Before the market opened, Shopify’s stock price jumped 21% as Shopify’s AI investments and cost efficiencies propel return to profitability. Shopify earnings for the third quarter surpassed predictions, showing higher growth. The company reported a revenue of $1.71 billion, which is a 25% increase compared to the year prior, which exceeded the expected $1.67 billion. Additionally, Shopify’s monthly recurring revenue reached $141 million, marking a 32% rise YOY, coming close to the projected $141.2 million.

The subscription-based revenue amounted to $486 million, representing a 29% boost YOY. Furthermore, Shopify witnessed the value of goods sold through the company over the quarter stood at $56.2 billion, indicating a growth of 22% compared to last year. In terms of profitability, Shopify presented earnings of $0.24 per share this quarter, showcasing an improvement from last year’s loss per share of $0.20 and surpassing expectations set at $0.14 per share.

The volume of payments processed through Shopify experienced the wave too, reaching a total value of $32.8 billion during this period—an increase of 31% YOY and exceeding estimates that were set at around $31.33 billion.

Key Takeaways

Shopify’s AI Investments and Cost Efficiencies Propel Return to Profitability, leading to a substantial increase in revenue, profits, and monthly recurring revenue. The success of the company can be credited to its strategic partnerships and the implementation of AI tools.

Shopify’s financial management has been positively influenced by reducing expenses through carefully planned workforce reductions and the divestment of specific business segments. These actions demonstrate the company’s dedication to improving cost efficiency while maintaining an approach to cautious hiring practices.

While the adoption of AI presents hurdles in many ways, the reason why Shopify’s AI Investments and Cost Efficiencies Propel Return to Profitability is all because of better planning and execution. Investors are keeping an eye on Shopify’s efforts to attract more businesses and utilize AI in order to maintain profitability over the long term.

Shopify’s all-inclusive commerce platform is designed to meet the needs of businesses of all sizes, offering tools for the management of online operations. The fact that known global brands have embraced it demonstrates its dependability and ability to adapt, establishing itself as a prominent player in the eCommerce industry.

AI Integration Fuel Shopify’s Remarkable Third Quarter Rise

Canada-based Shopify’s AI investments and cost efficiencies propel return to profitability. The increase in profits was a result of cost management and the integration of AI, which played a crucial role in attracting more businesses to utilize its platform. Shopify has introduced AI-powered tools like Shopify’s Magic Suite and Sidekick app to stay competitive in the competitive online market while also improving its delivery speed.

This online commerce facilitator, renowned for assisting businesses in launching their online stores, announced a profit of $0.55 per share, marking a sharp shift from last year’s loss of $0.12. Additionally, Shopify’s strategic collaborations with known brands have yielded higher results too. Notably, popstar Taylor Swift chose Shopify as the platform for selling her Eras Tour merchandise, resulting in record-breaking sales and website traffic on its launch day.

Shopify’s AI investments and cost efficiencies propel return to profitabilityadd to their summer wins, rapper Drake opened his new store, Drake Related, on Shopify. The company didn’t stop there, announcing in August a notable collaboration with Amazon. This new app within Shopify’s platform will allow US sellers to offer Amazon’s Buy with the Prime feature directly on their sites, a first outside of Amazon’s website.

The company in Ottawa announced that it earned $ 1.7 billion in revenue for the quarter ending 30th September. Its net income soared to $718 million, which includes a substantial $555 million gain from its investments. This is a sharp turnaround from the $159 million loss reported in the same quarter the previous year.

Shopify’s President Harley Finkelstein highlighted their strategic approach over the past quarters, focusing on achieving a balance between big operational goals and financial prudence. She spoke about shaping a new future for Shopify, indicating a transformative phase for the company.

Shopify has been adapting and evolving, aiming to recapture the strong growth it experienced as Canada’s most valuable company during the early days of the COVID-19 pandemic. This year, Shopify introduced a set of AI tools targeted at businesses using its platform, aiming to streamline their operations. At the same time, Shopify is enhancing its efficiency by automating tasks across its workforce.

These new AI offerings empower merchants to handle administrative duties and creative tasks, like answering customer questions or promoting their products, more effectively. Finkelstein emphasized their focus on blending human creativity with technological efficiency, noting that AI plays a crucial role in this synergy and will be a key component in Shopify’s ongoing strategy.

Strategic Workforce Reductions Drive Shopify’s Cost Efficiency In Q3

Although Shopify’s AI investments and cost efficiencies propelled return to profitability, it also saw its operating costs drop by 23% to $779 million in the third quarter. The company’s CFO, Jeff Hoffmeister, mentioned that this decrease largely came from reducing the number of employees.

This past summer, Shopify made a big decision to cut down its workforce by nearly 20%, marking the second time in under a year they’ve had to let employees go. Hoffmeister explained to investors that these tough decisions were key to improving the company’s financial management. He highlighted that the money spent on stock-based compensation also went down to $102 million this quarter from $150 million the previous year.

Jeff also noted that while they are still bringing on new people for critical roles, they’re doing so more cautiously, which has helped keep salary expenses lower than expected.

The company had been feeling the weight of costs from its delivery operations. Hoffmeister pointed out that selling these parts of the business to Flexport has helped reduce expenses somewhat. He mentioned that it’s still too early to tell the full effect of this deal, and he chose not to share financial specifics about it when asked.

The Hurdles And Prospects For Adopting AI Investments

For Shopify, introducing AI tools might just be what sets it apart, but getting businesses on board with this new tech could be a bit tricky. With a slowdown in demand and some businesses not too keen on trying new things, it might take some time before AI starts to pay off. Yet, if Shopify can prove that AI makes things more efficient, they could find new ways to make money from these innovations down the line.

As Shopify’s AI investments and cost efficiencies propel return to profitabilityInvestors are keeping an eye on how Shopify plans to draw in bigger companies and use AI to push their growth further. The company’s game plan to bring more businesses onto its platform and boost their sales is vital for staying on top. Plus, Shopify’s knack for staying innovative and outpacing rivals in the online market will play a big role in keeping its profits up.

About Shopify

Shopify is an all-in-one commerce platform that’s perfect for small and medium-sized businesses looking to spread their wings online and in person. It’s like a multipurpose channel for selling, letting business owners set up and run their shops across different channels — think websites, mobile, social media, online marketplaces, and even physical stores and pop-up shops. What’s best about Shopify is that it gives sellers a unified view of their business from one spot.

For those running online shops, Shopify comes packed with tools that make things like marketing, chatting with customers, handling payments, and shipping orders a whole lot easier. Plus, they’ve got this cool App Store that came about because Shopify lets tech-savvy users build their apps for Shopify stores and then sell them right in the App Store.

Shopify isn’t just for the small guys, though. It’s built to be super reliable and can handle the big leagues, too. Right now, it’s the engine behind over 800,000 businesses in roughly 175 countries. Big names like Red Bull, Tesla, GE, Nestlé, and Kylie Cosmetics trust it to power their online sales.

Conclusion

Shopify’s recent financial performance, characterized by substantial revenue growth, increased profitability, and enhanced cost efficiency, underscores the effectiveness of its strategic initiatives. The successful integration of AI tools and careful cost management has propelled the company to achieve remarkable results, surpassing market expectations.

The company’s ability to streamline operations and enhance its platform’s capabilities through AI-driven tools has contributed significantly to its profitability. Additionally, Shopify’s proactive approach to managing costs, including strategic workforce reductions and divestment of certain business segments, has further solidified its financial standing.

While the adoption of AI presents challenges, Shopify remains focused on demonstrating the long-term benefits of this technology to its user base. With a commitment to innovation and a comprehensive commerce platform catering to businesses of all sizes, Shopify is well-positioned to sustain its leading position in the competitive eCommerce landscape.

As Shopify continues to steer the busy “AI’s” market environment, its dedication to technological advancement and its ability to adapt to evolving industry trends will remain pivotal in driving its future growth and success. With its proven track record and global trust among businesses of varying scales, Shopify remains a key player in empowering businesses to thrive in the digital world.

Payment fraud poses a significant threat across industries, with pharmaceuticals, manufacturing, and finance being particularly susceptible. It is imperative for leaders in information technology and cybersecurity, including managers and team leaders, Heads of the ITs, CISOs, and IT managers, to stay informed about the current market of payment fraud, its associated costs, and the effective prevention strategies to comply with their existing fraud management strategies.

