How Embedded Payments Are Shaping the Future of B2B Transactions

Posted: September 30, 2024 | Updated:

Embedded payments are reshaping the B2B transaction sector, pushing the fintech industry toward a future where technology meets user convenience. These integrated solutions incorporate payment processing directly into software applications, improving efficiency and focusing on user needs. The role of embedded payments in advancing financial services is clear, offering new ways to enhance customer interactions through technologies like APIs and cloud computing.

Significant growth is expected in the area of embedded payments in 2025 and beyond. This article will explore the factors fueling this increase and what it means for traditional banking systems and fintech collaborations.

What Is Embedded Finance?

Embedded finance involves incorporating financial services and products—like payments, lending, insurance, and investment—directly into non-financial platforms and applications. This integration allows users to access financial services within the platforms they already use frequently and trust, bypassing traditional banking interfaces or separate financial apps.

Embedded finance aims to integrate financial services seamlessly into the user experience across various digital environments. This can include e-commerce sites, ride-sharing apps, travel booking portals, and social media platforms. The objective is to create a smooth, uninterrupted experience where financial transactions and services blend into the user’s regular activities on these platforms.

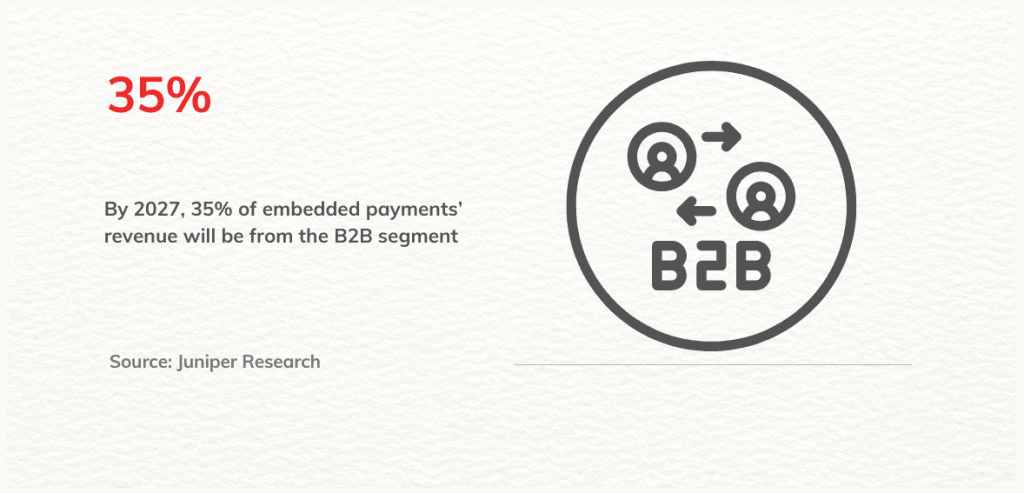

Source: Juniper Research

Open Banking vs. Embedded Finance: Key Differences

While both open banking and embedded finance modernize financial services through APIs, their scope and application differ.

Open banking focuses on allowing third-party providers to access customer banking data with consent. This is typically done under regulations like PSD2 in Europe, which mandate banks to share data via APIs. The primary goal is to foster competition and innovation in the financial sector. Open banking enables services such as personal finance management and account aggregation, giving consumers control over their financial data and allowing fintech companies to build new offerings on top of traditional banking systems.

Embedded finance, on the other hand, integrates financial services directly into non-financial platforms like e-commerce or ride-sharing apps. It goes beyond accessing data, and embedding services such as payments, lending, and insurance into everyday user experiences. Companies like Uber and Shopify can offer these services without users needing to leave their platforms or interact with a traditional bank.

In short, open banking enhances traditional financial products by improving data access, while embedded finance brings financial services directly into non-financial industries, creating new opportunities and simplifying transactions for users.

Types of Embedded Finance

Here’s a breakdown of the key types of embedded finance:

- Embedded Payments: Platforms like Uber and Amazon integrate payment options directly within their apps, streamlining the transaction process. Services like Apple Pay and Google Pay store payment information securely, enabling quick transactions, while tools like Stripe help small businesses accept payments easily, reducing operational complexity.

