Nuvei goes private following a $6.3 billion acquisition led by Advent International, with continued investment from CEO Philip Fayer, Novacap, and CDPQ. Nuvei Corporation, a fintech company based in Canada, confirmed the finalization of their planned arrangement under the Canada Business Corporations Act. The arrangement involved Neon Maple Purchaser Inc., a company established by Advent International, acquiring all issued and outstanding subordinate and multiple voting shares of Nuvei. Each share was purchased for $34.

Following this transaction, Nuvei’s subordinate voting shares have been removed from listing on the Toronto Stock Exchange as of November 18. Removal from the Nasdaq Global Select Market occurred on November 25.

Key Takeaways

- Nuvei Corporation Completes $6.3 Billion Privatization: In November 2024, Nuvei finalized its transition to a private entity through a $6.3 billion all-cash acquisition by Advent International. Shareholders received $34 per share, reflecting a significant premium over previous trading values.

- Maintained Leadership and Ownership Structure: Founder and CEO Philip Fayer, along with existing investors Novacap and CDPQ, rolled over substantial equity into the private entity. Fayer retains his roles as Chairman and CEO, ensuring continuity in strategy and operations.

- Delisting from Public Markets: Nuvei’s subordinate voting shares were delisted from the Toronto Stock Exchange and Nasdaq Global Select Market in November 2024, marking the company’s full transition from public to private ownership.

- Strategic Focus on Growth and Innovation: Backed by Advent, Novacap, and CDPQ, Nuvei aims to implement its Value Creation Plan, focusing on global expansion, advanced payment technologies, and enhancing customer relationships.

Nuvei Goes Private: A Look at the Key Details

In April 2024, Nuvei Corporation, a prominent Canadian payment processing company, announced its decision to become a private entity through a $6.3 billion all-cash transaction with Advent International, a global private equity firm. This arrangement allowed Neon Maple Purchaser Inc., a company established by Advent International, to acquire all the issued and outstanding subordinate voting shares and multiple voting shares of Nuvei Corporation.

This strategic move was completed in November 2024, marking a significant shift in Nuvei’s corporate structure while maintaining its existing leadership and ownership framework.

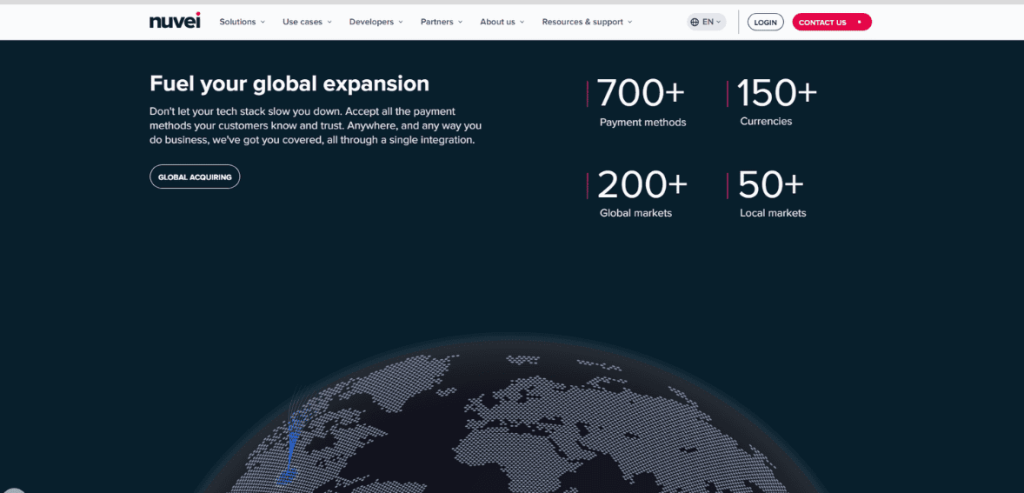

Founded in 2003 by Philip Fayer, Nuvei has established itself as a key player in the payment technology sector, offering a comprehensive suite of services, including global card acquiring, alternative payment methods, crypto payments, fraud and risk management, and analytics. Operating in over 200 markets and supporting 150 currencies, Nuvei serves a diverse clientele, including notable brands such as Shein, New Balance, and Microsoft.

The agreement to take Nuvei private was first announced on April 1, 2024. Under the terms of the deal, shareholders received $34.00 per share in cash, representing a premium of approximately 56% over Nuvei’s closing share price of $21.76 on March 15, 2024, and a premium of about 48% over the 90-day volume-weighted average trading price as of that date. This valuation positioned Nuvei at an enterprise value of approximately $6.3 billion.