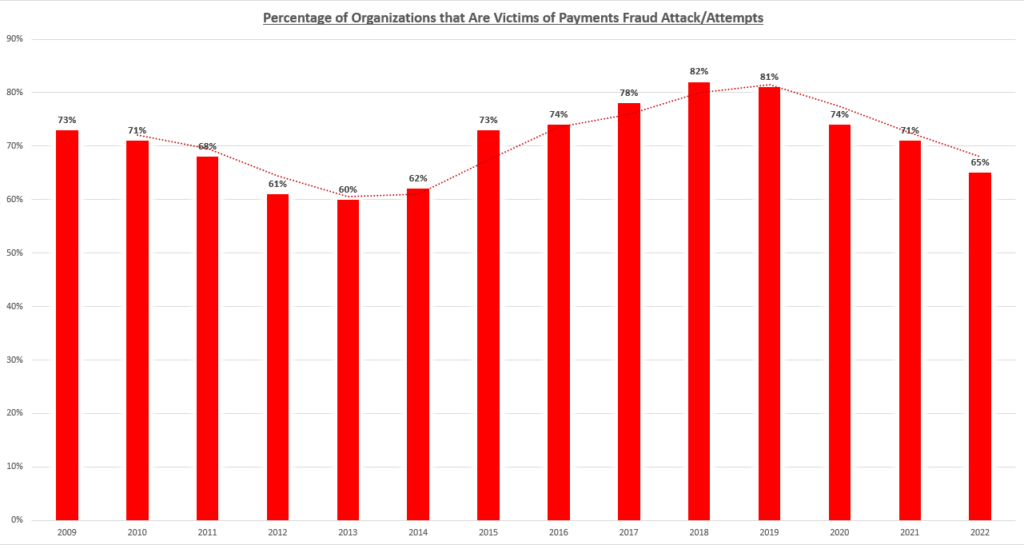

The AFP Payments 2023 Survey reveals a concerning trend, indicating that 65% of organizations fell victim to payment fraud in 2022. What’s even more alarming is that nearly half of these organizations (about 44%) were unsuccessful in recovering any of the pilfered funds.

Source: 2023 AFP Payments Fraud and Control Survey

Fraud management today is one of the most important aspects for businesses that are connected online and aiming to get rid of payment frauds effectively. Small and large businesses use specialized tools to prevent payment fraud and practice some important precautions and protocols for safety. These specialized tools and practices are crafted to proactively prevent, detect, and mitigate fraudulent activities. In this article, we will thoroughly discuss the core concepts of fraud management, explore the prevailing fraud management trends in 2024, and provide valuable insights to equip businesses in their battle against payment fraud.

What Exactly Is Fraud Management?

Businesses and organizations face diverse forms of fraud, perpetrated by employees, customers, third parties, vendors, and other entities like hackers. Annually, companies incur substantial financial losses amounting to billions of dollars due to fraudulent activities. The proliferation of online channels has particularly heightened the risk, impacting sectors such as e-commerce, banks, airlines, pharmaceuticals, and manufacturing. In response to these challenges, fraud management emerges as a systematic approach to handle fraud effectively within an organization or a company. Effectively reducing fraud requires early detection. It also requires a proactive method widely adopted by using analytics models with predictive capabilities to identify vulnerable transactions.

Providers specializing in fraud protection, whether high risk merchant account providers, payment service providers or dedicated fraud prevention software providers play a crucial role in preventing fraudulent behavior. They stay abreast of the latest fraud trends, employ AVS (Address verification), implement anti-fraud tools, and meticulously manage and analyze transactions, utilizing a combination of automated and manual order screening. Early detection of fraud not only minimizes revenue loss but also enhances customer satisfaction and retention. This multifaceted approach is essential for businesses fighting fraud.

Before rolling out an anti-fraud program, a crucial step involves assessing the organization’s vulnerabilities and pinpointing areas susceptible to fraudulent activities. A thorough risk assessment and analysis provide valuable insights into the organization’s weak points. Moreover, it digs deeper into the core to understand the likelihood, nature, and associated costs of potentially fraudulent activities.

Based on the assessment results, a risk-tolerance limit can be established to align with the organization’s specific needs. This approach proves beneficial by quantifying the risk assessment and enabling the company to concentrate its efforts on addressing more impactful and damaging instances of fraud.

Fraud management governance forms the framework of rules, practices, and processes dedicated to fraud management within a company. A robust and transparent fraud management governance policy serves as a deterrent to potential fraudsters, highlighting C-level commitment to minimizing and controlling fraud. Key elements of a comprehensive fraud management governance policy include:

● Promoting a culture of increased awareness among employees regarding fraud.

● Upholding the quality of each practice, risk, and rule process employed within the organization.

● Implementing ongoing surveillance for identifying and handling potential frauds.

● Conducting research on market trends in fraud prevention and mitigation technology.

● Providing clear descriptions of the process involved in investigating instances of fraud.

Aligned with the principles of good governance, each facet of a fraud management governance policy should be well-documented, appropriately delegated and designated, and easily accessible. Ideally, an individual within the organization should take the lead in spearheading the efforts related to fraud management governance. This comprehensive approach ensures a proactive stance in managing and mitigating fraud within the company.

Proactive Fraud Prevention

You’ve likely heard the age-old phrase, “prevention is always better than the cure,” and in fraud management, this saying holds true. Once a comprehensive fraud management plan is in place, and you’ve identified and assessed potential risks within your organization, the next crucial step is the implementation of controls, policies, procedures, and software. The primary aim is to prevent or significantly reduce the likelihood of fraud. Direct your efforts toward mitigating all three components of the fraud triangle:

● Understand the financial incentives that might drive individuals to commit fraud.

● Explore ways in which someone could rationalize committing fraud against your company.

● Assess and address the ease with which someone could commit fraud and go unnoticed.

By focusing on these key aspects, your organization can actively reduce the risk of fraud and fortify its defenses against potential threats. This proactive approach aligns with the wisdom encapsulated in the age-old saying, fostering a culture of vigilance and resilience in the face of fraud risk.

Fraud Detection

The efficacy of an organization in detecting fraud hinges on the proficient implementation of Reporting and Controls. These two strategies not only serve as preventive measures but also play a pivotal role in detecting fraudulent activities.

Controls, essentially tools, act as early warning systems for employees, signaling potential fraudulent behaviors. Deployment of these controls across various organizational layers is vital. However, employers must be well-versed in understanding how these controls operate and when to evaluate them.

On the other hand, Reporting stands as a critical facet of fraud detection. When correctly implemented, reporting mechanisms can identify and report fraudulent activities, safeguarding organizations from compromising sensitive information. The reports should encompass all essential details, including date and time stamps. This dual approach of controls and reporting forms a robust foundation for organizations aiming to enhance their fraud detection capabilities.

Monitor and Report

The effectiveness of an organization’s fraud management strategy significantly influences its overall success. Achieving this efficiency requires regular reviews and monitoring to ensure that the policies and practices within the fraud management strategy seamlessly align with the company’s vision and remain updated.

Additionally, a crucial step involves actively reporting any identified fraudulent activities to someone capable of addressing the issue promptly. This proactive reporting mechanism catalyzes timely action, preventing organizations from incurring substantial losses.

By adhering to these five stages during the implementation of the organization’s fraud management program, businesses can enhance their capabilities to detect and prevent suspected fraud, both internally and externally.

Benefits Of Effective Fraud Management Plans

● Safeguarding Against Severe Losses

Instances of fraud leading to substantial losses, which can jeopardize a company’s very existence, are fortunately rare but not unheard of. Whether it’s financial setbacks or the erosion of trust, the aftermath of such fraud leaves lasting scars.

The encouraging news is that the overall cost of implementing a fraud management strategy is not exorbitant, providing a shield against potential future losses.

● Gaining Valuable Insights

A well-structured fraud management strategy, when put into practice, offers valuable insights into an organization’s vulnerabilities. It serves as a beacon, illuminating both strengths and weaknesses that require attention. Armed with this knowledge, organizations can construct a more effective and efficient fraud management program, mitigating risks and fostering resilience.

● Instills Confidence and Attracts Opportunities

A well-executed fraud management strategy not only enhances control over an organization’s destiny but also instills a heightened sense of confidence. This increased confidence makes the organization more appealing to investors, business partners, and other potential opportunities.

Top Fraud Management Trends And Insights 2024

Scam Blocking Techniques and Tools Are Getting Attention

The need for a systematic approach to address the prevalence and complexity of scam trends is crucial. Relying solely on old security measures proves insufficient against the ever-evolving tactics employed by scammers. Businesses must acknowledge the significance of multi-layered strategies integrated with necessary tools and services to effectively safeguard against various types of scams.

A multi-layered fraud management approach integrates multiple security measures, each serving as a line of defense against different facets of fraudulent activities. This approach provides a comprehensive defense strategy that is not only more robust but also adaptable, thereby mitigating the risks posed by sophisticated phone scams.

