Point of Sale Market Share 2024

Posted: November 14, 2024 | Updated:

The Point of Sale market share has experienced significant growth and transformation in recent years, driven by technological advancements, evolving consumer behaviors, and the increasing adoption of digital payment solutions.

The global POS market continues to expand as of 2024, with various segments and regions contributing to its development. This article comprehensively analyzes the POS market share in 2024, focusing on key components, deployment models, end-user industries, regional insights, and future trends.

Point of Sale Market Share: An Overview

The POS system is a critical component in retail and service industries, facilitating transactions between businesses and customers. It encompasses hardware and software solutions designed to process sales, manage inventory, and handle customer data. The market’s growth is propelled by the increasing demand for efficient transaction processing, enhanced customer experience, and the integration of advanced technologies such as cloud computing and mobile solutions.

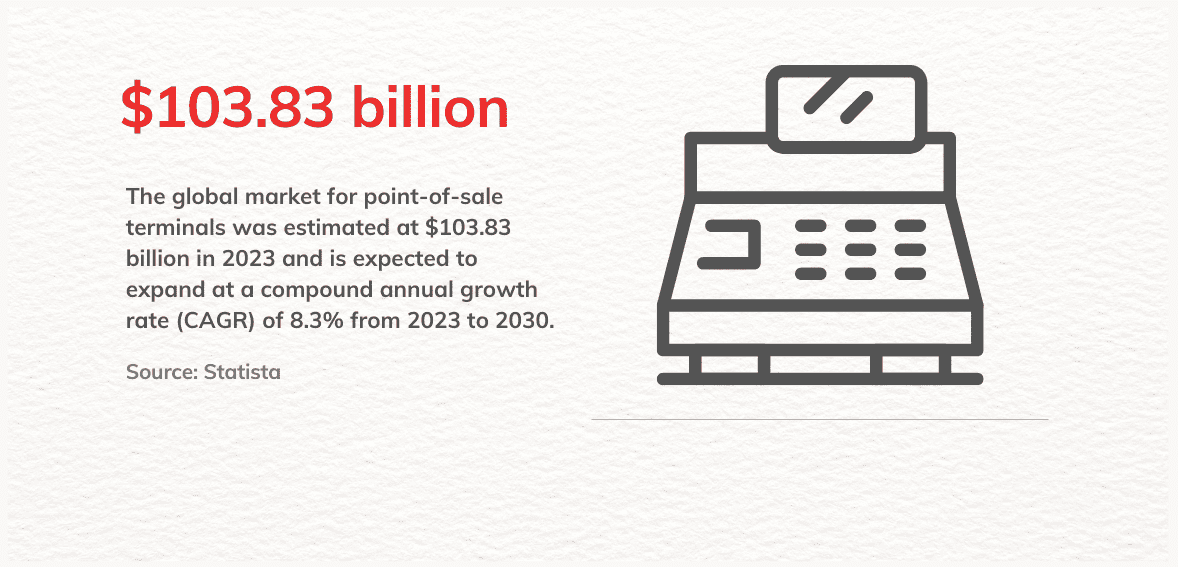

The global market for point-of-sale terminals was estimated at $103.83 billion in 2023 and is expected to expand at a compound annual growth rate (CAGR) of 8.3% from 2023 to 2030. This growth is attributed to the rising adoption of digital payment methods, the proliferation of e-commerce, and the need for streamlined business operations.

Market Segmentation of POS Systems: Overview and Trends

The POS market is divided into various segments: product types, components, deployment models, end-user industries, and geographical regions.

1. Product Segmentation

Regarding product segmentation, the POS terminal market is classified into fixed and mobile terminals. The fixed POS terminals held a significant share, over 60%, of global revenue in 2022. Large retailers and other major vendors favor fixed POS systems for their comprehensive functionalities, which support numerous operations such as bill printing, customer relationship management (CRM), inventory tracking, and accommodating multiple payment methods.

On the other hand, mobile POS (mPOS) terminals are anticipated to grow fastest from 2023 to 2030. The growth is primarily driven by the increasing preference for mobile payment solutions within stores, which offer flexibility to process transactions anywhere in the store. This capability significantly enhances customer satisfaction by minimizing wait times and streamlining service.