- Consumer Payments: Embedded finance simplifies payment acceptance across various channels—such as invoices, point-of-sale systems, and online checkouts. This feature is crucial for smaller businesses aiming to streamline their operations.

- B2B Payments: For business transactions, companies can integrate payment solutions into existing systems like supply chain or CRM platforms, improving efficiency by managing accounts payable and receivable without relying on external banking systems.

- Embedded Banking: Services such as Shopify Balance provide businesses with banking solutions, including loans and expense management, directly through their platforms. Lyft offers instant payment to drivers via branded debit cards, bypassing traditional bank accounts.

- Embedded Lending: Platforms like Afterpay and Klarna allow users to apply for loans at the point of sale, offering instant credit approval for easier financing.

- Buy Now, Pay Later (BNPL): Afterpay and Klarna enable customers to make installment-based payments directly on e-commerce platforms, spreading out payments and making large purchases easier to manage.

- Embedded Insurance: Tesla and other companies offer embedded insurance within the sales process, simplifying the purchase of coverage by removing the need for third-party providers.

- Embedded Investing: Apps like Acorns and Robinhood make investing more accessible by integrating it with other financial tools, allowing users to manage stocks and funds alongside their usual transactions.

The Transition from Traditional Payments to Embedded Finance

The shift from physical cards to digital credentials is increasingly transforming B2B payments, as embedded finance grows in importance. While embedded finance long has been a norm in consumer e-commerce, it is now gaining momentum in B2B settings. This shift is critical as businesses seek more efficient ways to handle payments and working capital management.

Digital credentials, which include the use of tokens, enable businesses to facilitate payments securely without sharing sensitive information, such as credit card numbers, with trading partners. This B2B payment innovation improves both security and efficiency in B2B transactions, especially in complex supply chains that involve multiple stakeholders. These tools can integrate with invoicing, existing procurement, and streamlining processes, supplier management systems.

This shift to digital payments also changes how businesses view payments, no longer seeing them as just transactions but as integrated parts of broader business operations, improving decision-making and offering better relationships with suppliers. As the adoption of embedded payments continues to rise, businesses are better positioned to navigate the increasing complexity of global commerce, as well as benefit from real-time visibility into financial workflows.

The Rise of Embedded Payments: A Rapidly Growing Industry Revolutionizing B2B Transactions

Embedded payments, with a current global transaction value of around $16 billion, are expected to grow significantly, potentially reaching $140 billion within the next three years. These payments are commonly found in services such as Uber, where the payment process occurs automatically after a ride. Yet, systems like Apple Pay and Google Pay, which require actions such as biometric authentication from users, only partly represent embedded payments.

This expected increase in embedded payments is primarily fueled by the business-to-business (B2B) sector. B2B systems are beginning to integrate payment processes directly into accounting software, making tasks like bill payments more straightforward.

An example of this integration is the partnership between Crezco, a UK fintech company, and Xero, an accounting software provider. This collaboration demonstrates how embedded payments are improving efficiency in back-end operations across various industries, such as logistics, where delivery confirmation now initiates the payment process, updating the traditional cash-on-delivery system to a digitized version.

Open Banking is advancing by providing standardized API access to payment systems, which enhances transaction automation and efficiency. This development is expected to streamline operations, accelerate payment cycles, and reduce costs, especially in B2B transactions.

Previously, many businesses treated payments as a separate, inconvenient step occurring after the delivery of goods or services. Embedded payments revolutionize this process by integrating the payment function into business software and platforms like enterprise resource planning (ERP) systems, procurement portals, and supply chain management tools.

In this framework, payments become a core component of the digital systems that manage business operations. Incorporating payment functionalities allows businesses to automate financial tasks, improve the efficiency of the payment process, and immediately access information on payment statuses, approvals, and cash flow. This integration fosters quicker decision-making, enhances supplier relationships, and facilitates business expansion.