To optimize efforts in preventing fraud, businesses and organizations must efficiently coordinate diverse risk signals, customer information, and data points. Through the consolidation and analysis of this information, organizations can devise a unified and well-rounded response. This approach aims to minimize risk, reduce customer friction, and mitigate the associated costs of prevention.

AIT SMS Fraud on the Rise

AIT, or A2P or International Traffic, represents a pervasive form of SMS fraud that orchestrates a surge in fake traffic through mobile applications or websites. Recent insights identify AIT as a prominent threat that individuals covering fraud prevention should be aware of, as projections are indicating its further escalation in 2024.

Here’s a common AIT scenario:

A fraudster makes a bot designed to generate fake accounts.

The bot initiates the delivery of OTP SMS to various mobile numbers.

The fraudster collaborates with a rogue entity to intercept the inflated traffic, avoiding actual message delivery to end users.

Together, they lay claim to the revenue generated, sharing the ill-gotten profits.

This cycle repeats, inflating revenues and manipulating conversion statistics.

As the application owner, you may find yourself burdened with the bill, even though the messages were technically delivered by the fraudsters. Fraudsters often target long-distance locations, as international destinations with higher delivery costs offer the most lucrative returns. Recent data reveals that over 43% of businesses have encountered AIT in recent years, with 60% of business owners seeing a noticeable acceleration in this threat.

To steer clear of AIT scams, businesses should opt for a trustworthy communication platform equipped with effective fraud prevention tools. One such tool is the Verify API, which allows you to enforce Two-Factor Authentication (2FA) for all A2P messages containing sensitive information. This proactive measure enhances security and safeguards your communication channels from fraudulent activities.

Escalation of Wire Frauds

Among the concerns that keep certified fraud examiners and anti-fraud professionals up at night, wire fraud stands out as a formidable adversary. Unlike schemes centered around credit lines and gift cards, wire fraud perpetrators are now setting their sights on the real estate market, participating in escrow closings.

Examining the losses, particularly in real estate, reveals a staggering 700% growth in wire frauds in the last five years, according to recent FBI data. Wire fraud poses a unique challenge because while institutions gather ample information about the payers initiating transactions, they possess scant details about the payees receiving the funds.

This gap in knowledge prompts fraud risk experts to explore improved methods for gaining insights into entire payee ecosystems. To safeguard against wire transfer fraud, it’s advisable to verify each transaction meticulously before releasing funds. Avoid contacting numbers provided in emails or on websites for verification. Instead, rely on the initial transaction information you received—trusted numbers that have been used in previous interactions before discussing financial matters. This practice enhances security and reduces the risk of falling victim to fraudulent activities.

Frauds Taking its Way Through ChatGPT

Fraud in the form of service is fueling the industrialization of fraudulent activities, posing a significant challenge to anti-fraud efforts. While cutting-edge technologies have been deployed to combat real-time transaction fraud and online scams, there’s been a concerning neglect of defenses against traditional, P2P, and physical frauds.

This neglect has given rise to a troubling trend where fraudsters are using modern tech integrated with older fraud schemes. Practices such as deposit and check fraud, and intercepting emails to pilfer information regarding your PII and credit cards also have become more sophisticated.

In some reported instances, criminals target unarmed mail carriers, they plunder for paper checks and items containing PII (Personally Identifiable Information), which are then sold in the black market, preferably the dark web. This results in exploitation for account takeovers, identity theft, and manipulation of checks by altering the amounts before depositing them into the mule accounts for laundering.

The integration of technologies like ChatGPT accelerates criminal activities. For example, a large-scale data breach at a retailer yields millions of card numbers, which fraudsters sell on the dark web, categorized by card type. The buyer of these card numbers can leverage ChatGPT to automate routines for swift and repetitive card-not-present attacks at an astonishing speed.

The key concept in understanding Fraud in the form of service is the division of labor among various players. With distinct groups involved in selling, exploiting, and buying PII, fraud transforms into a full-fledged industry. Fraudsters can navigate and operate within this industry more swiftly and easily than anti-fraud professionals can counteract. Countering industrialized fraud is poised to become a top priority for anti-fraud professionals in the upcoming year.

Phone Scammers Are Now Global

Phone scammers are adopting new tactics, using artificial identities to deceive individuals into thinking their calls are from reputable sources or friendly contacts. Employing urgency, fear, and empathy, scammers aim to manipulate emotions and gain unauthorized access to sensitive information through social engineering — sophisticated psychological attacks.

Expanding their reach globally, scammers now use local-number telecom technology, intended for global business-customer connections, to mimic phone numbers across different countries. This approach allows them to target a wider audience while remaining untraceable.

Businesses can leverage AI surveillance tools to identify and bar phone numbers associated with fraudulent activities, providing a proactive defense against evolving phone scam strategies.

Conclusion

As organizations grapple with the escalating threat of payment fraud, staying aware of the top fraud management trends in 2024 becomes imperative. The AFP Payments 2023 Survey underscores the alarming prevalence of payment fraud, emphasizing the urgency for robust fraud management strategies for 2024.

Through comprehensive governance policies, proactive prevention, vigilant detection, and strategic reporting, organizations can fortify their defenses. Embracing evolving trends such as scam-blocking techniques, addressing AIT SMS fraud, countering wire fraud escalation, and tackling fraud in the form of service will be crucial in navigating the evolving landscape of fraud prevention.

If you are planning to take your first step in your investment journey then you are at the right place. Everyone wants to be rich but most of people do not know much about investment. Unlike before, today we have a huge wealth of information over the internet. There are dedicated investment-related websites and blogs. There are numerous experts on different social media platforms who can guide you in learning how to invest. But, the major challenge is where to begin and which source to trust. This article will guide you with a well-researched list of the best investment websites for beginners in 2024 so that you can start your journey without ambiguities.

These investment websites provide you with the right tools and knowledge necessary to make informed investment decisions and effectively utilize their platforms. From educational materials to robo-advisors and trading simulators, an ideal investing website offers a multitude of valuable features. Let’s see some of the best investment websites tailored for beginners and grasp how to leverage them efficiently. But before we head-start, Let’s see how to select the best platform.

What Are Investment Websites?

Investment Websites serve as a means for individuals to acquire securities like bonds, ETFs, and stocks offering a valuable avenue for achieving financial objectives. Whether it is saving for specific goals such as building wealth or a child’s education over time, brokerage accounts are versatile. In addition to the primary function of facilitating investments and savings, these accounts often provide supplementary features, including access to research reports and various tools.

While an investment website allows you to withdraw funds at your discretion, it’s crucial to note that any gains on your investments may incur taxes, depending on your income.

Selecting The Right Investment Websites For Beginners

While there isn’t an all-purpose broker or investment website, certain crucial factors should guide your decision when selecting a stock broker for beginners.

Cost Structure: For beginners, the ideal brokerage accounts impose no commissions on online stock and ETF trades, which are typically the focus. However, be aware that some brokers may charge commissions or fees for more intricate transactions like options trading, mutual funds, and other products.

Account Minimums: Consider the minimum deposit requirement some stock brokers may have, ranging from $5 to $500 and sometimes even for free. The best investment accounts, in our view, eliminate account minimums. It’s worth noting that a few brokers may not permit fractional share investing, so ensure you have enough funds to acquire at least one share of an ETF or stock. Opt for low brokerages that enable anyone, even with limited capital, to initiate their investment journey.

Diversification of Funds: For many, delving into individual stocks, especially for beginners, might not be the optimal choice. The preferred investing platform for beginners should provide access to low-cost exchange-traded funds and fee-free mutual funds, offering a smart investment approach without necessitating an extensive understanding of the stock market.

Account Options: When selecting stock brokers, you have the option of a cash account or a margin account:

Cash account: You can use only the money available in your account.

Margin account: Borrow funds from your broker for investments. However, trading on margin carries risks, making it less advisable for novice and rookie investors. Margin interest rates are typically high, particularly in an environment of rising rates.

Top Investment Websites Right Now

1. Fidelity

Fidelity Investments stands out for its robust educational platform, but its real strength lies in its research capability. With a suite of top-notch calculators and research tools. Fidelity makes it simple for novice investors to identify the most suitable investing opportunities and strategies. For those unsure of where to start, Fidelity’s 200-plus investor centers offer in-person assistance.

As a low-cost broker, Fidelity impresses with no account minimums and $0 commissions on US ETFs, options trades, and stock. Investors benefit from competitive margin rates, potentially as low as 9.25%. Fidelity goes further in the mutual fund domain, offering zero-expense-ratio mutual funds with no minimum investment or account opening requirements.