A notable aspect of this transaction was the continued involvement of existing Canadian shareholders. Philip Fayer, the company’s founder and CEO, along with investment firms Caisse de dépôt et placement du Québec (CDPQ) and Novacap, chose to roll over a substantial portion of their equity into the new private entity. Under the terms of the agreement, Philip Fayer and the investment funds, collectively referred to as the Rollover Shareholders, exchanged their shares for a mix of cash and equity in the purchasing company or its affiliate.

This was executed in line with the stipulations of the Plan of Arrangement and individual rollover agreements with each shareholder. Following the arrangement, the company is now a wholly-owned subsidiary of the purchaser, with ownership and control distributed approximately as follows: Advent International holds about 46%, Philip Fayer 24%, Novacap 18%, and CDPQ 12%.

Philip Fayer, the founder and CEO of Nuvei, has converted about 95% of his shares and will remain one of the company’s major shareholders. He will also maintain his positions as Chairman and Chief Executive Officer, overseeing all operational aspects of the company. The existing leadership team at Nuvei will also stay on in their current roles.

In the announcement, Fayer expressed enthusiasm about starting a new phase with Advent, Novacap, and CDPQ, emphasizing a commitment to their long-term strategy aimed at increasing global customer revenue. He noted that for over 20 years, the company has offered essential solutions that support customer growth. Fayer assured that this commitment would persist as they aim to strengthen customer relationships through the provision of modern, adaptable, and specifically designed technology.

Fayer added that an important element of this next phase is the rollout of their Value Creation Plan, a detailed strategy to enhance their operations and capitalize on opportunities for rapid growth. Advent is joining forces with long-term investors Novacap and CDPQ, who continue to be significant stakeholders and share a belief in Nuvei’s dynamic and prosperous future.

David Lewin, Lead Senior Partner at Novacap, commented that since 2017, they have had the opportunity to support Nuvei’s management in pursuing its ambitious strategy for global growth. With a leadership team that consistently fosters innovation and cultivates significant partnerships across various industries, Nuvei has positioned itself as a leading fintech player in essential sectors with prospects for sustainable growth. As Nuvei enters an exciting phase of expansion, they are eager to enhance their partnership and discover new opportunities to generate enduring value for all stakeholders.

Kim Thomassin, Executive Vice-President and Head of Québec at CDPQ stated that since their initial investment in Nuvei in 2017, CDPQ is proud to have supported the growth of this Québec-based fintech leader, particularly through its global acquisitions. They are pleased to support Nuvei once more as it begins a new phase of its development, working with esteemed partners like Advent and continuing shareholders such as Philip Fayer and Novacap.

Bo Huang, Managing Director at Advent, expressed enthusiasm about initiating this partnership and supporting Nuvei’s expansion through strategic investments and acquisitions to enhance its global customer service as a contemporary payments partner.

The payment for the shares has been transferred by or on behalf of the Purchaser to the TSX Trust Company, serving as the depositary under the arrangement. Payments to the former shareholders of the company will be made as soon as possible after today’s date, or, for registered shareholders, following the receipt of a properly completed and signed letter of transmittal along with the necessary share certificates and/or DRS Advices representing the previously held shares.

As a result, Nuvei Corporation completed its go-private transaction on November 15, 2024. Consequently, the company anticipated that its subordinate voting shares would be delisted from the Toronto Stock Exchange (TSX) around November 18, 2024, and from the Nasdaq Global Select Market around November 25, 2024. The TSX confirmed that Nuvei’s shares were scheduled for delisting at the close of trading on November 18, 2024.

About Nuvei

Nuvei, based in Montreal, Canada, is a financial technology company that focuses on global payment processing. It provides businesses with various payment solutions such as card issuing, banking services, risk management, and fraud prevention, enabling them to process payments across different markets through a single integration.

The company was listed on the Toronto Stock Exchange and Nasdaq under the ticker symbol NVEI before it went private.

Conclusion

Nuvei Corporation’s transition to a private entity, finalized in November 2024, marks a pivotal development in the fintech sector. The $6.3 billion all-cash transaction, led by Advent International with continued investment from founder Philip Fayer, Novacap, and CDPQ, underscores a strategic commitment to Nuvei’s long-term growth. By delisting from public markets, Nuvei aims to enhance its operational flexibility, enabling a concentrated focus on delivering advanced payment solutions across its extensive global network. This move is anticipated to facilitate the implementation of the company’s Value Creation Plan, designed to optimize operations and accelerate growth.

The sustained involvement of existing shareholders, particularly Philip Fayer, who retains a significant ownership stake and continues as Chairman and CEO, ensures continuity in leadership and strategic direction. This continuity is expected to strengthen Nuvei’s position in the competitive payment technology landscape. The collaboration with Advent International and the continued support from Novacap and CDPQ are poised to drive Nuvei’s mission to provide modern, flexible, and purpose-built payment technology solutions.