing approaches and produce content that is often more authentic and engaging, particularly to younger audiences.

Transparency and Ethical Practices

Transparency is a hallmark of many DTC brands, driven by consumers’ interest in ethical practices and sustainability. These brands are typically forthright about their sourcing, production processes, and pricing.

Being transparent builds trust and sets DTC brands apart from traditional businesses, which may not be as open.

Mission-Driven Products

A clear mission beyond mere product sales defines many DTC brands. Brands emphasizing sustainability, wellness, or social impact integrate these principles into their products and marketing. This mission-centric approach attracts customers seeking to support brands that contribute to wider social or environmental objectives.

Community Building

DTC brands actively engage with their customers via social platforms, newsletters, and branded content, cultivating loyal communities. Many focus on interactive engagement, using social media to promote products, share customer experiences, and develop a sense of community among their followers.

Strong Customer Support

Direct access to customer data equips DTC brands to offer personalized support. They can directly manage complaints, returns, and inquiries, often resolving issues more efficiently than brands dependent on third-party sellers. Effective customer support boosts satisfaction and can enhance brand loyalty.

Innovative Product Development