To enhance the investor journey, Fidelity provides both a hybrid robo and robo-advisor solution, requiring only a $10 initial investment. If your balance is below $25,000, Fidelity waives these fees; beyond that, fees are 0.35% per year.

Pros:

Fidelity’s array of services is unmatched by many other brokers.

Beginners will find Fidelity approachable, while detail-oriented investors can customize their experience extensively.

As a privately owned entity, Fidelity has earned a solid reputation through decades of reliable client service.

Cons:

Some brokers outshine Fidelity in active trading capabilities.

The platform layouts may feel a tad dated on occasion.

E*Trade, with its $0 commissions for stocks and ETFs, stands out as one of the premier brokers for novice investors seeking an excellent trading platform and a diverse range of investment options. E*Trade provides a broad spectrum of account types, making it a well-rounded brokerage that caters to the majority of investors’ requirements.

For those new to investing, E*Trade offers an exceptional collection of tools and educational resources, facilitating a responsible start to investing. Notably, unlike some other online-based brokers, E*Trade boasts a physical branch network, offering beginners the option of in-person assistance if needed.

Pros:

Engaging features and tools that can be quite addictive.

The online POWER E*TRADE excels in catering to newbie traders.

Provides Morgan Stanley with thorough research.

Cons:

Does not support cryptocurrency trading.

Live data necessitates a $1000 minimum balance in the account.

Experienced traders might lean towards downloadable desktop platforms.

If you’re new to investing, JPMorgan’s platform is designed with user-friendliness in mind, featuring $0 commissions, even on mutual funds. While most brokers have zero fees for transactions for commission-free investing in specific funds, JPMorgan’s rare offering of $0 commissions on all mutual funds sets it apart.

For existing Chase customers with bank accounts or credit cards, JPMorgan Self-Directed Investing proves to be a particularly appealing choice. The app consolidates the management of all Chase accounts in one place. Notably, J.P. Morgan extends its appeal with an excellent robo-advisor platform accessible through the app. This makes it an intelligent choice for beginners looking to automate some investments while still retaining control over their stock portfolio. If you’re in search of a beginner-friendly brokerage account, JPMorgan’s investing platform is worth considering.

Pros:

JPMorgan Self-Directed Investing provides Chase Bank customers with a convenient avenue to invest in stocks, ETFs, options, bonds, and mutual funds.

The firm is recognized among our top brokers for banking services in 2023.

JPMorgan’s proprietary research often delves more deeply than the third-party research available through many other brokers.

Cons:

The platforms offered by JPMorgan are basic, lacking the advanced tools preferred by serious investors and traders, who may find more sophisticated options elsewhere.

Website navigation can be a source of frustration.

4. Merrill Edge

Merrill Edge, the online brokerage associated with Bank of America, offers a robust selection of $0 minimum investment options and research tools through a user-friendly platform. It proves to be an excellent choice for Bank of America customers, thanks to its seamless integration with the bank’s services and accessibility to various financial products.

In collaboration with Morningstar, Merrill Edge presents an Investing Classroom featuring short courses covering funds, stocks, ETFs, bonds, and portfolio types. This feature contributes to its status as one of the best investing websites. Each course includes quizzes to assess your knowledge and reinforce your learning. Don’t overlook the webinar series, delving into topics ranging from financial psychology to sustainable investing.

The Tools section provides resources to assist in number-crunching for college planning, retirement goals, and general personal finance. Users also gain access to the BofA Research platform, offering market insights, analysis, and research reports from Bank of America.

Pros:

Dynamic Insights, Portfolio Story, and the Fund and Stock Stories stand out as top features, especially for everyday investors who have benefited from $0 commission stock trades.

Merrill Edge provides access to high-quality Bank of America Securities proprietary research.

The platform boasts a premium design feel.

Cons:

Certain site elements may experience delays in loading.

Merrill does not offer services in cryptocurrencies, futures, foreign exchange, fractional shares, or paper trading.

5. Charles Schwab

An influential player in the brokerage landscape, Charles Schwab played a pivotal role in driving the industry toward lower-cost trading. To enhance accessibility, they eliminated trade commissions entirely in 2019! Moreover, their recent merger with TD Ameritrade brings together the best features and resources from both platforms.

Charles Schwab provides an extensive array of educational content through its Insights & Education section, covering investing strategies, market updates, retirement planning, and more. Schwab offers clients access to third-party research reports and tools, along with webinars, workshops, and online courses to enhance investor skills.

After the completion of the merger with TD Ameritrade, Schwab investors will gain access to courses and resources from its Education Center. Additionally, TD’s popular Thinkorswim platform, featuring paper trading and advanced technical analysis tools, will become available.

Pros:

In contrast to numerous brokers emphasizing short-term trading, Schwab promotes a long-term perspective among its clients.

Schwab introduced enhanced services and more favorable pricing for clients with higher net worth in July 2023.

Investors and traders can access a comprehensive library of research and content at Schwab.

Cons:

Cryptocurrency trading is not offered at Schwab.

The fee structure for mutual fund transactions is needlessly intricate.

6. SoFi

SoFi stands out as an excellent broker for beginners, offering an outstanding user experience and combining investing, banking, and budgeting into one comprehensive platform. Unique features include fractional share investing and access to IPO investing for smaller investors.

SoFi distinguishes itself by providing commission-free options trading, emphasizing long-term responsible investing, and offering a variety of educational tools. These features make SoFi an ideal choice for both beginners and seasoned investors. Fractional shares enable investors to enter the stock market with just a few dollars.

SoFi’s user-friendly platform is particularly well-suited for those who find the stock market intimidating. SoFi also caters to retirement savers by offering IRAs, a feature not found in some other beginner-friendly brokerages. If you’re seeking an excellent online trading platform for beginners, SoFi is one of our top recommendations.

Pros:

SoFi simplifies the process of saving, investing, borrowing, and insuring, providing a one-stop solution.

SoFi clients enjoy a range of popular options for investments like ETFs, stocks, IPOs, crypto, automated investing, and stock options.

SoFi stands out by offering 22 cryptocurrencies, surpassing numerous other brokers in the current market.

Cons:

The platform does not provide open-ended individual bonds or funds.

The asset charts are very basic, lack advanced features.

7. Ally Invest

A relatively recent player in the brokerage scene, Ally Invest proves to be a solid choice for individuals already engaged with Ally Bank seeking an uncomplicated way to extend their financial endeavors into the realm of investing.

The convenience extends to Ally’s mobile app, allowing users to access their accounts, receive quotes, and execute trades. Recognized for outstanding customer service and progressive digital banking features, Ally ensures a seamless transfer of funds between your bank and investment accounts.

Pros:

When it comes to the integration of brokerage and banking combinations, Ally stands out by providing universal account access and facilitating instant money transfers between accounts.

It is recognized as one of the best for banking services in 2023.

Ally further impresses with a no-load $0 mutual fund trade. Particularly noteworthy for beginners, Ally’s trading ticket and options matrix offer enhanced usability.

Cons:

While Ally Invest excels in certain aspects, its trading tools lag behind those of industry leaders such as Fidelity and Charles Schwab, albeit at a significant distance.

Additionally, although Ally’s educational content is robust, it is somewhat concealed – not available in the app and challenging to locate on the website.

8. Vanguard

For those seeking the most cost-effective investment option, Vanguard emerges as a top contender. This prominent American fund management group has established itself as a discount online brokerage, offering unparalleled value on both sides of the Atlantic, whether you’re investing in a stocks and shares ISA or a brokerage account.

Investing in Vanguard’s LifeStrategy portfolios can cost as little as 0.22% annually, with a platform fee of 0.15%. While Vanguard may not provide extensive educational resources on its site, it shines for individuals with some existing knowledge. The LifeStrategy portfolios cater to various risk preferences, ranging from cautious to aggressive.

Pros:

Extensive variety of mutual funds available.

Commission-free trades for stocks, options, and ETFs.

A recognized leader in offering low-cost funds.

Competitive interest rate on uninvested cash.Maintains high-order execution quality.

Cons:

Utilizes a basic trading platform.Provides limited research and data.

Conclusion

Selecting the best investment website for beginners requires careful consideration of factors like cost structure, account minimums, diversification of funds, and available account options. Fidelity impresses with its educational platform and comprehensive services. E*Trade stands out for its diverse investment options and user-friendly tools. JPMorgan’s platform is designed for user-friendliness, especially for existing Chase customers.

Merrill Edge, associated with BOA, offers seamless integration and a variety of educational resources. Charles Schwab provides extensive educational content, and SoFi stands out with its comprehensive platform. Ally Invest is a solid choice for Ally Bank customers, and Vanguard offers cost-effective investment options with a variety of mutual funds. Each platform has its strengths and considerations, catering to different preferences and needs in the dynamic landscape of online investing. If you want to be financially responsible and increase your earnings then start investing with these best investment websites.