2. By Component

Discussing the components, the hardware segment dominated the global market in 2022, representing over 63% of total revenue. This segment includes devices essential for POS functions, such as EFT-POS machines, cash drawers, barcode scanners, tablets, receipt printers, and monitors. These components are integral to fixed POS terminals, supporting daily operations and management tasks.

Conversely, the software component of POS systems is predicted to experience the highest growth rate from 2023 to 2030. This rise is linked to the increasing demand for software solutions that offer data support, multifunctional capabilities, and sales analysis tools. Different industries require specialized software solutions; for instance, retail POS software typically includes features for accounting, transaction notifications, and inventory control. The services component encompasses installation, maintenance, and support, which are crucial for the efficient operation of POS systems.

3. By Deployment Model

Regarding deployment models, there are two options:

- On-Premise: Traditional POS systems installed locally on a company’s hardware and servers. While offering control and customization, they require significant upfront investment and maintenance.

- Cloud-Based: These systems operate over the Internet, offering scalability, remote access, and lower initial costs. The cloud segment is projected to experience a significant growth rate of 10.9% from 2023 to 2030. The shift towards cloud-based POS systems is gaining momentum among businesses, driven by their numerous advantages compared to traditional on-premises setups.

Additionally, in January 2022, Xenial, Inc. introduced an update to its cloud-based POS system, the 3.6 Xenial Ordering. This version includes enhancements to the overall workflow, user interface, and underlying infrastructure, improving the system’s performance and functionality.

4. By End-User Industry

The market also varies by end-user industry.

- Retail: Accounted for over 30% of the overall revenue. Retailers integrate POS systems with inventory, merchandising, marketing, and CRM data to offer personalized and interactive customer experiences. The retail segment includes supermarkets/hypermarkets, convenience stores, grocery stores, specialty stores, and gas stations.

- Hospitality: Restaurants, hotels, and cafes use POS systems to manage orders, payments, and customer preferences. The hospitality POS terminals market is estimated to grow at a CAGR of over 10% from 2021 to 2027.

- Healthcare: Expected to exhibit a significant CAGR over the forecast period. The broad application scope includes managing patient information, facilitating quick payment processes, and tracking employee statistics. The need to organize payment processes and manage patient records, especially during events like the COVID-19 pandemic, has boosted market growth in this sector.

- Entertainment: Cinemas, amusement parks, and event venues use POS systems for ticketing and concessions.

Growth Trends in the POS Market Across North America, Asia Pacific, and Europe

Asia Pacific

They remained the largest market in 2022, accounting for over 33% of the total revenue share. Government initiatives supporting a cashless economy have increased the demand for POS terminals in the region. As a manufacturing hub for POS hardware components, China has seen a rise in digital payment technologies, presenting lucrative opportunities for mPOS systems.

United States:

In 2022, the U.S. POS market was valued at $4.97 billion and is currently considered to have over 13% of the global POS market share. This growth is largely attributed to the retail and restaurant sector’s increasing use of cloud-based PoS software. The region’s substantial presence of key industry players contributes significantly to market expansion.

Payment processors like Stripe and PayPal support emerging payment technologies, including contactless payments, mobile wallets, and cryptocurrencies. These firms also enhance their data analytics capabilities to improve customer experience and inventory management.

Europe

Europe holds a significant share due to the presence of established retail chains and the increasing adoption of digital payment solutions. It is experiencing significant growth, with a CAGR of 7.8% from 2023 to 2030.

The increasing demand for cashless and contactless transactions, coupled with regulatory actions on secure payments, has expanded the POS terminal market in the region.

Key Players in the POS Market for 2024

The POS market comprises several key players offering diverse solutions to cater to various industry needs. Notable companies include:

- NCR Corporation supplies mobile and electronic payment systems to the hospitality and retail industries, with a focus on point-of-sale (POS) software applications and inventory management solutions.

- Square, Inc.: A prominent provider of POS solutions, Square serves over 4 million merchant clients globally. In 2023, its Square segment processed payments worth USD 209.6 billion, generating USD 7.03 billion in revenue.

