Are Credit Card Fees Tax Deductible?

Posted: May 08, 2024 | Updated:

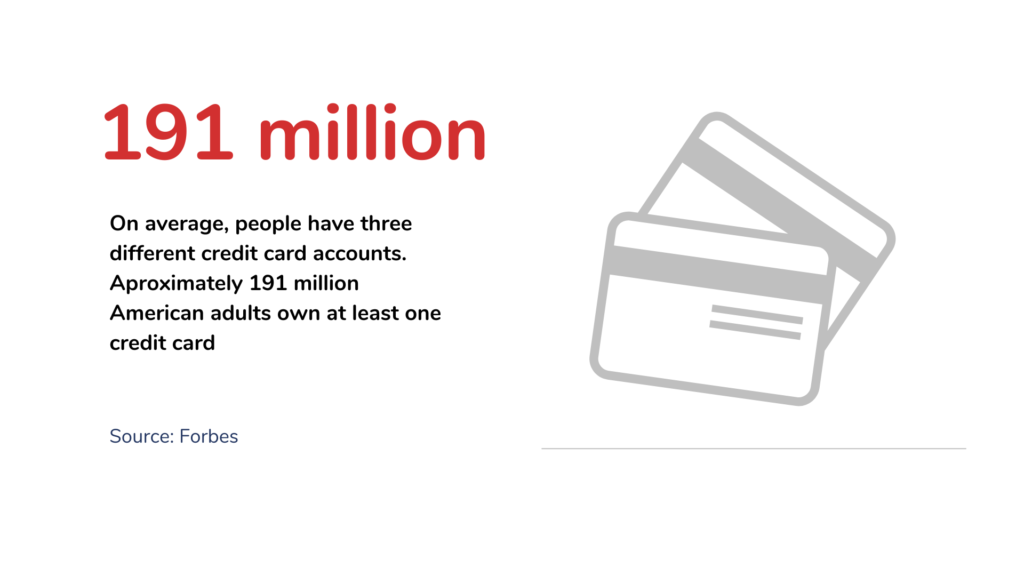

Credit card usage continues to be extremely popular, with an average of three accounts per person. Approximately 191 million American adults own at least one credit card, half of all Americans possess at least two cards, and 13% hold five or more cards. As businesses increasingly move online and process more digital payments, knowing if credit card fees are tax deductible is crucial. Understanding the related tax implications of credit card purchases is essential to maximize deductions and minimize overall tax liability.

This article will explore whether credit card payments are tax-deductible and how credit card fees affect business taxes. This knowledge will equip you to capture every tax benefit your business is eligible for. Learning the best practices for deducting these fees can enhance your business’s tax strategy and improve your financial results.

Source: Forbes

Understanding Credit Card Fees

Credit card issuers charge different rates for personal and business cards. These charges may be made yearly, for each individual transaction, or continuously. Common types of fees include late payment fees, annual fees, balance transfer fees, interest charges, and cash advance fees.

Charges, like annual fees, are incurred regularly, no matter where the card is being used. Others, such as those for cash advances, are only charged when specific transactions are made.

Credit card fees can vary greatly depending on the issuer and card type. While some cards may have no annual fee, others charge a substantial amount each year.

In addition to personal use, businesses that take credit cards as payment incur additional fees. Processing costs are applied to each transaction when debit cards, credit cards, and digital payment modes are accepted. These fees often take the form of a percentage of the transaction value plus a minor fixed amount.

Can You Deduct the Credit Card Fees

The simple answer is that it varies. It primarily hinges on whether the credit card fees were incurred for business-related activities or personal use.

Regulations from the Internal Revenue Service (IRS) suggest that people who use business credit cards for business activities, as well as entrepreneurs, can deduct “ordinary” and “necessary” expenses for their operations. In your industry, standard expenses are commonly accepted and typical. The costs that are deemed necessary for your business are known as essential expenses.

IRS Publication 535 outlines that fees associated with business credit cards—including late payments, annual fees, and balance transfer fees—often qualify under this criteria. This also extends to the potential deduction of business credit card interest and any costs incurred from accepting credit card payments.

Make sure the credit card is used just for company expenses if you intend to reduce credit card costs used for businesses from your taxes. This is so because the amount of your deductible is based on the percentage of the card that is used for business costs. For example, only 50% of the annual charge is deductible if you used the card for business purposes for 50% of your purchases.

Such complexities underscore the importance of maintaining a clear separation between your personal and business finances to avoid accounting complications.

So, What About Personal Expenses?

Interest on credit cards used for personal purchases is not tax-deductible, a rule established by the Tax Reform Act of 1986. The scope for deducting any form of personal interest on individual tax returns is minimal and generally restricted to mortgage interest, student loan interest, and interest related to investment income.

Maintaining a clear separation between personal and business expenses is essential. Whether using a small business credit card or a consumer card, it’s advisable to use a specific card only for business transactions. Mixing personal expenses with business spending on your credit card can jeopardize your ability to deduct associated fees and interest on your tax filings.