The term “Financial responsibility” might sound heavy, perhaps mimicking your dad’s or mom’s voice in your head. However, being financially responsible is simply about maintaining control over your money instead of letting it control you. It’s a crucial aspect of shaping your path to adulthood.

When you exhibit financial responsibility, you cultivate healthy spending habits that prevent you from overspending. This approach allows you to enjoy your money and the sense of security it provides, eliminating the monthly worry of struggling to pay your bills.

Integrating financial management into your life’s essential processes and incorporating it into your ongoing plans or aspirations is crucial. Even if your finances seem intricate and perplexing, the ten valuable tips in this article should assist you in taking command and gaining control over them.

What Exactly Is Being Financially Responsible?

Practicing financial responsibility entails managing your money wisely and making informed decisions. It involves the skillful handling of saving, budgeting, and investing. Additionally, it means being mindful of spending habits and preventing the escalation of debt.

Financial responsibility is significant as it empowers you to steer your finances effectively and make choices aligned with your best interests. When you exhibit financial responsibility, the likelihood of falling into debt or bad financial choices is on the list. It serves as a cornerstone for realizing long-term financial objectives and establishing a robust foundation for your future.

Top 10 Tips For A Financially Responsible Future

1. Pay Yourself What You Are Worth and Cut Your Expenses

The first step is to ensure you’re compensated fairly by understanding your job’s market value. Evaluate your productivity, contributions, and skills to determine your worth. Research both external and internal salary rates for your role. Advocating for your deserved salary showcases market awareness.

List your degrees, qualifications & skills, certifications, and achievements when negotiating pay. This demonstrates your alignment with job requirements and helps in salary research.

However, financial stability requires spending less than you earn regardless of income. Cost-cutting efforts in various areas can lead to significant savings. Small adjustments can make a difference without major sacrifices.

2. Controlling Credit Card Debt

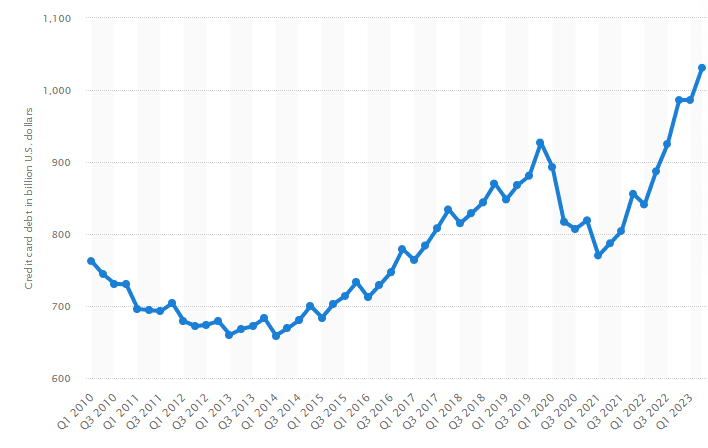

Credit cards serve as a valuable tool for significant purchases and establishing a positive credit history. Many credit cards offer enticing rewards like cash back or airline miles, enhancing their appeal. However, the convenience of credit cards may lead to the swift accumulation of debt. This holds as an American’s average credit card debt is $6,365. Fortunately, there are practical steps to prevent the accrual of substantial debt.

Source: Statista – Credit card debt in the United States from 2nd quarter 2010 to 2nd quarter 2023

To maintain a healthy credit profile, consider the following tips:

Ensure to settle your balance entirely every month.

Make on-time payments consistently.

Aim for a low utilization ratio, ideally below 30%.

Familiarize yourself with the details of your credit card agreement.

Avoid opening too many accounts in a short timeframe.

Using credit cards wisely contributes to improved financial well-being. Monitoring your credit score is equally crucial. Experian and many other online services offer free credit monitoring services, which provide access to your credit report and FICO Score, along with real-time alerts about changes in your credit report, allowing you to address potential issues promptly.

If your credit score falls below your desired level, bringing overdue accounts up to date and consistently paying bills on time can be instrumental in enhancing it.

3. Tackle Your Debt

Just as we discussed earlier in relation to credit cards, carrying debt can pose challenges in managing your monthly expenses. Additionally, it can elevate your debt-to-income ratio, potentially hindering progress toward your financial objectives. If you’re grappling with high-interest debt, incorporating debt repayment into your financial routine can be a smart move.

Consider setting “debt payoff” as one of your financial goals and review your budget to determine the amount you can allocate each month to reduce your debt. Explore various debt payoff strategies, such as the debt avalanche method or the debt snowball method, to find an approach that aligns with your financial circumstances and objectives.

4. Budgeting for Responsible Financial Well-Being

Establishing a budget isn’t exclusive to business owners or finance experts; it’s a crucial practice for everyone. It serves as a foundational financial habit that complements other financial planning strategies, applicable regardless of your financial situation.

Once you’ve crafted a budget, you gain clarity on your investment capacity, determine reasonable contributions to your emergency fund, and identify the amount available for monthly debt repayment. Here are some tips to start by:

Determine your net income: Your gross income, or take-home pay, is the foundation of a successful budget. It is all of your earnings less the costs of taxes and employer-sponsored benefits like medical coverage and plans for retirement.

Monitor your spending: List your fixed expenses to start the budgeting process. These are regular monthly expenses like utilities, lease or mortgage, and auto payments. Next, list your variable expenses, which include things like gas, groceries, and pleasure that could change on a monthly basis. There are chances for possible savings in this area.

Establish achievable goals: Prior to scathing into the details you’ve tracked, outline a list of your short-term and long-term financial goals. Possibly in a year or three, short-term objectives could include things like setting up an emergency fund or paying off credit card debt. Conversely, long-term objectives, like funding your child’s education or retirement, might take longer than five years to complete.

Create a strategy: This is the phase where all the elements converge: your actual spending versus your intended expenditure. Utilize the compiled list of fixed and variable expenses to project your upcoming monthly outlays. Then, align this with your priorities and net income. Contemplate establishing precise—and achievable—spending limitations for each expense category. You may opt to categorize your expenses further, distinguishing between necessities and luxuries. Consider adopting the 50-30-20 plan—allocating 50% to needs, 30% to wants, and 20% to savings.

Modify your spending to adhere to the budget: Having established your expenses and income, you can now make any required adjustments to prevent overspending and allocate funds toward your objectives. Prioritize trimming your discretionary “desires” as the initial area for potential reductions.

5. Prioritize Your Financial Well-being

Taking control of your interest and borrowing expenses may seem challenging, but in reality, it boils down to discerning between necessities and luxuries. For instance, while having a car may be a necessity, owning a high-end model is a luxury. If you can’t afford to pay for it outright, it’s advisable to opt for a more budget-friendly option.

Similarly, having a place to live is a necessity, but residing in a mansion is a luxury. For most individuals, a mortgage is a necessary step to own a home, but it’s crucial to do so in a financially responsible manner. A general guideline is that the cost of your home shouldn’t exceed two to 2.5 times your annual income. Additionally, a healthy measure is ensuring that your monthly mortgage payment doesn’t surpass 30% of your monthly take-home pay.

Beyond steering clear of excessive spending on your home, it’s advisable to make a substantial down payment that eliminates the need for private mortgage insurance (PMI). If meeting these purchasing criteria proves challenging, consider renting until you’re financially ready to make a home purchase.

6. Build Your Emergency Fund

Regardless of your income or expenses, having an emergency fund is crucial for financial stability. The size of this fund should align with your lifestyle, with a common recommendation being enough to cover three to six months of expenses.

To ease into the habit of saving, start with a modest initial contribution. This ensures your cash flow isn’t strained, reducing the likelihood of abandoning your savings routine.

Opt for direct deposit to keep your savings out of sight and out of mind. Many employers offer this option, allowing you to allocate funds to multiple accounts.

While an emergency fund is essential, avoid allocating an excessive portion of your savings to it. Since it’s meant for quick access, it’s often stored in low-yield options like a savings account with minimal interest.

Once you reach your target for the emergency fund, redirect your contributions to an account that can generate returns, such as your retirement account. This strategic move allows your money to grow over time, maximizing its potential.

7. Buckling Up Your Investments

Starting your investment journey may feel overwhelming as a newcomer, but it can be easy with little knowledge. Questions about the required amount, how to initiate the process, and the best strategies for beginners can be daunting. However, investing early in your life can yield substantial returns, thanks to the power of compound earnings. This phenomenon allows your investment returns to generate their own returns, leading to significant growth over time.