With more businesses in the B2B sector adopting embedded payments, credentials, and tokens, the approach to business payments is transforming. Payments are now seen as an automated, integral part of business operations, not as a separate, manual task to be completed after other activities.

Key Drivers Behind the Growth of Embedded Payments in 2025

The expansion of embedded payments in 2025 is influenced by several important factors that are transforming how various industries handle finances.

- Industry Demand and Application: Real estate, automotive, and insurance sectors are increasingly integrating embedded finance to simplify transactions and improve customer interactions. These sectors handle large volumes of transactions, making embedded payments a practical choice for facilitating regular financial activities such as automated payments and providing immediate transaction visibility.

- Commerce Evolution: The emergence of new buying methods, both online and offline, is increasing the need for embedded payment systems. As consumer behavior changes, financial institutions and companies are adopting embedded finance to cut operational costs and generate new revenue sources, often through partnerships with fintech companies (Maast Blog). This integration allows for the more direct incorporation of financial services into customer interactions, including self-service checkout systems and embedded lending.

- Technological Advancements: Developments in API technology are simplifying the process for companies to integrate financial services into their platforms with little investment. These integrations are enhancing customer satisfaction and retention by enabling more straightforward, user-friendly payment methods. Furthermore, advancements like digital currencies and AI-driven fraud detection are improving the security and ease of use of embedded payments.

As these factors continue to influence the market, embedded payments are increasingly becoming crucial for businesses aiming to meet contemporary consumer expectations and boost operational efficiency.

Challenges and Opportunities in the Embedded Finance Market

The embedded finance market is experiencing rapid growth, evolving from basic payment and lending services to more intricate offerings such as insurance, payroll, taxes, and regulatory compliance solutions. The retail and e-commerce sectors are at the forefront of this transformation, benefiting from established digital infrastructures and the widespread adoption of payment systems. Additionally, industries like ridesharing and food delivery are effectively utilizing embedded finance to manage payments to gig workers, which also generates extra revenue through debit card transaction fees.

However, progress varies across sectors. The real estate industry, which relies on high-value transactions and traditional practices, encounters more significant challenges in adopting embedded finance solutions. Regulatory and legal hurdles remain substantial obstacles.

An emerging trend sees larger platforms exploring the option of building certain financial services in-house, particularly in areas like credit risk management and collections, to boost profitability. Despite this, these platforms continue to depend on third-party enablers for core infrastructure and regulatory compliance. These enablers are essential in helping platforms navigate the complex regulatory landscape, offering services like licensing and compliance management.

Traditional banks face disruption from the rise of embedded finance, as it shifts customer relationships away from them. This shift creates opportunities for banks to reposition themselves by investing in technology or forming partnerships with platforms. By leveraging their regulatory expertise and resources, banks can play a significant role in embedded finance through services like Banking-as-a-Service (BaaS), which allows other platforms to embed financial services within their ecosystems.

The ongoing expansion of embedded finance is set to transform how consumers and businesses interact with financial services, driven by continuous investments and innovations within the market.

Conclusion

Embedded payments are revolutionizing B2B transactions by integrating financial services directly into business operations, enhancing both efficiency and user experience. As businesses move away from traditional payment processes to digital payments, they are increasingly adopting technologies that facilitate seamless transactions within their existing systems. The rapid growth of embedded payments, projected to reach significant market values in the coming years, is driven by a combination of industry demand, evolving consumer behaviors, and technological advancements.

However, this transformation is not uniform across all sectors. Industries such as real estate face unique challenges due to regulatory hurdles, while others like retail and e-commerce are leading the charge in adopting embedded finance. Traditional banks, while disrupted by this shift, also have the opportunity to reposition themselves through strategic partnerships and technological investments.

As we look ahead, the importance of embedded payments in shaping the future of financial transactions cannot be overstated. By embracing these innovations, businesses can streamline their financial workflows, enhance customer interactions, and remain competitive in an increasingly complex global market. The evolution of embedded payments promises to create a more integrated and efficient financial landscape, ultimately benefiting both businesses and consumers alike.