List of Credit Card Processing Fees Tax-Deductible for Merchants

Fortunately for merchants, credit card fees, payment processing fees, and merchant services fees are typically tax-deductible. This is due to the fact that they are acknowledged as inevitable and essential business expenses, but more so later.

For now, here is a list of some of the types of fees that are deductible:

- Markup fees

- Flat rate fees (also known as fixed fees)

- Batch fees

- Chargeback fees

- Non-sufficient funds fees

- POS software fees

- Per-transaction fees

- Payment gateway fees

- Payment Card Industry (PCI) compliance fees

- Authorization fees

- Statement fees

This list is not exhaustive but covers many of the standard fees that merchants can deduct.

How Can You Deduct Credit Card Charges?

Businesses of any kind can deduct credit card fees from their taxes, but the form used depends on the structure of the company. Different types of companies have different tax filing requirements. If a corporation, including LLCs that elect to be treated as C-corps, must file a tax return, it should use Form 1120. For S-corps, Form 1120-S is used for filing. Partnerships, on the other hand, use Form 1065 for their filings. If you are a sole proprietor or a single-member LLC, you can deduct these credit card charges for business expenditures using Schedule C Form 1040.

You must be able to prove beyond a reasonable doubt that the use of the credit card was exclusively for business in order to deduct business credit card fees. For instance, you are not eligible to deduct the full yearly charge of your credit card if you use it once a year to pay for gas for a business vehicle. To distinguish between personal and work expenses and keep accounting and monitoring simpler, business owners are encouraged to keep different business credit cards and personal credit card accounts.

Separate financial accounts must be kept up to date to minimize personal culpability. Combining personal and corporate funds may result in the loss of liability protections offered by LLCs and other similar entities. Courts may “pierce the corporate veil” in certain situations, making shareholders and directors personally accountable for company losses.

Things to Remember When Filing Taxes

Navigating your taxes can be challenging, and errors can cost you. To ensure accuracy and maximize deductions, follow these best practices when preparing your tax filings:

- Maintain meticulous records: Keeping organized records is crucial. Store all invoices, receipts, and relevant documents safely, as they are essential for substantiating your deductions. These documents will verify that each expense was strictly for business objectives.

- Keep personal and business expenses separate: Avoid using personal credit cards for business expenses and vice versa. This separation simplifies tax preparation and maximizes potential deductions. A POS system with integrated accounting features can also help categorize fees effortlessly.

- Consult a tax professional: Taxes, like merchant services and payment processing, are complex and often best handled by experts. Tax professionals have the specialized knowledge to navigate the nuances of tax laws and can uncover deductions you might have missed.

- Stay informed on tax policies: Keep abreast of new tax regulations in your country or jurisdiction. Being up-to-date ensures compliance with the law and helps you take full advantage of available deductions.

Common Mistakes in Deducting Credit Card Fees

It is usually simple to deduct credit card fees: those paid for business usage are deductible, but those paid for personal use are not. Yet, people often need to work on this process. One significant issue is the inability to have separate accounts for personal and business expenses.

When trying to keep credit card charges low, the following mistakes are often made:

- Mistaking credit card interest for deductible interest: Unlike mortgage interest, which is deductible on personal tax returns, credit card interest is not deductible unless explicitly tied to business expenses.

- Reducing annual fees on personal credit cards: Some individuals mistakenly deduct annual fees for personal credit cards used sporadically for business. This is problematic because it’s difficult to understand accurately which portion of these fees is business-related.

- Double-deducting processing fees: Business owners often record only the net amount received from their merchant service provider as income, which already accounts for credit card transaction fees. Therefore, these fees cannot be deducted again as they are implicitly included in the net income reported.

- Minimizing non-business-related expenses: To deduct credit card fees, taxpayers must show a clear link between them and their business operations.

Conclusion

Credit card fees are tax deductible depending on whether they were incurred for business or personal use. Understanding the IRS regulations regarding deductible expenses is crucial for maximizing tax benefits. Business owners can typically deduct fees associated with business credit cards, provided they are deemed “ordinary” and “necessary” for business operations. However, it’s essential to maintain a clear separation between personal and business finances to avoid complications during tax filing.

Deducting credit card fees requires meticulous record-keeping and adherence to best practices to ensure accuracy and compliance with tax laws. Consulting a tax professional can help navigate complexities and identify potential deductions, ultimately optimizing tax strategy and financial outcomes.

Frequently Asked Questions

Are credit card fees tax deductible for individuals?

No, per the Tax Reform Act of 1986, personal credit card fees like annual, late, and cash advance fees aren’t deductible for individuals.

Can businesses deduct credit card fees?

Yes, businesses can deduct these credit card charges tied to business expenses, including annual and transaction processing fees, as long as they meet the IRS’s “ordinary and necessary” criteria.

How are personal and business credit card fees treated differently for tax purposes

Businesses can deduct fees from business credit cards for business expenses only, while personal card fees aren’t deductible unless used for business purposes.

What types of credit card interest are deductible for businesses?

Businesses can deduct interest on purchases for business needs, such as office supplies or travel. However, interest on personal purchases, even on a business card, isn’t deductible.