Whether you’re committing $1,000 monthly or a more modest $50, establishing a regular contribution to your investments is key. This consistency ensures a steady influx of funds into your investment portfolio. To set you on the right path, here are some fundamental insights to consider before diving into the world of investing:

Determining the right amount:

It is a crucial decision, influenced by your financial situation, investment goals, and the timeline for achieving them.

For retirement, a common investment objective, consider allocating 10% to 15% of your annual income. If you have a workplace retirement account, like a 401(k), that offers employer matching, prioritize contributing enough to receive the full match. This matching contribution is essentially free money, a valuable boost towards your retirement goals.

For other aspirations such as homeownership, travel, or education, evaluate your time horizon and financial needs. Break down the required amount into manageable monthly or weekly investments to stay on track.

Opening an investment account:

If you lack access to an employer-sponsored retirement plan, an individual retirement account (IRA) is a viable option, offering both traditional and Roth IRAs. However, if your investment goals extend beyond retirement, explore taxable brokerage accounts. These accounts provide flexibility, allowing withdrawals without additional taxes or penalties, making them suitable for various financial objectives.

Create an Investment Approach

Selecting the right investment strategy hinges on your specific saving objectives, the financial milestones you aim to achieve, and the time frame for reaching them.

For long-term goals extending beyond 20 years, such as retirement, a significant portion of your funds can be allocated to stocks. However, delving into individual stock selection can be intricate and time-intensive. For most individuals, a prudent approach is to invest in low-cost stock mutual funds, index funds, or ETFs, providing diversified exposure to the stock market.

Conversely, if you are saving for a short-term goal with a horizon of less than five years, the inherent risk associated with stocks suggests a more conservative approach. Safeguard your funds in secure avenues such as online savings accounts, cash management accounts, or low-risk investment portfolios to preserve capital and liquidity.

A Primer on Investment Choices

Upon determining your preferred investment strategy, the next step involves selecting specific assets for your portfolio. Every investment comes with its own set of risks, and comprehending the characteristics of each instrument, evaluating its risk profile, and ensuring alignment with your financial objectives is crucial. Here are some popular investment options, particularly suitable for beginners:

Stocks

Bonds

Mutual Funds

Exchange-traded funds (ETFs)

Understanding the nature of these investments will empower you to make informed decisions that align with your financial goals and risk tolerance.

8. Prepare for the Unforeseen

Contemplating mortality may not be pleasant, but ensuring the well-being of your loved ones in the event of your demise is a responsible step. Even if you’re presently unattached with no dependents, securing an affordable life insurance policy while you’re younger is a prudent financial move.

The process of obtaining life insurance is straightforward, and it doesn’t have to strain your monthly budget. Although there is a multitude of life insurance products available, opting for a term insurance policy is often considered a clear-cut choice for many individuals seeking the coverage they require.

As you navigate significant milestones like marriage, homeownership, or parenthood, a term insurance policy becomes a valuable asset, offering financial protection in the event of your absence.

9. Update Your Will

You might be wondering about the relevance of a will in the realm of financial responsibility. A will, formally known as a last will and testament, is a legal document that outlines your preferences concerning the distribution of your assets and finances after your passing. It stands as a crucial element of financial responsibility, ensuring that your wishes are upheld. Without a will, the execution of these wishes may be uncertain, leading to additional time, costs, and emotional strain for your heirs.

While no single document can anticipate every posthumous issue, a well-crafted will can address a significant portion of them. Surprisingly, only 33% of Americans had a will in 2021. Whether you have dependents or varying degrees of assets, having a will is essential. While you can create a basic will on your own, seeking guidance from a legal professional is advisable for added assurance. To enhance the protection of your loved ones and streamline the posthumous process, it’s wise to consider updating your will.

10. Maintain Accurate Tax Records

Last but not least, neglecting to keep meticulous records may result in missing out on potential income tax deductions and credits.

Establish a systematic approach and maintain it throughout the year. This proactive strategy is far more efficient than the last-minute scramble during tax season, preventing oversights that could have otherwise contributed to savings.

Conclusion

Embracing financial responsibility is not just a distant goal but a practical and achievable path to securing your financial well-being. By incorporating the ten essential tips provided, you can navigate the realm of personal finance with confidence and control.

Understanding the fundamentals of financial responsibility involves more than just budgeting; it requires a holistic approach to managing your money wisely. From addressing credit card debt to strategically investing for the future, each tip contributes to a comprehensive strategy for long-term financial success.

Take the time to pay yourself what you’re worth, control credit card debt, tackle existing debts, and establish a realistic budget. Prioritize your financial well-being by distinguishing between necessities and luxuries, building an emergency fund, and initiating a well-thought-out investment journey.

Remember, your financial journey is not complete without preparing for the unforeseen. Securing life insurance, updating your will, and maintaining accurate tax records are integral components of a responsible financial plan.

In essence, being financially responsible is about taking charge of your financial destiny, making informed decisions, and cultivating habits that lead to a secure and prosperous future. As you embark on this journey, keep in mind that financial responsibility is not a destination but a continuous process of learning, adapting, and thriving in the ever-changing landscape of personal finance.

Running an online business requires an effective method for receiving payments, and payment gateways serve as financial tools that facilitate the collection of payments through credit or debit cards. Nowadays, where online shopping is prevalent, and physical cash is less common, having an accessible and user-friendly payment gateway is essential for engaging both consumer and business clientele.

To make an informed choice for your business, it’s crucial to evaluate factors such as cost, features, and supported payment methods. Read on to discover the best payment gateways in 2024 suitable for businesses that rely on card-based transactions.

A payment gateway is a software application utilized by merchants to facilitate the acceptance of various electronic payments, including credit cards. Functioning as encryption systems, these gateways play a crucial role in safeguarding sensitive information like credit card numbers during the transfer from customers to merchants. Following this secure exchange, the gateways transmit transaction details to both the customer’s bank and the merchant’s acquiring bank, responsible for credit card processing services.

The payment gateway assumes the responsibility of authorizing credit card transactions and ensuring the seamless transfer of funds from the customer’s account to the merchant’s account. It’s common for payment gateways to impose a monthly fee along with a per-transaction fee for their services.

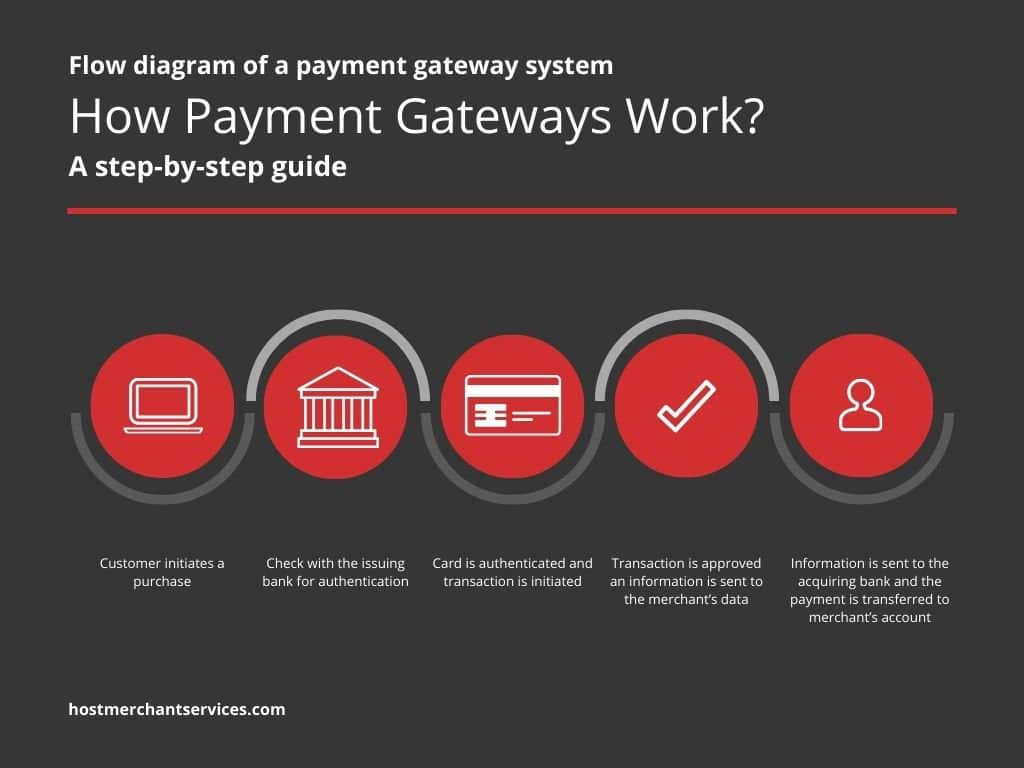

How Payment Gateway Works?