- Oracle Corporation: Provides point-of-sale solutions worldwide, featuring inventory management, reporting and analysis, and table reservation capabilities.

- Qu, Inc.: Delivers digital-first solutions tailored for quick-service and fast-casual restaurant chains through a unified platform that supports omnichannel ordering.

- Quail Digital produces high-quality wireless headset systems for healthcare, retail, and quick-service sectors, prioritizing technical innovation and design excellence.

- Ingenico Group: A global leader in seamless payment solutions, Ingenico offers a comprehensive range of POS terminals and services.

- VeriFone Systems, Inc.: Specializes in providing secure payment solutions and POS systems for various industries.

- PAX Technology Limited: Provides innovative POS terminals and payment solutions to merchants worldwide.

Shifting the focus to recent developments, Acumera, Inc. presented their Acumera Reliant Platform in January 2024 at the National Retail Federation’s Annual Convention and Expo. This platform ensures that retailers have continuous access to vital applications.

Recently, POSaBIT Systems Corporation announced the full launch of POSaBIT POS 2.0, a next-generation point-of-sale system specifically designed for the cannabis industry. This new version introduces various enhancements aimed at improving user experience and operational efficiency. Notable updates include a more intuitive user interface, advanced data analytics capabilities, and expanded integrations with popular e-commerce platforms.

The POSaBIT POS 2.0 system is part of POSaBIT’s ongoing efforts to innovate within the cannabis retail sector by offering robust and compliant financial services and transaction methods.

Technological Trends Shaping the POS Market

Several technological advancements are influencing the POS market, leading to enhanced functionalities and improved user experiences:

- Mobile POS (mPOS) Systems: The portability and flexibility of mPOS systems have made them particularly appealing to SMEs. These systems allow businesses to process transactions anywhere, improving customer service and operational efficiency. The transaction value is projected to increase at an annual growth rate of 22.84% between 2024 and 2029, reaching $4.42 trillion by 2029.

- Cloud-Based POS Solutions: Cloud technology enables real-time data access, scalability, and cost-effectiveness. Businesses increasingly adopt cloud-based POS systems to streamline operations and enhance decision-making processes.

- Integration with E-commerce Platforms: The convergence of online and offline sales channels has led to the development of POS systems that integrate seamlessly with e-commerce platforms such as Shopify, WooCommerce, and Magento, providing unified inventory management and customer data analytics.

- Contactless Payments and NFC Technology: The rise of contactless payments, accelerated by the COVID-19 pandemic, has prompted businesses to upgrade their POS systems to accept NFC-enabled transactions, enhancing customer convenience and safety.

How Market Share Impacts Pricing and Innovation

The market share of key players in the POS terminal market significantly impacts pricing and innovation within the industry. Firms with larger market shares often have greater resources to invest in research and development, leading to innovations that can drive the market forward. This is evident from the activities of major companies like VeriFone and Ingenico, which continue to lead with advancements in payment security and integration capabilities.

Market share also affects pricing strategies. Larger companies can leverage economies of scale to offer competitive pricing, which can pressure smaller players to either innovate or reduce their prices to maintain relevance.

Furthermore, the market share concentration among top players tends to intensify competition. As companies strive to increase their market share, they invest in new technologies and strategic partnerships to enhance their product offerings and expand their customer base. For example, partnerships that integrate advanced payment technologies and improve operational efficiencies are common among leading firms.

Conclusion

Rapid technological advancements and increasing demand for efficient, flexible payment solutions will shape the Point of Sale (POS) market in 2024. The growth is driven by integrating mobile and cloud-based systems, adopting contactless payment methods, and the need for businesses to enhance customer experiences while streamlining operations.

As key industries such as retail, hospitality, and healthcare embrace these technologies, the market’s expansion is set to continue, with key players influencing both innovation and pricing. Businesses that capitalize on mobile and cloud-based POS and e-commerce integration trends will likely maintain a competitive edge. With increasing investments in R&D, the future of the POS market promises further advancements that will enhance both functionality and user experience.