The structure of a payment gateway can be divided based on its use in either an online payment portal or an in-store setting. For online payments, the gateway must be hosted on the website. This can be done through a third-party service provider or directly by the merchant using an API. This integration enables the website to interact with the payment processing network and receive a response from the issuing bank.

In an in-store setting, a payment gateway is utilized through a physical card reading device or a POS terminal. These devices connect to the processing network via a secure internet connection, ensuring a seamless transaction process.

Key Players In The Payment Gateway Ecosystem

Merchant:

The merchant is the individual or business conducting online sales of goods or services. To enable online transactions, a merchant requires a merchant account, essentially a bank account tailored for online transactions. Integrated with the payment gateway, this account ensures secure transaction processing, serving as the destination for incoming funds after settlement.

To open a merchant account, thorough research is necessary to select a provider that aligns with specific business requirements.

Customer:

Customers constitute the primary participants in the payment gateway ecosystem. They utilize various online payment methods, including debit or credit cards, net banking, UPI, or online wallets, to make purchases online.

Acquirer and Issuer Bank:

Two distinct types of banks operate within the payment gateway ecosystem. The acquirer bank manages payments on behalf of the merchant, housing the merchant account. This bank serves as the endpoint for financial transactions routed through the payment gateway, ultimately receiving the funds.

Conversely, the issuer bank is where the transaction originates. This account belongs to the customer initiating the payment for a product. The issuer bank represents the customer and supports diverse payment methods like credit cards, debit cards, or net banking.

Payment Gateway:

Serving as the intermediary between the merchant’s website or app and the acquirer and issuer banks, the payment gateway plays a crucial role.

When a customer makes a purchase on the merchant’s platform, the payment gateway facilitates the smooth progression of the payment. It ensures the secure transfer of payment information and manages the authorization and settlement of transactions.

Payment Processor:

The payment processor is responsible for overseeing the technical connections between the payment gateway, the acquiring bank, and the issuer bank. It validates and securely routes payment transactions. Both the payment gateway and the payment processor are essential components in effectively managing online payment transactions.

How To Select The Best Payment Gateway?

Selecting the appropriate payment gateway for your business is a crucial decision. Opting for a gateway that doesn’t align with your business model can potentially lead to significant financial losses and a decline in customer satisfaction.

Consider the following key factors:

Cost:

The foremost consideration when choosing a payment gateway is the overall cost it incurs. The costs associated with payment gateways typically involve a set-up fee, a monthly fee, and a transaction fee.

To determine the most cost-effective option for your business, it’s essential to evaluate both the volume and value of your transactions. Many payment gateways offer competitive transaction fees, often around 2.9% + 30¢. Carefully assessing these costs ensures a financially prudent choice for your business.

Accepted Card Types:

The widely utilized credit cards—Visa, MasterCard, and Amex—are typically supported by most payment gateways. However, if your customers commonly use alternative card types like debit cards or Diners Club cards, it’s crucial to ensure that your chosen payment gateway accommodates these variations.

Holding Period:

While payments are generally swiftly approved, there is a brief holding period before the funds are settled into your account. This delay allows for the processing of refunds and handling chargebacks. Holding periods can range from 1-7 days, varying among payment service providers. Depending on your cash flow needs, you can opt to receive immediate payment or wait for the designated settlement period.

Multiple Currency Support:

For businesses engaged in international transactions, verifying that your selected payment gateway can process payments in various currencies and from different countries is essential. Enabling customers to pay in their preferred currency is paramount. Additionally, it’s advisable to check for any associated fees related to foreign currency transactions.

Seamless Integrations:

Ensure that your chosen payment gateway seamlessly integrates with your shopping cart, accounting software, and any other tools essential for your business operations. This integration capability enables automation in your accounting processes, ultimately saving valuable time.

Customization Options:

Consider whether the payment gateway provides customization features. For instance, having the ability to incorporate your logo or modify the payment page’s color scheme can enhance your brand representation. Many gateways offer this through an API, though it’s worth noting that not all gateways provide such customization options.

Emphasis on Security:

Prioritize security when making your payment gateway selection. It’s crucial to confirm that the gateway employs state-of-the-art encryption technology to safeguard your customers’ credit card details from potential theft.

PCI Compliance:

Verify that the chosen payment gateway adheres to PCI compliance standards. This compliance involves following the PCI DSS standard, a set of security regulations mandatory for all businesses engaged in credit card payment processing. Choosing a PCI-compliant gateway ensures that your business meets the required security standards.

Top 10 Payment Gateways In 2024

There are many payment gateway options now with the rise of e-commerce and online payments, here is our best pick for the reliable payment gateway solution for 2024:

1. Authorize.Net

Pricing: $25 monthly

Processing Charges: 2.9% + an additional $0.30 for every transaction

Authorize.Net, affiliated with Visa, accommodates major credit cards like Mastercard, Visa, Discover, American Express, JCB, and Diner’s Club. It also supports digital payment services such as PayPal, Visa Checkout, and Apple Pay. While it caters to global transactions, your business must be registered in the US, Canada, UK, Australia, or Europe.

Starting with the gateway-only plan, which incurs no setup fee, it involves a monthly gateway fee, a per-transaction charge, and a daily batch fee. For larger business needs, enterprise solutions provide customized pricing.

Pros: Tailored fraud prevention with AFDS Offers both payment gateway and one-stop solution for flexibility No setup charges, minimizing the initial costs

Cons: Additional charges for specific features like e-check and Account Updater Merchant account approval may take up to 5 business days, potentially delaying the setup.

2. PayPal

Pricing: Free

Processing Charges: 2 to 4% + an additional $0.49 for every transaction

A stalwart in online payments, PayPal facilitates quick registration and online payment acceptance. It extends its services to mobile and in-person transactions, among other financial solutions.

Online card payments typically incur a $0.49 fee plus an additional 3.49%. QR code payments reduce costs to 1.90% for transactions above $10 or 2.40% for transactions of $10 or less, plus the $0.49 fee. Businesses usually face no monthly recurring fees. In-person payments cost 2.70% for card-present transactions or 3.50% plus $0.15 for keyed transactions.

Pros: Versatile payment solutions for diverse business needs Strong global recognition instills customer trust Efficient customer support post-sale Transparent pricing with no monthly fee

Cons: May not be cost-effective for high-volume sellers Known for holding funds from sellers and occasional account closures with limited recourse.

3. Stripe

Pricing: Free

Processing Charges: 2.9% + an additional $0.30 for every transaction

For companies of any kind, Stripe offers outstanding adaptability with over 660 integrations. Because of its highly configurable nature and application programming interfaces, it can be easily integrated into applications for smartphones and other software, catering to both startups as well as big corporations. Robust identification of fraud and tools for risk management, a flexible checkout procedure, the capacity to process payments via the Internet in over 135 currencies, and low-cost, programmed clearinghouse processing are some of the key features. Stripe offers flexible monthly agreements and reasonable fees when compared to different payment gateway service providers.

Pros: Zero monthly charges Zero setup charges Developer-friendly Highly versatile with many integrations and customizations

Cons: Instant deposits cost 1% of the transaction No native inventory management

4. Square:

Pricing: Free

Processing Charges: 2.6% + an additional $0.10 for every transaction

Founded in 2009, Square has become a prominent financial services and mobile payment provider, generating over $3 billion annually. Offering an intuitive and user-friendly experience, Square gained popularity in online payment gateways. Without needing to know programming or other specialized technical abilities, consumers can create an effective online presence with its tools.

Square offers several more sophisticated plans with recurring costs in addition to a starter package at no cost. Dispute resolution and live mobile assistance are included with all plans. On a device you own, Square’s standard POS is free to use through a mobile app. Advanced attributes, such as shortage in inventory alerts, are only available with a monthly POS plan.

Pros: Zero monthly charges Clear pricing on a per-transaction basis Cheap and best hardware BNPL options for online and in-person transactions Numerous add-ons and integrations are available

Cons: Loyalty programs for customers cost extra No additional phone supportInflexible support hours for customers

5. Braintree:

Pricing: Free

Processing Charges: 2.59% + an additional $0.49 for every transaction

Since its acquisition by PayPal in 2013, Braintree has become closely associated with the renowned payment service provider. What sets Braintree apart is its provision of dedicated merchant accounts, a rarity among payment service providers. Some notable users of Braintree’s payment solutions include Uber, Airbnb, and GitHub.

Pros: Drop-in payment widget with a best-in-class UI Accept multiple payment methods with a single implementation Single dashboard to manage all user subscriptions

Cons: Coupon management is not very robust Setup is challenging, lacking seamless migration from existing payment systems Slow response from customer support

6. Stax:

Pricing: $99 per month (no transaction fees)

Stax distinguishes itself with comprehensive customization tools that make branding tailored to your business easier than with other payment gateways. Its custom branding options allow you to tailor invoices, receipts, and website payments to align with your brand. Stax integrates seamlessly with popular business software programs like Xero, QuickBooks, MS Teams, Hubspot, Slack, Zoho, Google Docs, and Calendly.

Unlike most payment gateways, Stax adopts a flat monthly fee model instead of charging a percentage of each transaction, though there are still flat per-transaction fees.

Pros: No charges for transactions; pay one flat-rate monthly subscription fee. Free mobile or terminal reader Scheduled payments and Recurring invoices option Digital invoicingOption for ACH processing

Cons: Additional fees per terminal1% charge for same-day access to funds

7. Payment Depot

Pricing: $79 flat fee monthly

Processing Charges: 2% + an additional $0.10 or $0.22 for every transaction

Distinguishing itself from other payment processor companies, Payment Depot employs a subscription pricing model based on a merchant’s month-on-month transaction volume. Merchants pay a flat fee per transaction along with the interchange rate, irrespective of the transaction type.

Notably, Payment Depot doesn’t impose hidden fees or cancellations and ensures swift access to funds within 48 hours of a transaction. The company offers various card readers, terminals, and POS systems, complemented by 24/7 customer support.

Pros: Significant savings for merchants in fees Top-notch customer care and support Flexible month-to-month billing

Cons: Limited hardware options Relatively costly for businesses with lower transaction volumes

8. Clover

Pricing: $14.95 monthly

Processing Charges: 2.6% + $0.10 for every transaction

Clover stands out as one of the premier payment gateways for small, brick-and-mortar businesses due to its user-friendly interface suitable for non-technical users. Its features encompass reporting tools for aggregated sales across multiple locations, revenue tracking, end-of-the-day reports, sales tracking, and analysis of peak business hours. Clover facilitates rapid deposits, allowing access to sales transaction funds within minutes (with a 1% fee).

Additionally, it supports the creation of digital and physical gift cards and accepts payments via Google Pay, Apple Pay, PayPal, and Venmo.

Pros: Well-structured and transparent pricing plans Comprehensive feature set, including tracking, loyalty programs, and order management. Acceptance of a wide variety of payment methods

Cons: Longer learning curve for users with limited technical expertise

9. Adyen

Pricing: Free

Processing Charges: $0.13 plus different interchange

Adyen stands as an international payment processor facilitating transactions across diverse payment channels, such as in-app orders with in-person pickup, self-scan and pay, in-store purchases, home shipping, QR code payments, and self-service kiosks.

For businesses in the US, Adyen imposes a $0.13 processing fee along with a variable interchange fee determined by the customer’s payment method. Interchange typically ranges between 2% to 4%, varying based on the chosen payment method. As a global processor, Adyen supports nearly every card or payment platform, including Alipay, Affirm, Apple Pay, Amazon Pay, Diners Club, and Cash App Pay.

Pros: Zero setup or monthly charges Round-the-clock mobile support A comprehensive knowledge base available on its site

Cons: Requires two months’ written notice for contract termination Minimum sales volume requirement of $120 Not as user-friendly for individuals without a technical background

10. Helcim:

Pricing: Free

Processing Charges: 1.92% + an additional $0.8 for every transaction

Helcim is renowned for its cost-effective payment gateway, offering an array of features, including invoice creation, subscription setup, and international payment processing. The platform provides numerous APIs, enabling customization of the payment gateway to align with specific business needs.

For businesses with high transaction volumes, Helcim offers automatic volume discounts, eliminating the need to contact their sales team for negotiation.

Pros: Zero monthly charges—transaction fees only Below the average rates for processing payments No need of long contracts, you can pay as you go API allows for extensive customization

Cons: Flat charges of $10 monthly for instant deposits Additional cost associated for hardware

Conclusion

Selecting the right payment gateway is a pivotal decision for any online business, influencing both customer satisfaction and financial outcomes. Evaluating factors such as cost, features, and supported payment methods is crucial. Among the top 10 payment gateways in 2024, each option offers unique advantages and considerations.

Whether it’s the cost-effective model of Helcim, the user-friendly interface of Clover, or the international capabilities of Adyen, understanding your business needs is key. Ultimately, a well-informed choice ensures not only smooth transactions but also sets the foundation for sustained growth and success in the competitive online marketplace.

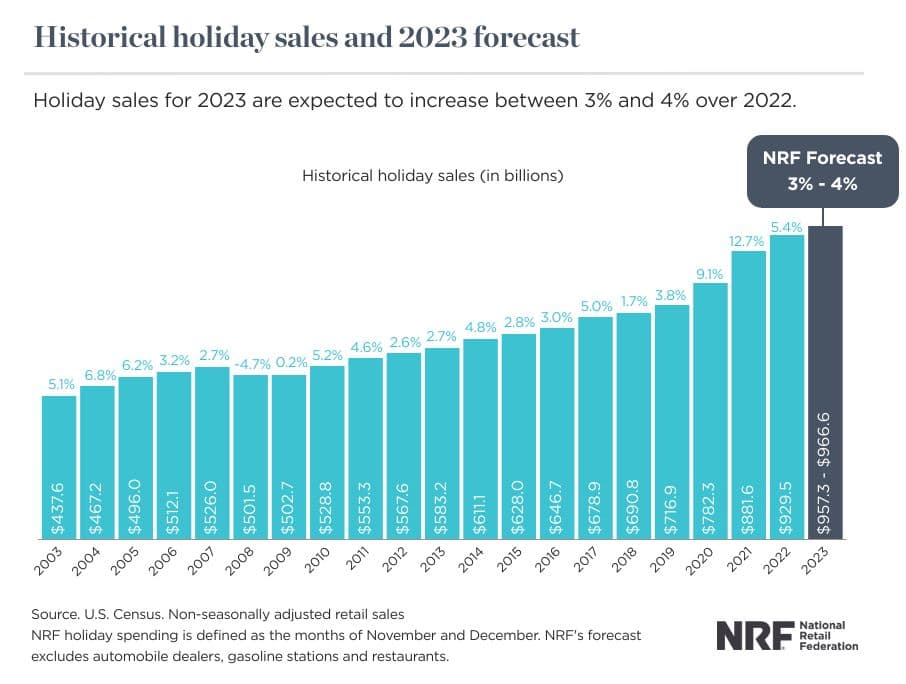

The holiday shopping season for 2023 has officially arrived. Brands and retailers are busy and actively involved in their marketing strategies. They are making sure to have inventory and aligning their resources for a great quarter ahead and a joyous holiday season. Plans are in place for wholesale, dropship, marketplaces, and social initiatives, creating a great atmosphere for the festivities.

Taking insights from the figures for 2022, retailers and brands have plenty of reasons to feel positive about the approaching holiday season. Projections indicate that retail sales will surpass $1.6 trillion by 2027, which is more than phenomenal.

However, the current economic landscape brings some uncertainty to this year’s quarter due to factors like macroeconomics, inflation rates, job market conditions and high-interest rates. There is anticipation among industry observers as they await to see how consumers will navigate these challenges while approaching their holiday shopping. Let us understand the holiday shopping trends in 2023 and how inflation and supply chain problems will impact these 2023 holiday shopping trends.

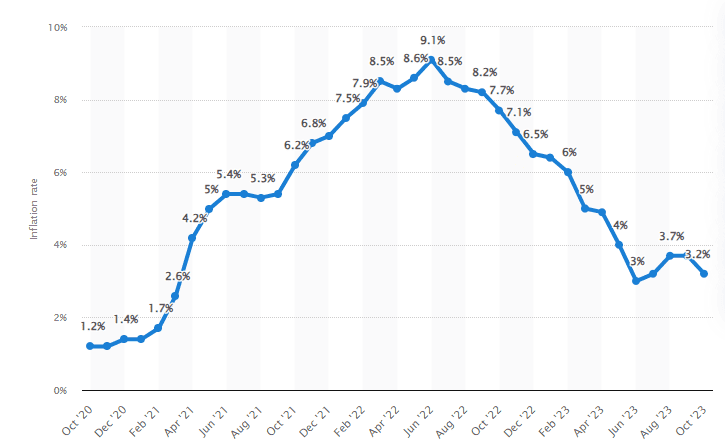

Source: Statista – Monthly inflation rate in the US

The Impact Of Inflation On Item Prices This Year